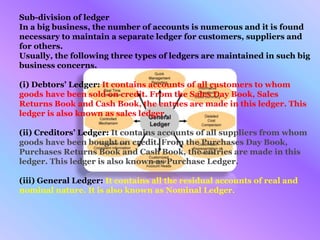

The document provides an overview of ledger accounting, explaining its role as a main book of accounts where transactions are classified and summarized. It details the differences between journals and ledgers, the posting process, and various types of ledgers including debtors', creditors', and general ledgers. Additionally, it highlights the advantages of using ledgers, such as enhanced accuracy and comprehensive tracking of transactions related to assets, liabilities, income, and expenses.

![This presentation is owned by

ABUL KALAM AZAD PATWARY

“for class 9-10[accounting]”](https://image.slidesharecdn.com/accounting-chapter-7-150209050048-conversion-gate02/85/Accounting-chapter-7-1-320.jpg)

![This presentation is owned by

ABUL KALAM AZAD PATWARY

“for class 9-10[accounting]”](https://image.slidesharecdn.com/accounting-chapter-7-150209050048-conversion-gate02/75/Accounting-chapter-7-1-2048.jpg)