Download as PDF, PPTX

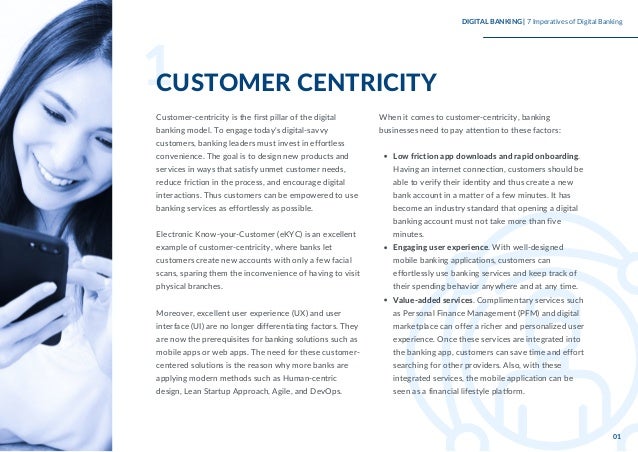

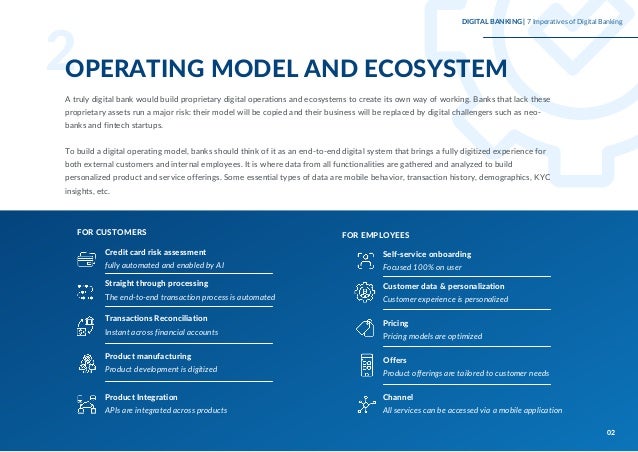

The document outlines six essential imperatives for building a successful digital banking model, which includes customer centricity, operating models, technology principles, data analytics, digital start-up culture, and regulatory compliance. It emphasizes the need for banks to create seamless customer experiences by leveraging modern technologies and agile processes, while fostering a culture of innovation and responsiveness. The paper highlights the role of regulators in supporting the transformation of traditional banks into competitive digital entities.