Wockhardt Q4FY12 Results Drive Growth

•

1 like•509 views

Wockhardt posted a net loss of Rs 191.6 crore for Q4FY12 due to exceptional items such as derivative liabilities and goodwill impairment. Excluding exceptional items, net profit grew 57% YoY to Rs 261.6 crore. Net sales grew 32.2% YoY to Rs 1,241.4 crore. The brokerage expects the company to benefit from its product portfolio and focus on high margin products, projecting a revenue CAGR of 14.8% over FY12-FY14. However, it has lowered earnings estimates for FY13-FY14 to factor in higher taxes and the potential delay of a nutrition business sale. The stock currently trades at attractive valu

Recommended

More Related Content

What's hot

What's hot (19)

Similar to Wockhardt Q4FY12 Results Drive Growth

Similar to Wockhardt Q4FY12 Results Drive Growth (20)

More from Vinit Bolinjkar LION bolinjkar.vinit@gmail.com

More from Vinit Bolinjkar LION bolinjkar.vinit@gmail.com (20)

Recently uploaded

Recently uploaded (20)

Wockhardt Q4FY12 Results Drive Growth

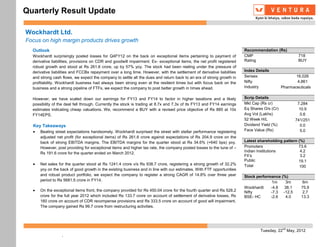

- 1. Quarterly Result Update Wockhardt Ltd. Focus on high margin products drives growth Outlook Recommendation (Rs) Wockhardt surprisingly posted losses for Q4FY12 on the back on exceptional items pertaining to payment of CMP 718 derivative liabilities, provisions on CDR and goodwill impairment. Ex- exceptional items, the net profit registered Rating BUY robust growth and stood at Rs 261.6 crore, up by 57% yoy. The stock had been reeling under the pressure of derivative liabilities and FCCBs repayment over a long time. However, with the settlement of derivative liabilities Index Details and strong cash flows, we expect the company to settle all the dues and return back to an era of strong growth in Sensex 16,026 profitability. Wockhardt business had always been strong even at the resilient times but with focus back on the Nifty 4,861 business and a strong pipeline of FTFs, we expect the company to post better growth in times ahead. Industry Pharmaceuticals However, we have scaled down our earnings for FY13 and FY14 to factor in higher taxations and a likely Scrip Details possibility of the deal fell through. Currently the stock is trading at 8.7x and 7.3x of its FY13 and FY14 earnings Mkt Cap (Rs cr) 7,284 estimates indicating cheap valuations. We, recommend a BUY with a revised price objective of Rs 885 at 10x Eq Shares O/s (Cr) 10.9 FY14EPS. Avg Vol (Lakhs) 0.6 52 Week H/L 741/251 Key Takeaways Dividend Yield (%) 0.0 Beating street expectations handsomely, Wockhardt surprised the street with stellar performance registering Face Value (Rs) 5.0 adjusted net profit (for exceptional items) of Rs 261.6 crore against expectations of Rs 204.9 crore on the back of strong EBITDA margins. The EBITDA margins for the quarter stood at Rs 34.6% (+640 bps) yoy. Latest shareholding pattern (%) However, post providing for exceptional items and higher tax rate, the company posted losses to the tune of – Promoters 73.6 Indian Institutions 4.2 Rs 191.6 crore for the quarter ended on March 2012. FII’s 3.2 Public 19.1 Net sales for the quarter stood at Rs 1241.4 crore v/s Rs 938.7 crore, registering a strong growth of 32.2% Total 100 yoy on the back of good growth in the existing business and in line with our estimates. With FTF opportunities and robust product portfolio, we expect the company to register a strong CAGR of 14.8% over three year Stock performance (%) period to Rs 5681.5 crore in FY14. 1m 3m 6m Wockhardt -4.8 38.1 75.9 On the exceptional items front, the company provided for Rs 450.04 crore for the fourth quarter and Rs 528.2 Nifty -7.3 -12.5 2.7 crore for the full year 2012 which included Rs 133.7 crore on account of settlement of derivative losses, Rs BSE- HC -2.6 4.0 13.3 160 crore on account of CDR recompense provisions and Rs 333.5 crore on account of good will impairment. The company gained Rs 99.7 crore from restructuring activities. nd Tuesday, 22 May, 2012 .

- 2. Quarterly Result Update On the earnings front, the depreciation and interest expenses were in line with our expectations. However, the tax rate at 31%, stood higher than our estimates. Factoring in higher tax rate, we have scaled down our earnings to Rs 808.2 crore and 968.4 crore for FY13 and FY14 respectively v/s Rs 889.6 crore and Rs 1070.1 crore previously. Further, the Wockhardt- Danone deal for the sale of nutrition business was supposed to be culminated in the month of March. However, it got delayed, considering the management has not given time line of the deal, we have scaled down our earnings and have not factored in the deal. However, the deal if sails through would be EPS accretive, we estimate the company to post an EPS of Rs 164 for FY13 v/s the current forecast of Rs 82.4. nd Tuesday, 22 May, 2012

- 3. Quarterly Result Update Description Q4FY12 Q4FY11 % Chg. Q4FY12 Q3FY12 % Chg. FY201203 FY201103 % Chg. Net Sales 1241.4 938.7 32.2 1241.4 1208.7 2.7 4613.8 3751.2 23.0 Other operational Income 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 Total Oper. Income(TOI) 1241.4 938.7 32.2 1241.4 1208.7 2.7 4613.8 3751.2 23.0 Raw Materials Cons.- 312.5 216.4 44.4 312.5 327.1 -4.5 1213.0 875.0 38.6 % to TOI 25.2 23.1 - 25.2 27.1 - 26.3 23.3 - Stock adj. (-)Inc / (+)Dec- -8.0 6.6 - -8.0 -13.9 -42.4 -106.3 61.7 - % to TOI -0.6 0.7 - -0.6 -1.2 - -2.3 1.6 - Net Raw Mat adj. for stock 304.5 223.0 36.6 304.5 313.2 -2.8 1106.7 936.7 18.1 % to TOI 24.5 23.8 - 24.5 25.9 - 24.0 25.0 - Other expenses 326.1 307.0 6.2 326.1 379.3 -14.0 1500.0 1381.1 8.6 % to TOI 26.3 32.7 - 26.3 31.4 - 34.2 38.0 - Contribution Net_Sales 610.8 408.8 49.4 610.8 486.6 25.5 1930.9 1390.1 38.9 Personnel 181.5 143.8 26.2 181.5 139.8 29.8 567.3 524.7 8.1 % to TOI 14.6 15.3 - 14.6 11.6 - 12.3 14.0 - Total expenditure 812.1 673.7 20.5 812.1 832.3 -2.4 3173.9 2842.5 11.7 Operating Profit 429.3 265.0 62.0 429.3 376.4 14.1 1439.9 908.7 58.4 % to TOI 34.6 28.2 - 34.6 31.1 - 29.6 23.1 - Non-Operating Income 61.5 161.8 -62.0 61.5 8.6 615.1 78.2 196.0 -60.1 Interest 48.2 90.1 -46.5 48.2 67.9 -29.0 214.4 267.1 -19.7 Exceptional Items -450.4 -172.1 161.7 -450.4 19.9 - -452.0 -529.8 -14.7 Gross Profit 893.0 508.8 75.5 893.0 297.1 200.6 1755.7 1367.4 28.4 Depreciation 28.8 27.1 6.2 28.8 27.7 4.0 122.5 116.6 5.1 PBT before Extra-ord -36.7 137.4 - -36.7 250.1 - 576.7 104.4 452.6 % to TOI -3.0 14.6 - -3.0 20.7 - 12.5 2.8 - Extraordinary Items - - - 0.0 0.0 - 0.0 0.0 0.0 PBT -36.7 137.4 - -36.7 250.1 - 576.7 104.4 452.6 Tax Rate -415.3 -21.0 1880.0 -415.3 14.8 - 40.8 8.3 392.5 Prov. for Tax 152.2 -28.8 - 152.2 37.0 311.4 235.1 8.6 2621.4 % to TOI 12.3 -3.1 - 12.3 3.1 - 5.1 0.2 - Profit after Tax -188.9 166.2 - -188.9 213.1 - 341.6 95.7 256.9 % to TOI -15.2 17.7 - -15.2 17.6 - 7.4 2.6 - Minority Interest - - - 0.0 0.0 - 0.0 0.0 0.0 PAT (adj. For MI) -191.6 161.8 - -191.6 212.8 - 342.7 90.5 278.5 Face Value 5.0 5.0 - 5.0 5.0 - 5.0 5.0 - Equity Share capital 54.7 54.7 - 54.7 54.7 - 54.7 54.7 - EPS (Rs.) -17.3 15.2 - -17.3 19.5 - 31.2 8.7 256.9 CEPS (Rs.) -14.6 17.7 - -14.6 22.0 - 42.4 19.4 118.6 nd Tuesday, 22 May, 2012

- 4. Quarterly Result Update P/E Bands P/B Bands EV/EBITDA Bands 2000 2000 25000 1500 1800 1000 1600 20000 1400 500 1200 15000 0 1000 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 -500 800 10000 -1000 600 -1500 400 5000 -2000 200 -2500 0 0 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 Dec-00 Dec-02 Dec-04 Dec-06 Dec-08 Dec-10 Dec-12 CMP 8X 11.685X 15.37X 19.055X 22.74X CMP 1X 2.55X 4.1X 5.65X 7.2X EV 5X 7.63X 10.26X 12.89X 15.52X NIFTY Comparison BSE-Healthcare Comparison 250.00 250.0 200.00 200.0 150.00 150.0 100.00 100.0 50.00 50.0 0.00 0.0 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 May-11 Jul-11 Sep-11 Nov-11 Jan-12 Mar-12 Wockhardt NIFTY Wockhardt BSEHC nd Tuesday, 22 May, 2012

- 5. Quarterly Result Update Financial & Projections Y/E March, Fig in Rs. Cr FY 2011 FY 2012e FY 2013e FY 2014e Y/E March, Fig in Rs. Cr FY 2011 FY 2012e FY 2013e FY 2014e Profit & Loss Statement Per Share Data (Rs) Net Sales 3751.2 4613.8 5208.7 5681.5 EPS 8.7 35.1 73.9 88.5 % Chg. 23.0 12.9 9.1 Cash EPS 19.4 46.3 86.5 101.9 Total Expenditure 2842.5 3174.1 3605.7 3853.3 DPS 0.0 0.0 0.0 0.0 % Chg. 11.7 13.6 6.9 Book Value 103.0 134.5 208.3 296.4 EBITDA 908.7 1439.7 1603.1 1828.2 Capital, Liquidity, Returns Ratio EBITDA Margin % 24.2 31.2 30.8 32.2 Debt / Equity (x) 3.4 2.0 1.5 0.8 Other Income 15.9 23.5 26.5 30.5 Current Ratio (x) 2.3 1.6 2.3 2.2 Exceptional items 436.6 506.8 0.0 0.0 ROE (%) 8.5 26.1 35.5 29.9 PBDIT 488.1 956.4 1629.5 1858.7 ROCE (%) 9.8 21.5 28.8 31.9 Depreciation 116.6 122.5 138.0 147.0 Dividend Yield (%) 0.0 0.0 0.0 0.0 Interest & Finance Charges 267.1 214.4 320.2 310.4 Valuation Ratio (x) PBT 104.3 619.5 1171.4 1401.3 P/E 82.1 20.4 9.7 8.1 Tax Provisions 8.6 235.1 363.1 432.9 P/BV 7.0 5.3 3.4 2.4 Reported PAT 95.7 384.3 808.2 968.4 EV/Sales 2.7 2.2 1.9 1.8 PAT Margin (%) 2.6 8.3 15.5 17.0 EV/EBIDTA 11.1 7.0 6.3 5.5 Efficiency Ratio (x) Manpower cost / Sales (%) 14.0 12.8 14.8 14.8 Inventory (days) 69.4 70.0 70.0 70.0 Other Exp / Sales (%) 20.1 19.6 18.8 18.5 Debtors (days) 58.9 60.0 60.0 60.0 Tax Rate (%) 8.3 38.0 31.0 30.9 Creditors (days) 42.5 45.0 45.0 45.0 Balance Sheet Cash Flow statement Share Capital 799.9 816.1 816.1 816.1 Profit After Tax 90.5 342.7 808.2 963.6 Reserves & Surplus 326.5 654.9 1463.2 2426.8 Depreciation 116.6 122.5 138.0 147.0 Minority Interest & Others 0.0 0.0 0.0 0.0 Working Capital Changes 258.0 578.6 -718.1 -86.2 Total Loans 3849.5 2967.2 3370.7 2587.1 Others 151.1 -126.5 0.0 0.0 Deferred Tax Iiability 0.0 0.0 0.0 0.0 Operating Cash Flow 616.2 917.4 228.1 1024.4 Total Liabilities 4975.9 4438.2 5649.9 5830.0 Capital Expenditure -214.3 -720.4 170.4 -300.0 Goodwill 0.0 0.0 0.0 0.0 Change in Investment -174.6 886.3 -879.3 -9.7 Gross Block 4048.7 4769.1 4598.6 4898.6 Cash Flow from Investing -389.0 165.9 -708.8 -309.7 Less: Acc. Depreciation 1468.4 1295.4 1433.4 1580.4 Proceeds from equity issue 76.6 16.2 0.0 0.0 Net Block 2580.2 3473.6 3165.3 3318.3 Inc/ Dec in Debt -168.0 -882.3 403.5 -783.6 Capital Work in Progress 887.4 0.0 878.4 887.1 Dividend and DDT 0.0 0.0 0.0 0.0 Investments 89.6 90.8 91.7 92.6 Cash Flow from Financing -91.4 -866.2 403.5 -783.6 Net Current Assets 1160.5 974.8 1615.7 1633.0 Net Change in Cash 135.9 217.1 -77.3 -68.9 Deferred Tax Assets 258.2 -101.0 -101.0 -101.0 Opening Cash Balance 347.0 482.9 700.0 622.7 Total Assets 4975.9 4438.2 5649.9 5830.0 Closing Cash Balance 482.9 700.0 622.7 553.9 nd Tuesday, 22 May, 2012

- 6. Quarterly Result Update Ventura Securities Limited Corporate Office: C-112/116, Bldg No. 1, Kailash Industrial Complex, Park Site, Vikhroli (W), Mumbai – 400079 This report is neither an offer nor a solicitation to purchase or sell securities. The information and views expressed herein are believed to be reliable, but no responsibility (or liability) is accepted for errors of fact or opinion. Writers and contributors may be trading in or have positions in the securities mentioned in their articles. Neither Ventura Securities Limited nor any of the contributors accepts any liability arising out of the above information/articles. Reproduction in whole or in part without written permission is prohibited. This report is for private circulation. nd Tuesday, 22 May, 2012