Downloaded 30 times

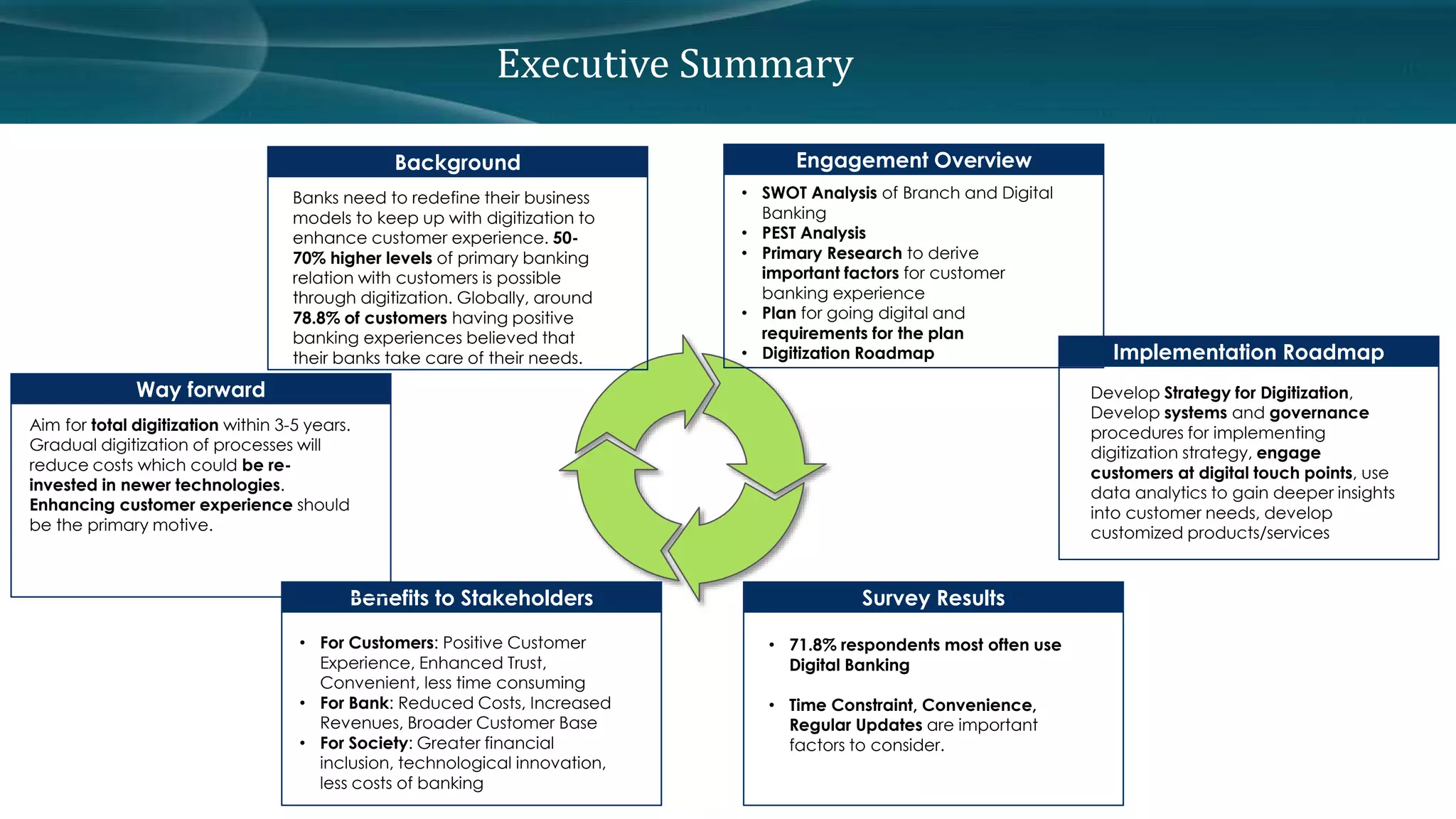

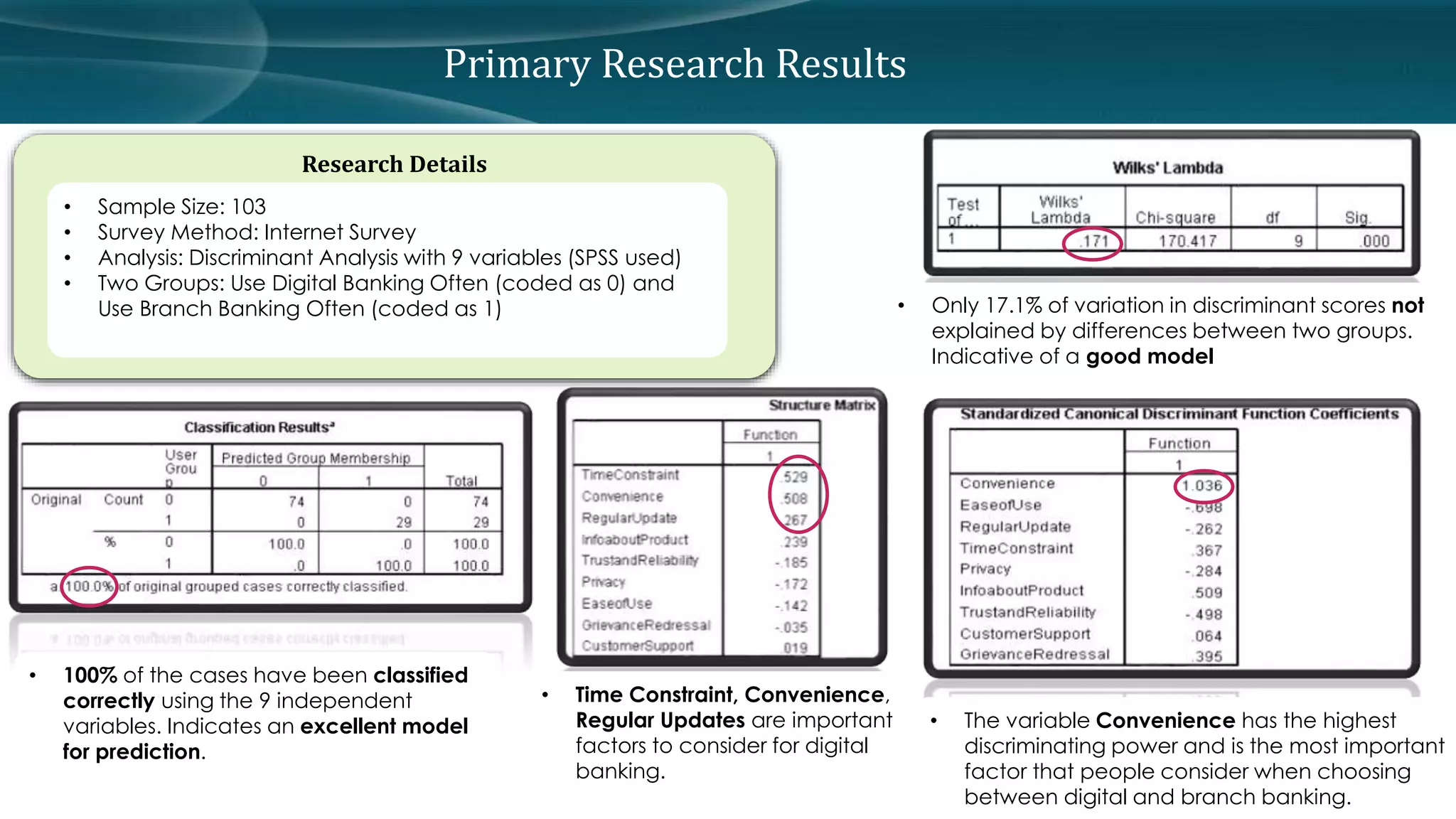

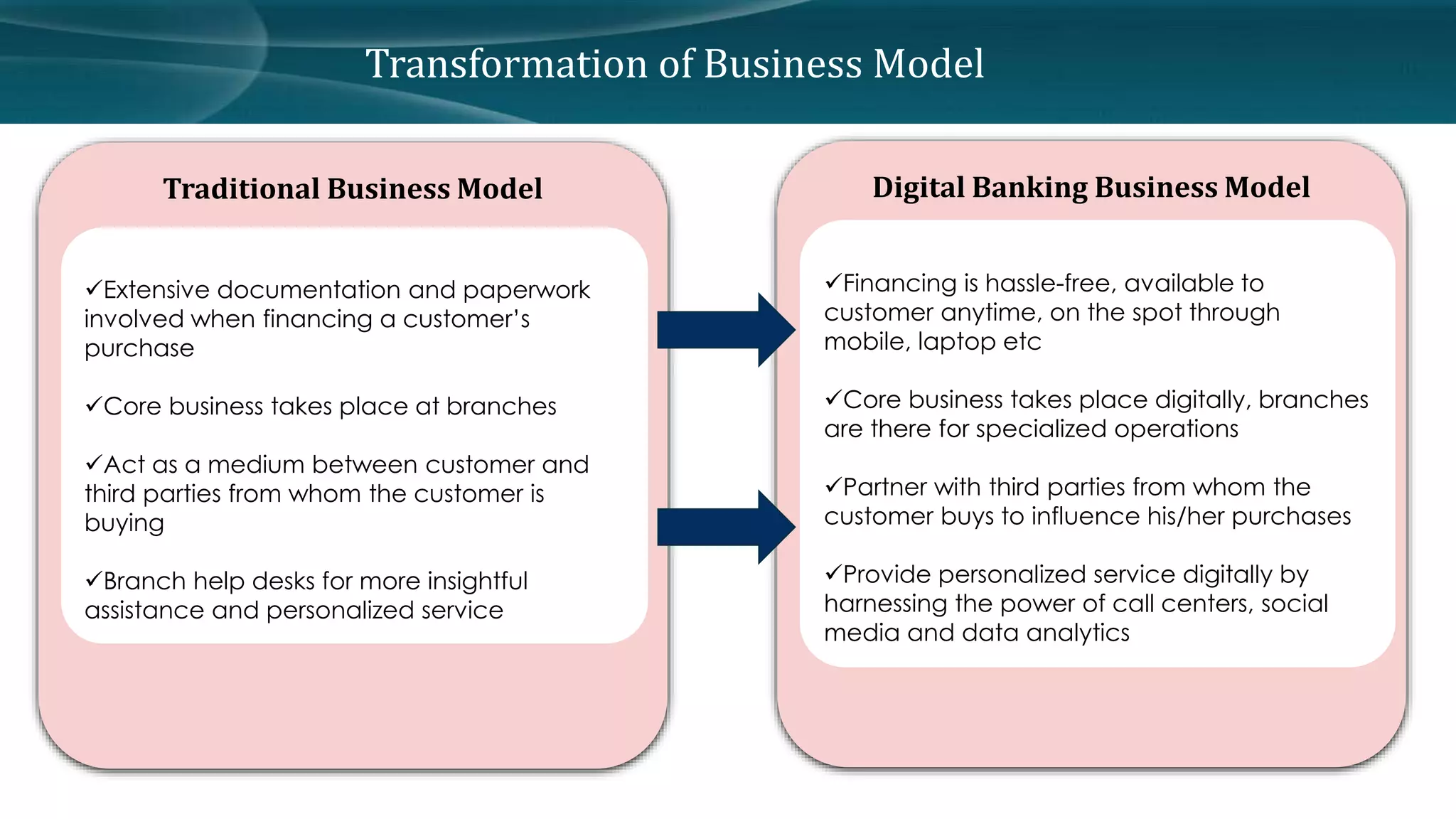

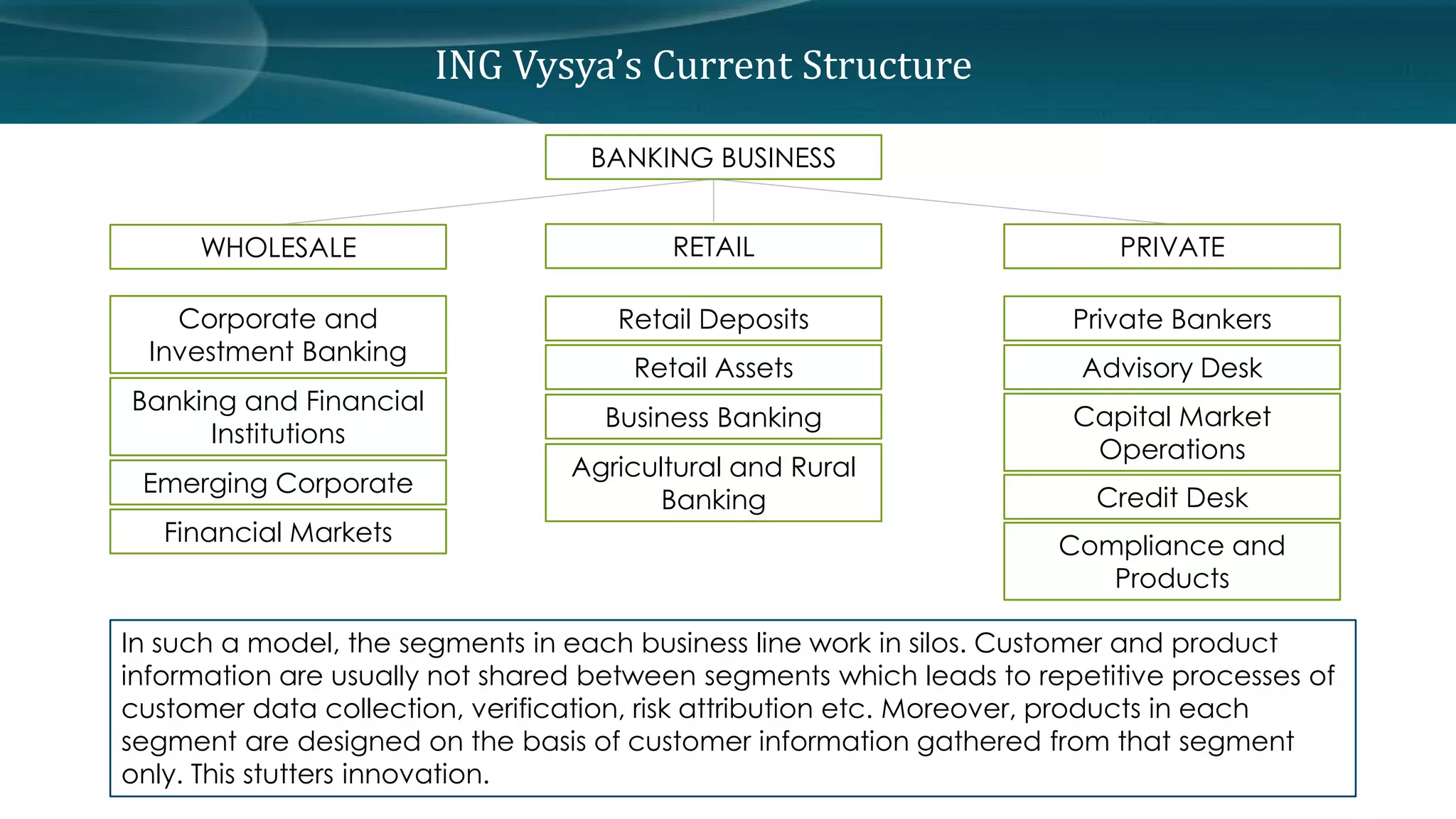

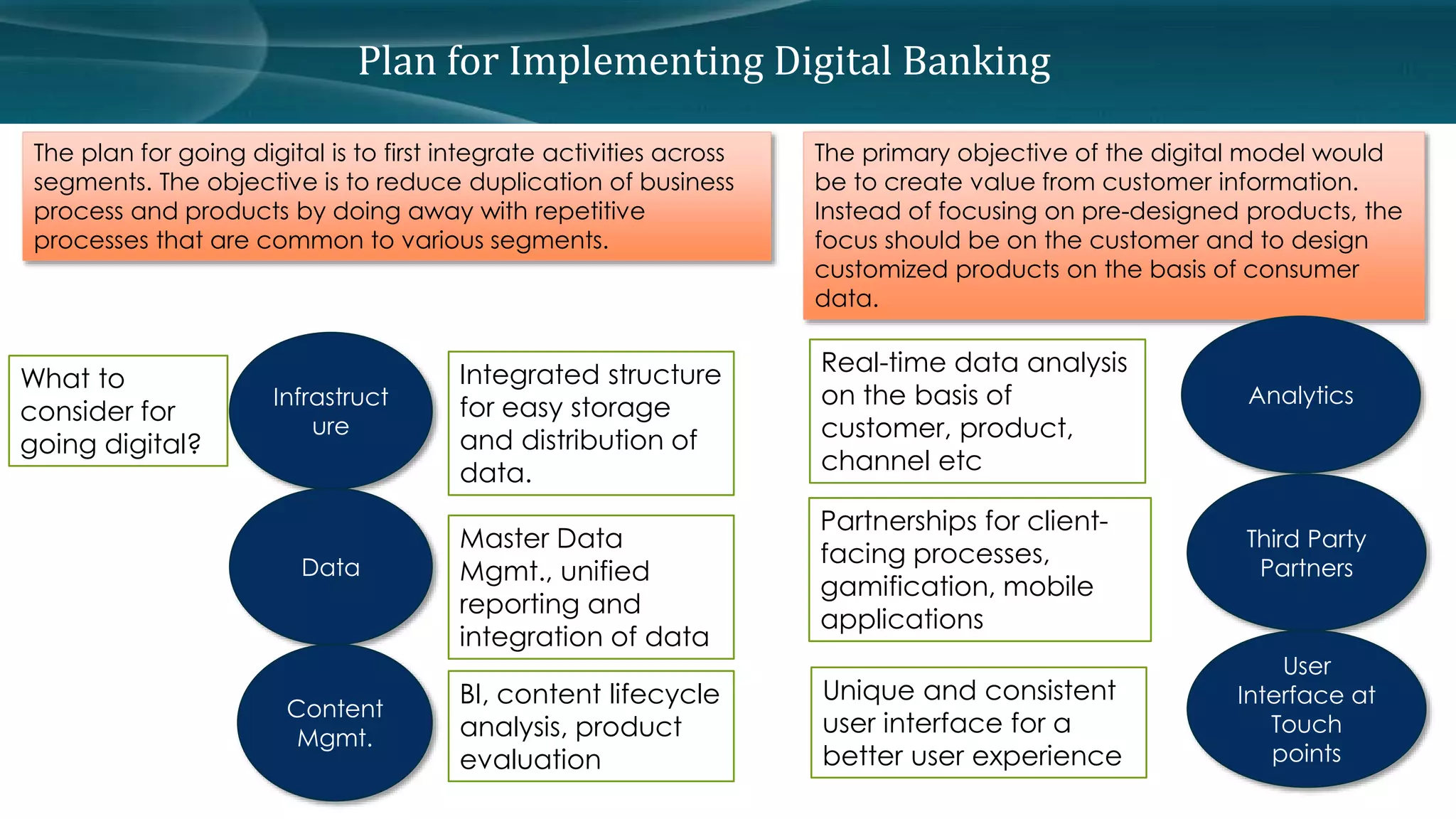

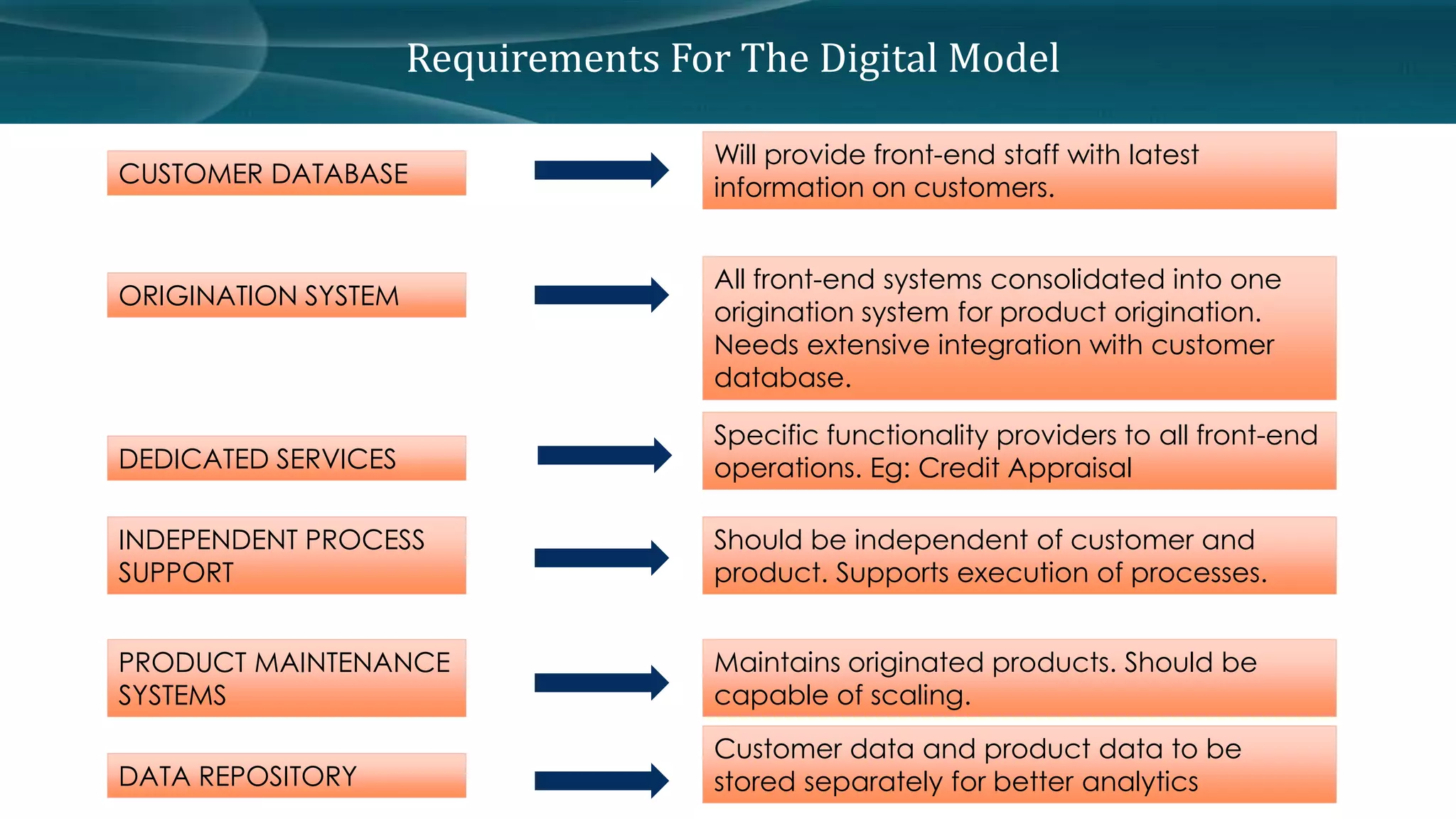

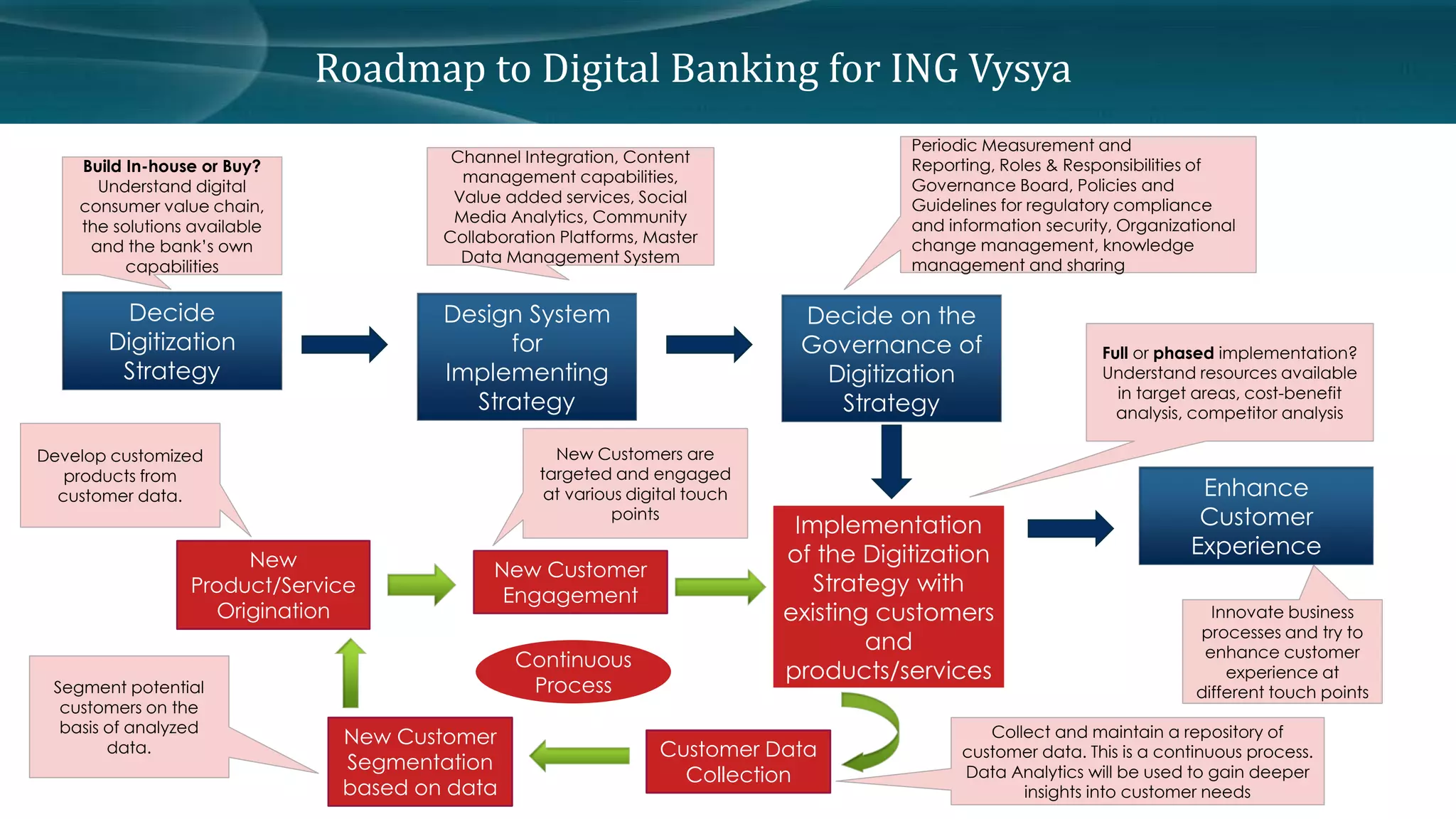

- The document discusses recommendations for digitizing banking services based on a comparative study of digital and branch banking. - A survey found customers prefer digital banking over branches due to convenience and time savings. Key implementation factors are infrastructure, data management, analytics, and user interfaces. - The recommendations include creating an integrated customer database, origination systems, independent processing support, and data repository to power customized digital products and services.