Downloaded 35 times

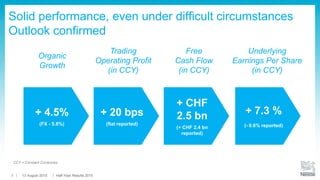

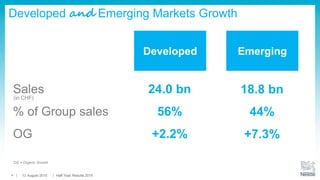

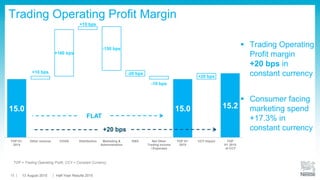

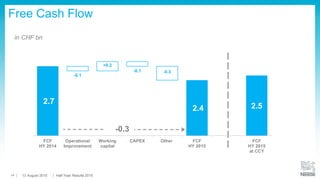

This document provides a summary of Nestlé's 2015 half-year results. Overall, Nestlé saw solid organic growth of 4.5% despite negative foreign exchange impacts. All regions saw organic growth, with particular strengths in Zone EMENA and Nestlé Waters. The trading operating profit margin was flat in constant currencies due to pricing and efficiencies offsetting investment in marketing. Consumer-facing marketing spend increased 17.3% in constant currencies. The outlook for the full year remains unchanged with a goal of around 5% organic growth and margin improvements.