Downloaded 282 times

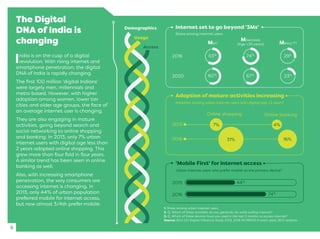

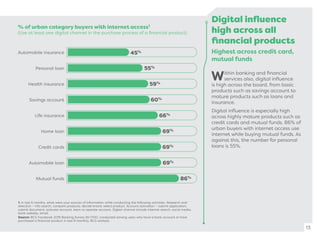

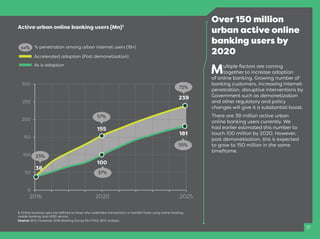

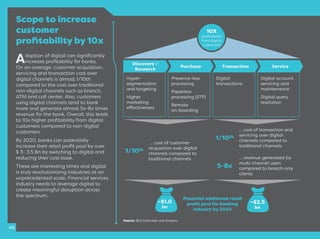

India is experiencing a digital revolution in financial services, driven by increased internet and smartphone penetration. The digital influence on financial products is significant, but the adoption of online banking remains low due to consumer inertia and concerns about security. Financial institutions must adapt and leverage digital channels to enhance customer experience and profitability, as an estimated 120 million urban banking users will be digitally influenced by 2020.