Download as PDF, PPTX

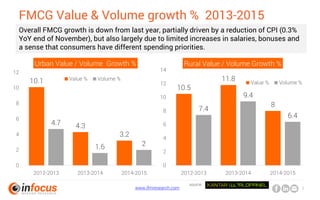

The document analyzes the changing landscape of consumer retail in Vietnam, highlighting a decline in overall FMCG growth and a shift in shopping preferences towards convenience stores and online platforms. It shows increasing consumer intent to shop via smartphones and online channels, with modern trade outlets gaining favor. Key insights include the importance of product range and convenience in store selection, as well as the anticipated impact of greater online shopping and competition in the retail sector.

![[Kantar worldpanel] FMCG Monitor from March to November 2017](https://cdn.slidesharecdn.com/ss_thumbnails/kantarworldpanel-fmcgmonitormarch-november2017en-171229122250-thumbnail.jpg?width=640&height=640&fit=bounds)

![[E-Contest 2020] No.1 Team](https://cdn.slidesharecdn.com/ss_thumbnails/e-contest7-210118082139-thumbnail.jpg?width=640&height=640&fit=bounds)

![[Nielsen] The need for speed: giving vietnamese consumers what they want](https://cdn.slidesharecdn.com/ss_thumbnails/cvsneedforspeeden-160405065431-160802012129-171227171353-thumbnail.jpg?width=640&height=640&fit=bounds)