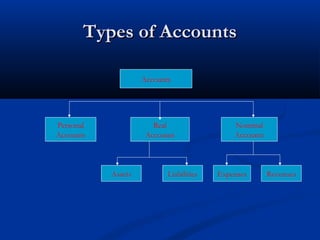

The document provides an overview of basic accounting concepts and the accounting cycle. It defines accounting as a process to record and communicate financial information. It explains the accounting equation that balances assets, liabilities, and owner's equity. Transactions are exchanges that affect accounts. The accounting cycle includes analyzing transactions, journalizing, posting, preparing a trial balance, adjusting entries, financial statements, and closing entries. The document also outlines users and branches of accounting.