Downloaded 34 times

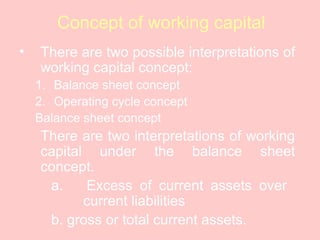

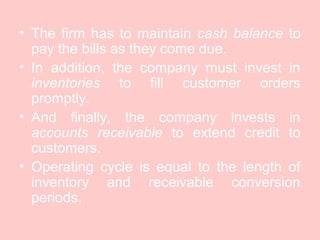

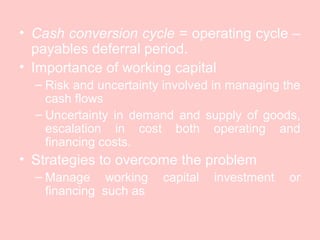

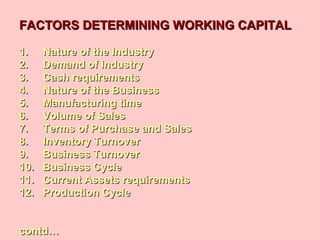

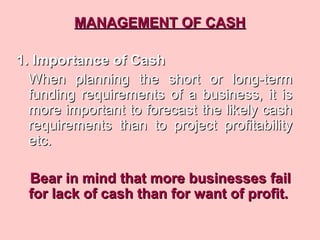

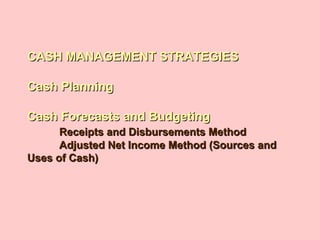

![ECONOMIC ORDER QUANTITY [ EOQ ]ECONOMIC ORDER QUANTITY [ EOQ ]

The ordering quantity problems are solved byThe ordering quantity problems are solved by

the firm by determining the EOQ ( or thethe firm by determining the EOQ ( or the

Economic Lot Size ) that is the optimum levelEconomic Lot Size ) that is the optimum level

of inventory.of inventory.

There are two types of costs involved in thisThere are two types of costs involved in this

model.model.

ordering costsordering costs

carrying costscarrying costs

The EOQ is that level of inventory whichThe EOQ is that level of inventory which

MINIMIZES the total of ordering and carryingMINIMIZES the total of ordering and carrying](https://image.slidesharecdn.com/workingcapitalppt-170411070330/85/Working-capital-ppt-59-320.jpg)

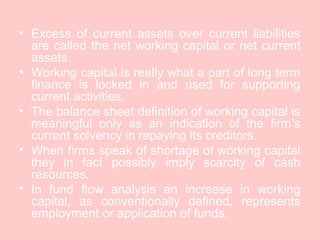

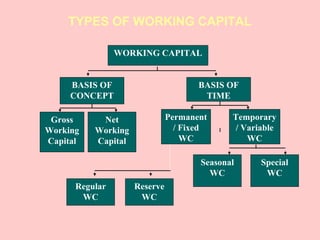

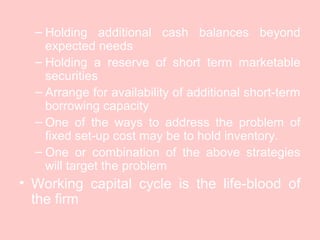

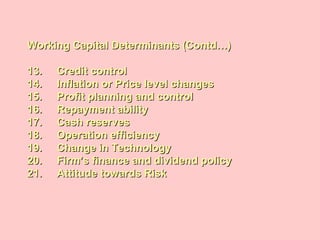

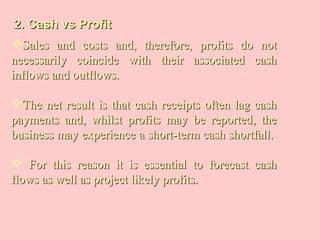

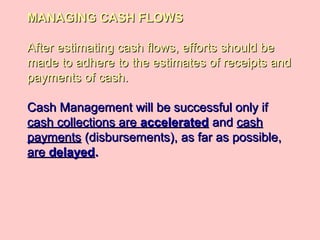

![SELECTIVE CONTROL OF INVENTORYSELECTIVE CONTROL OF INVENTORY

Different classification methodsDifferent classification methods

ClassificationClassification BasisBasis

ABCABC

[Always Better Control ][Always Better Control ]

Value of items consumedValue of items consumed

VEDVED

[ Vital, Essential,[ Vital, Essential,

Desirable ]Desirable ]

The importance orThe importance or

criticalitycriticality

FSNFSN

[ Fast-moving, Slow-[ Fast-moving, Slow-

moving, Non-moving ]moving, Non-moving ]

The pace at which theThe pace at which the

material movesmaterial moves

HMLHML

[ High, Medium, Low ][ High, Medium, Low ]

Unit price of materialsUnit price of materials

SDESDE

[ Scarce, Difficult, Easy ][ Scarce, Difficult, Easy ]

Procurement DifficultiesProcurement Difficulties

XYZ Value of items in storage](https://image.slidesharecdn.com/workingcapitalppt-170411070330/85/Working-capital-ppt-66-320.jpg)

The document provides an overview of working capital, including definitions, concepts, and management. It defines working capital as the capital required for financing short-term assets like cash, inventory, and receivables. There are two concepts of working capital - the balance sheet concept focuses on current assets and liabilities, while the operating cycle concept looks at cash flows through purchasing, production, and sales cycles. Proper management of working capital is important, as both excess and inadequate working capital can hurt a business. Factors like industry, sales, and inventory turnover affect working capital needs. Forecasting and estimating working capital requirements involves considering items like materials, production timelines, credit terms, and cash flows.