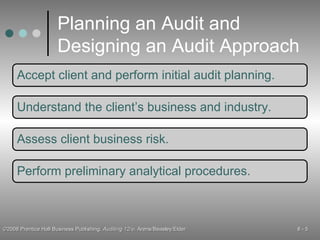

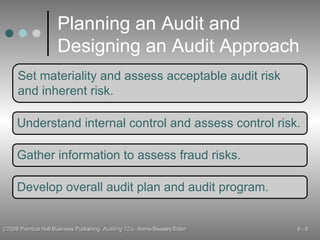

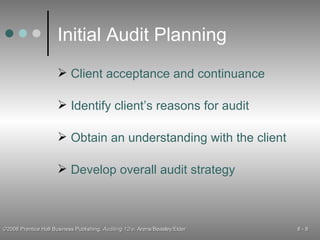

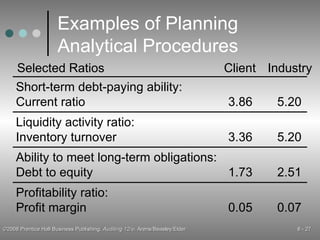

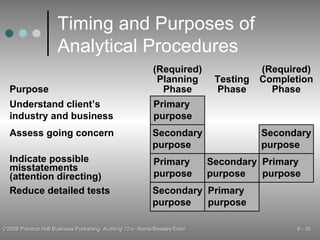

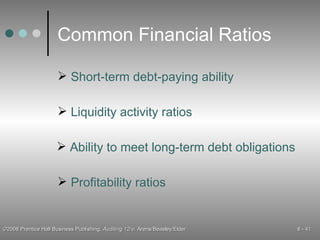

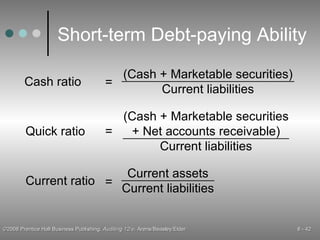

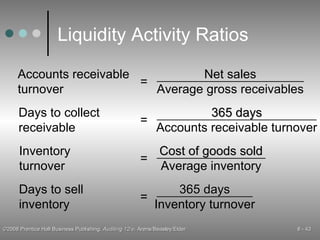

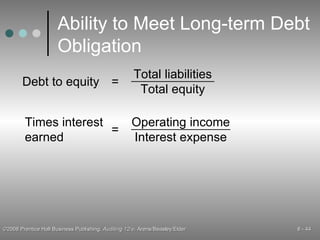

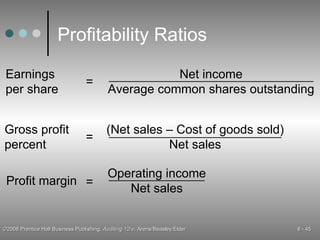

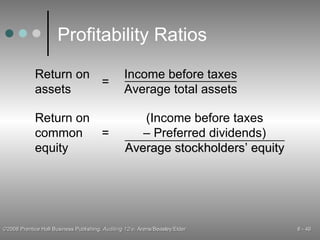

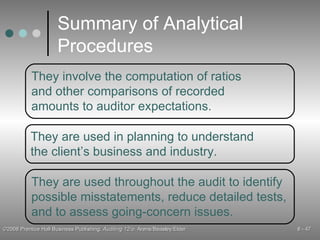

Audit planning involves three main reasons: 1) to obtain sufficient evidence, 2) to help keep costs reasonable, and 3) to avoid misunderstandings with the client. The key parts of planning include accepting the client, understanding the client's business and industry, assessing business risks, and performing preliminary analytical procedures. Analytical procedures are used in the planning, testing, and completion phases of the audit to understand the client, identify possible misstatements, and reduce detailed tests. Common financial ratios used in analytical procedures include liquidity, activity, debt obligation, and profitability ratios.