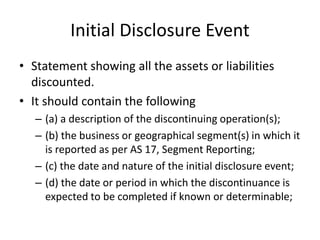

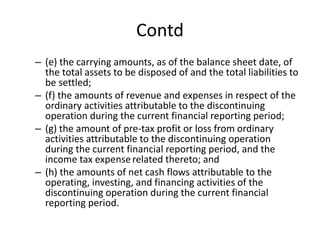

This document outlines Accounting Standard 24 regarding discontinuing operations. The objective is to enhance the ability of users of financial statements to project cash flows, earnings, and financial position by segregating information about discontinuing operations from continuing operations. A discontinuing operation must be disposed of or abandoned per a single coordinated plan, represent a separate business line or geographical area, and be distinguishable operationally and for reporting. Initial disclosure of a discontinuing operation must include a description, the business segment, the disclosure event date and nature, expected completion date if known, carrying amounts of assets and liabilities, revenue/expenses, pre-tax profit/loss, and cash flows attributable to the discontinuing operation.