Downloaded 11,688 times

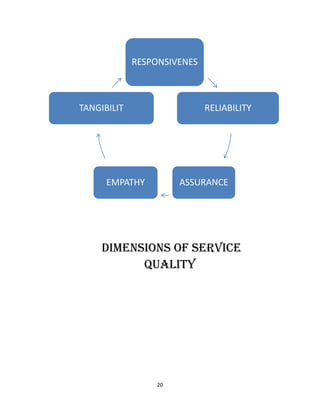

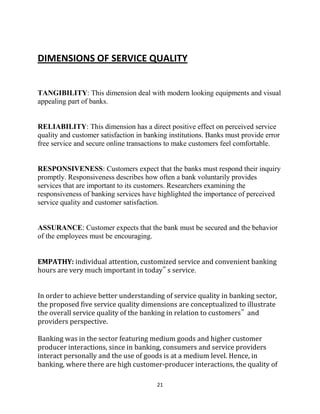

This document is a project report on the service quality of HDFC Bank. It includes an introduction, company profile of HDFC Bank, discussion of service quality in banks, research objectives, methodology, data analysis, findings, conclusion and recommendations. It also includes various appendices related to the project such as a questionnaire. The overall aim of the report is to evaluate the service quality provided by HDFC Bank to its customers.