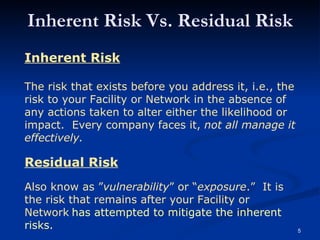

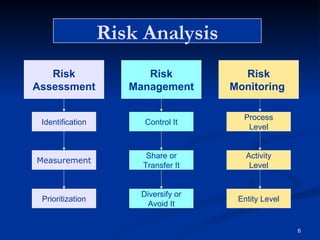

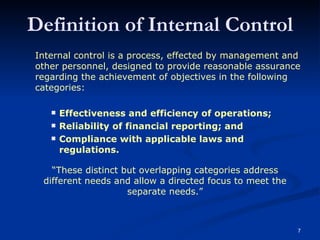

This document discusses risk assessments and their importance for audit planning. It provides definitions for risk and risk assessment, and explains how risk assessments allow entities to understand potential impacts on objectives. Risk assessments employ both qualitative and quantitative methods, relate risks to time horizons and objectives, and assess inherent and residual risks. The document also discusses how internal auditors can add value through risk-based audit planning and evaluating management's risk assessments and controls. Key components of risk assessments are outlined.