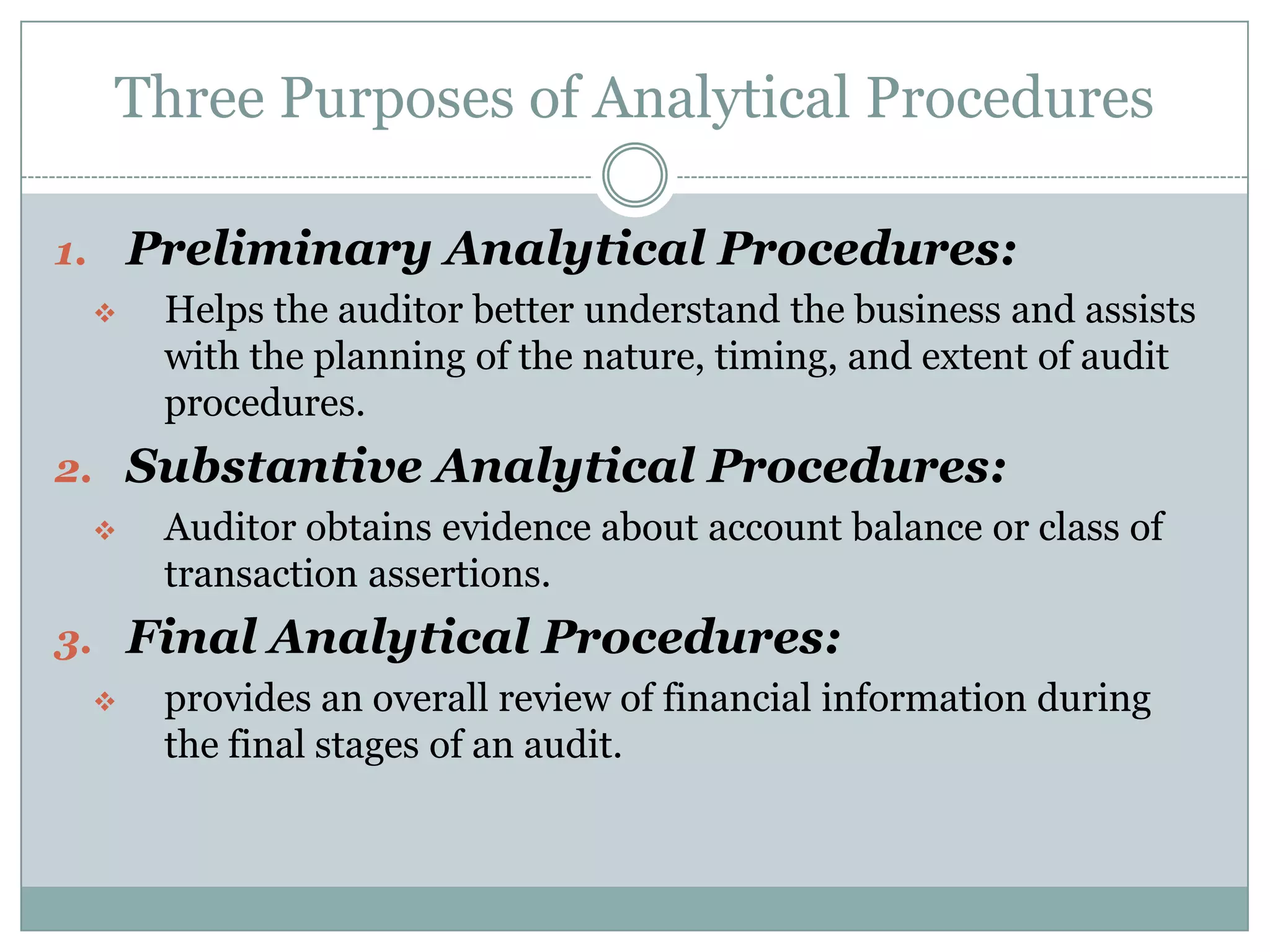

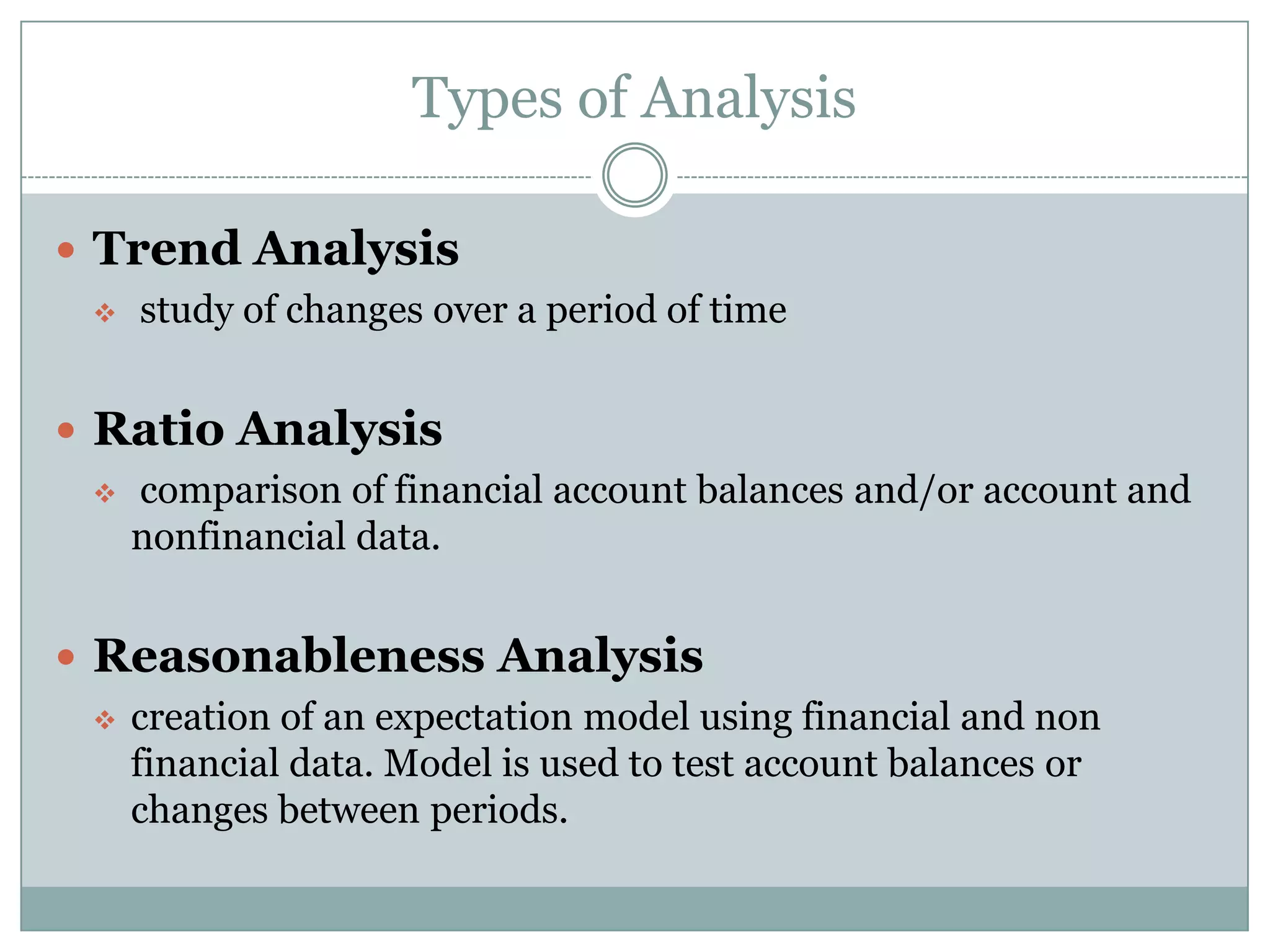

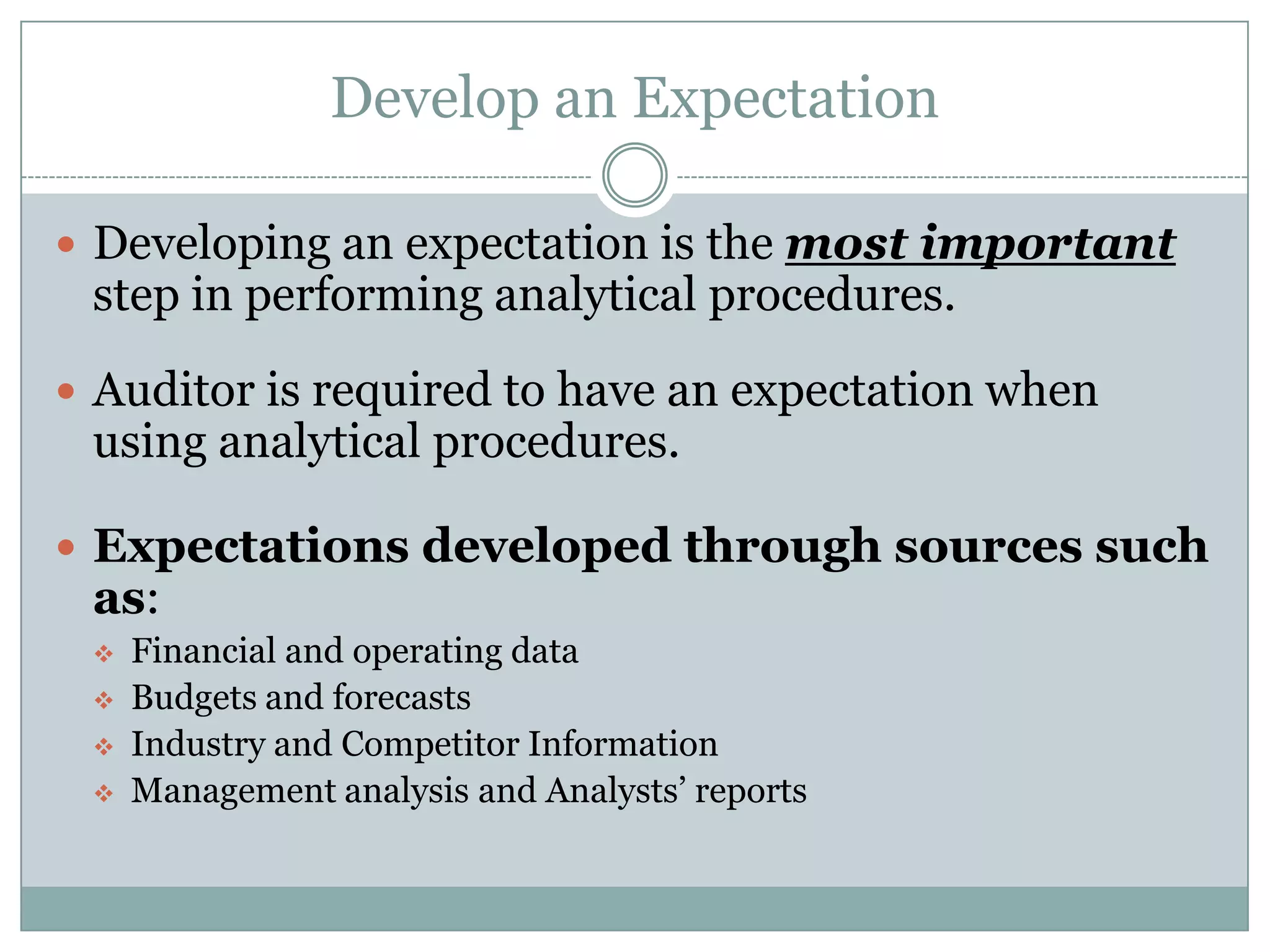

Analytical procedures are an important part of the audit process and include evaluations of financial information through analysis of relationships among financial and non-financial data. There are three types of analytical procedures: preliminary, substantive, and final. Preliminary procedures help plan the audit, substantive procedures test account balances and transactions, and final procedures provide an overall review. Developing an expectation is the most important step for substantive procedures, where the expectation is compared to actual amounts to investigate significant differences.