Downloaded 14 times

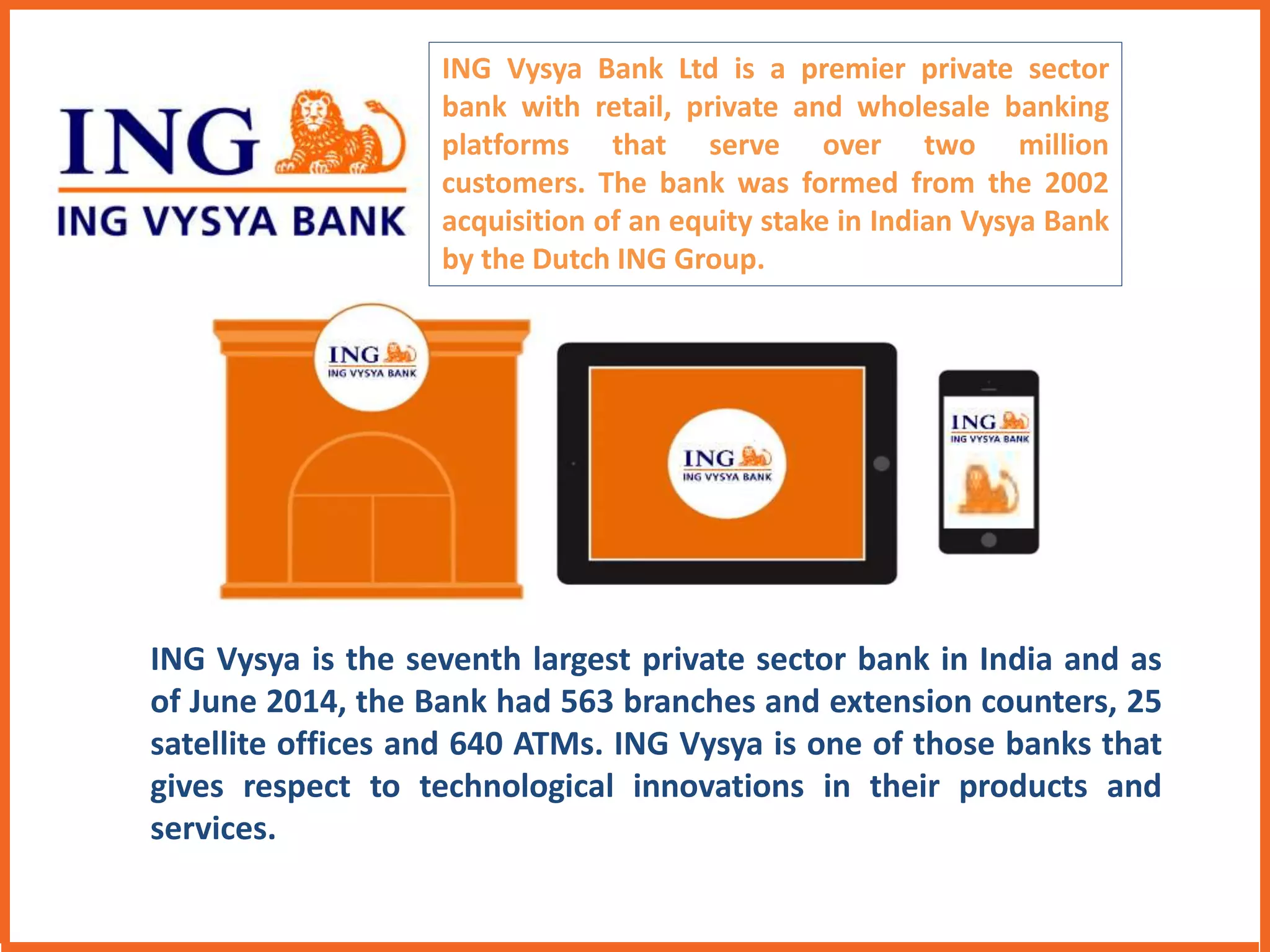

This document discusses the transition from traditional branch banking to digital banking. It analyzes the strengths and weaknesses of branch banking versus digital banking. The document then recommends a roadmap for ING Vysya Bank to move towards digital banking, including adopting a more customer-centric approach, targeting rural areas through technology, finding new ways to engage customers, and integrating products and services on a digital platform.