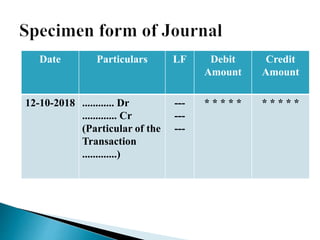

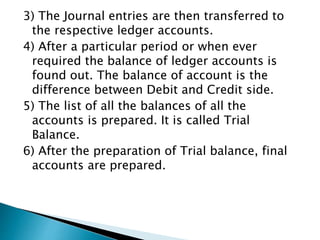

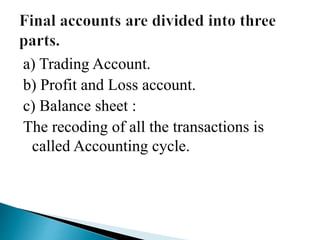

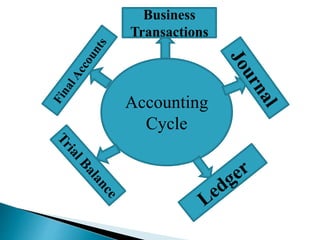

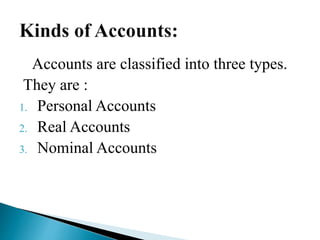

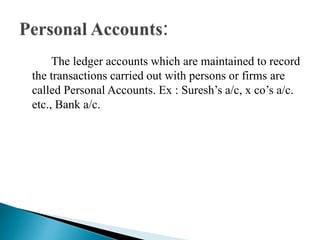

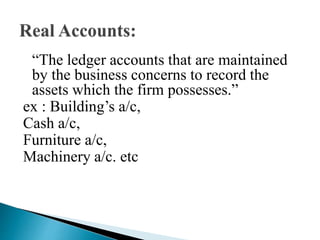

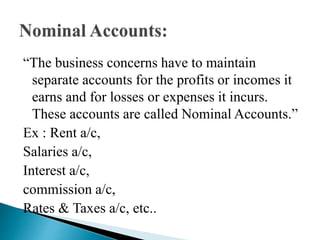

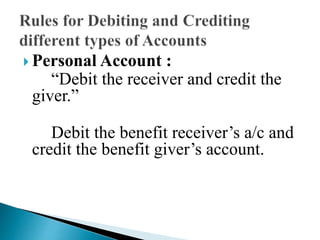

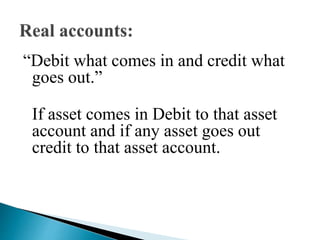

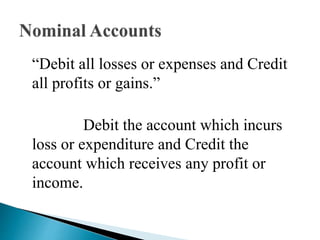

The document discusses accounting, defining it as the process of recording, classifying, and summarizing business transactions and events in terms of money to assess the financial performance and position of a business. It notes that accounting involves recording debits and credits according to set rules, and that accounts are classified as personal, real, or nominal. The accounting cycle is also summarized as the process of recording transactions, posting to ledgers, preparing trial balances and final financial statements.