Downloaded 107 times

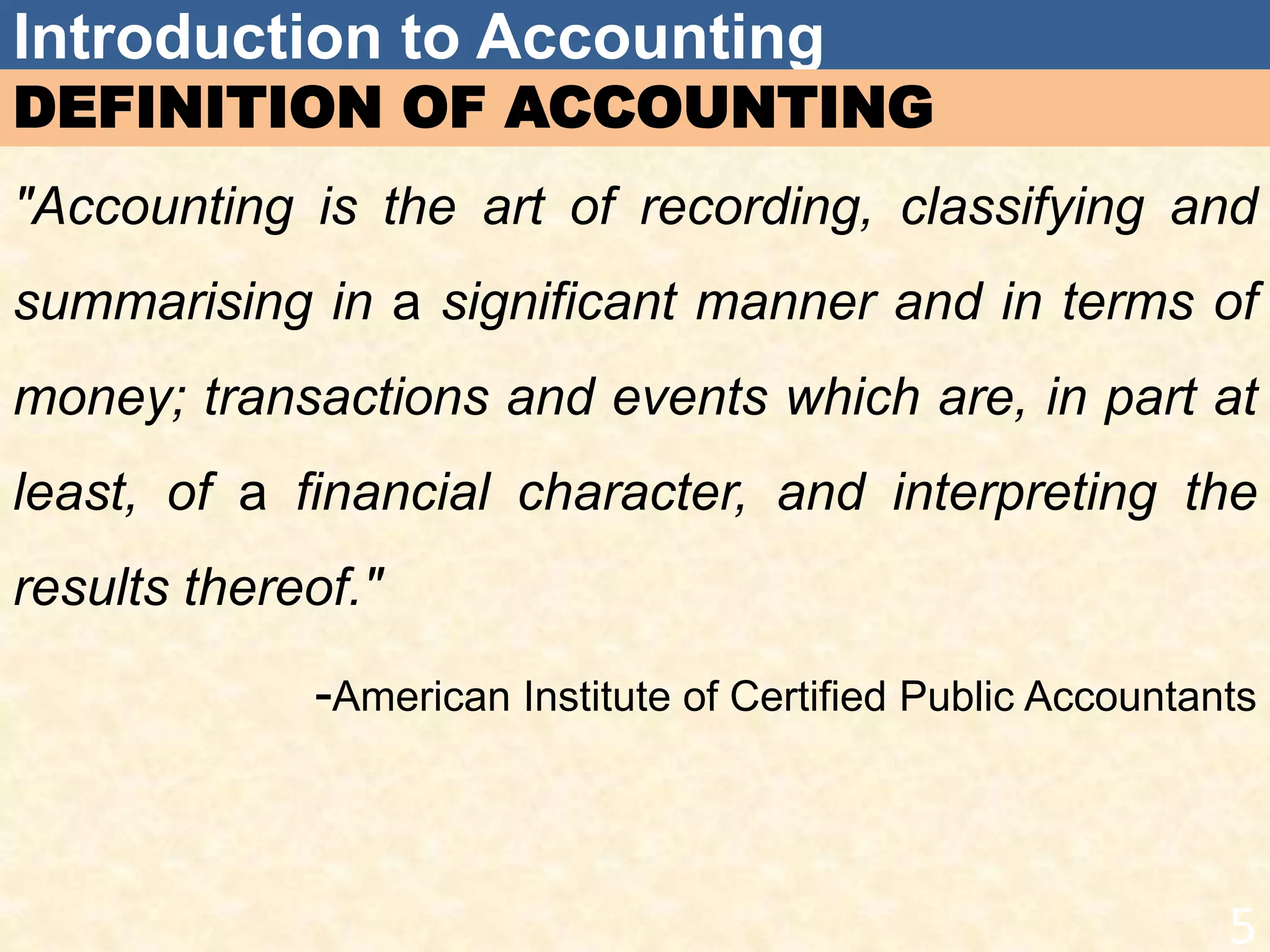

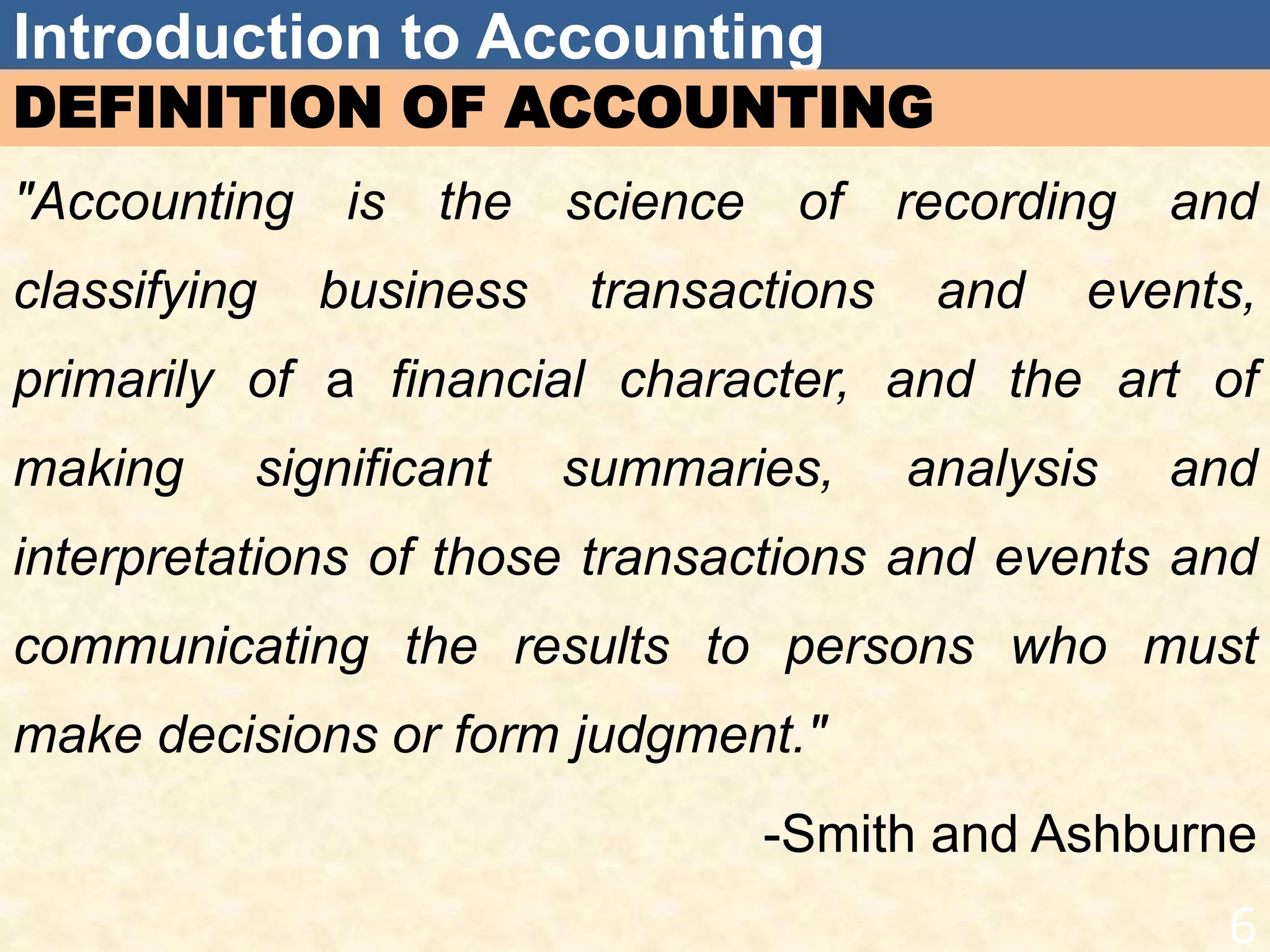

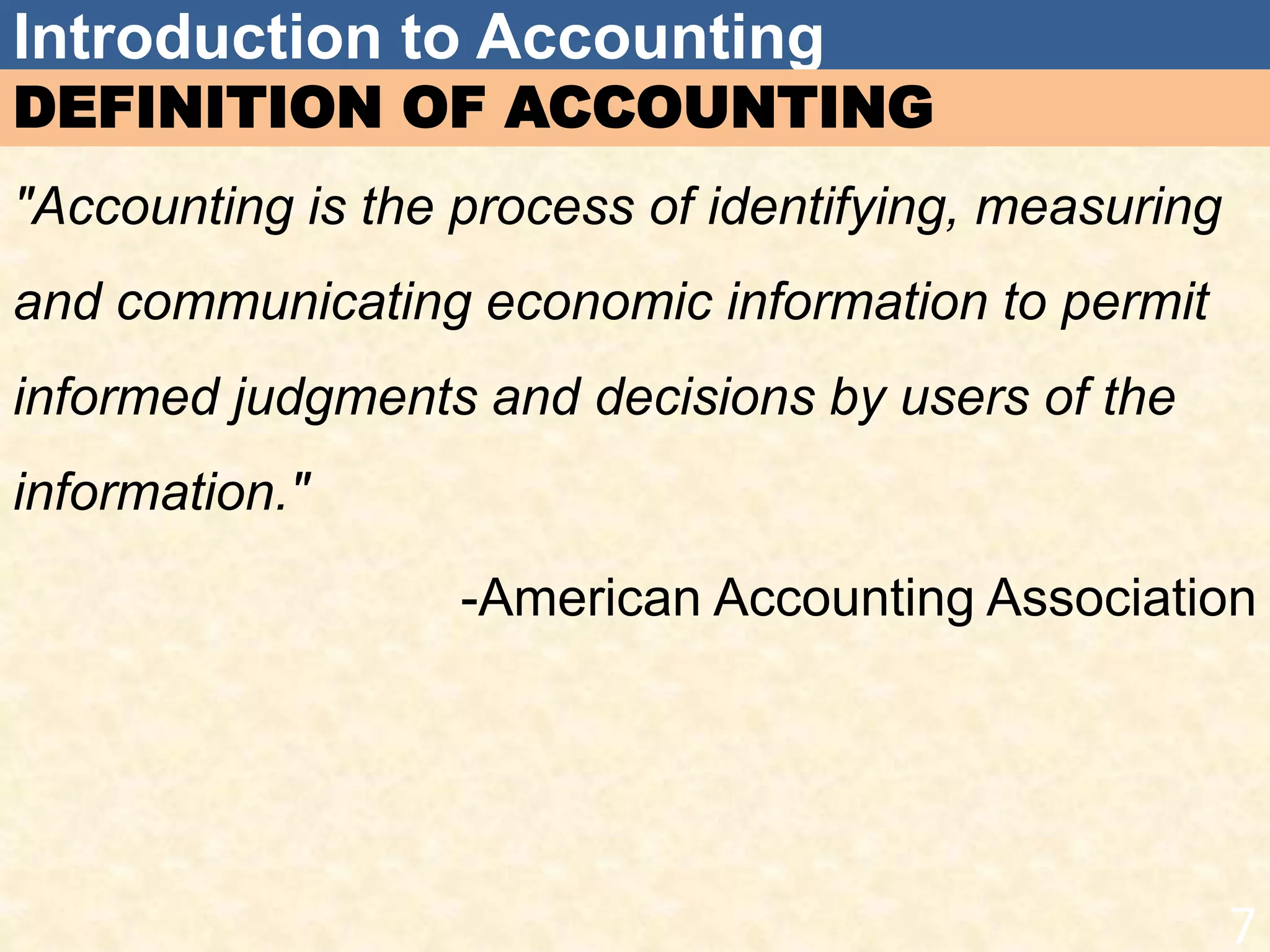

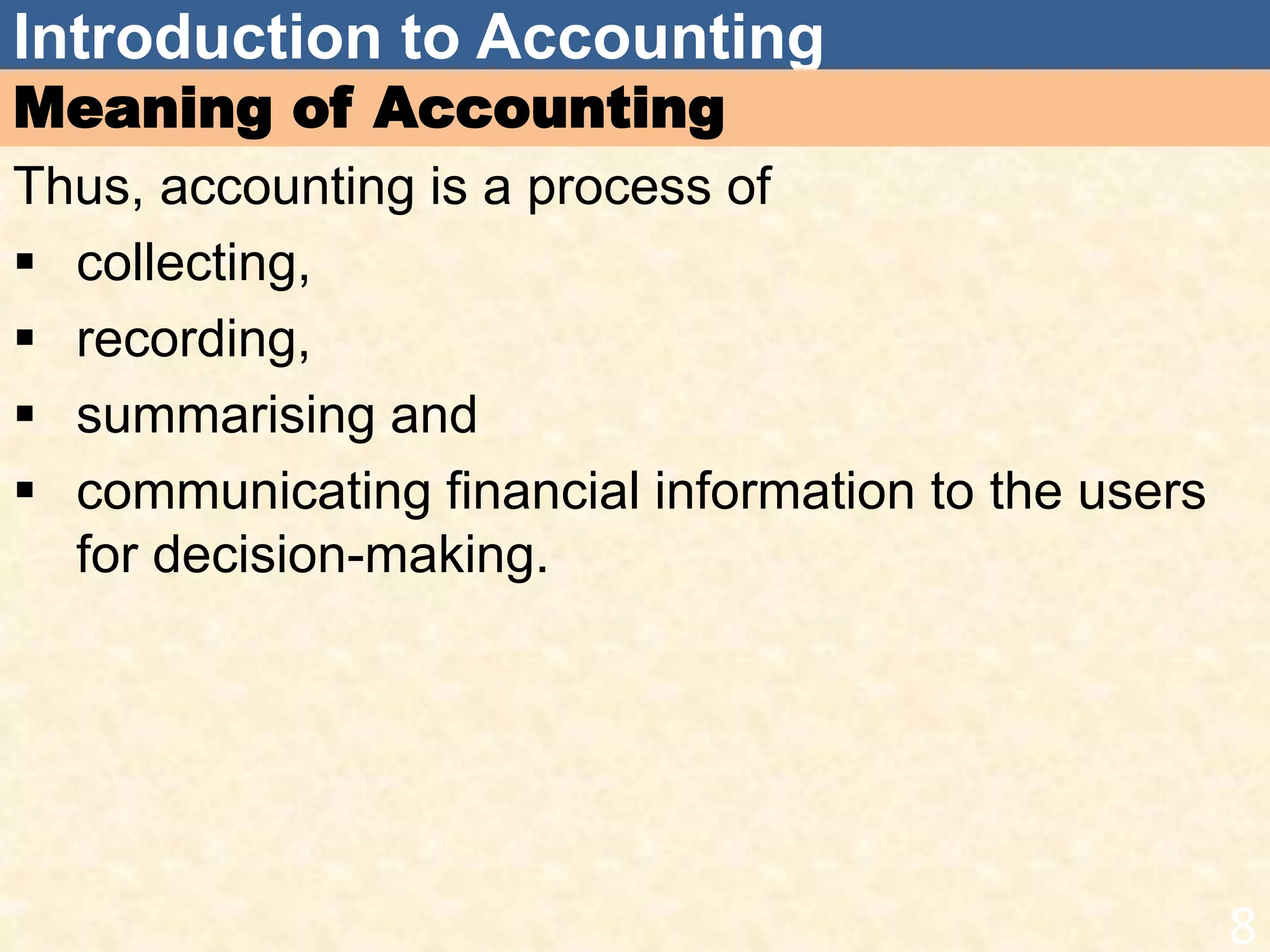

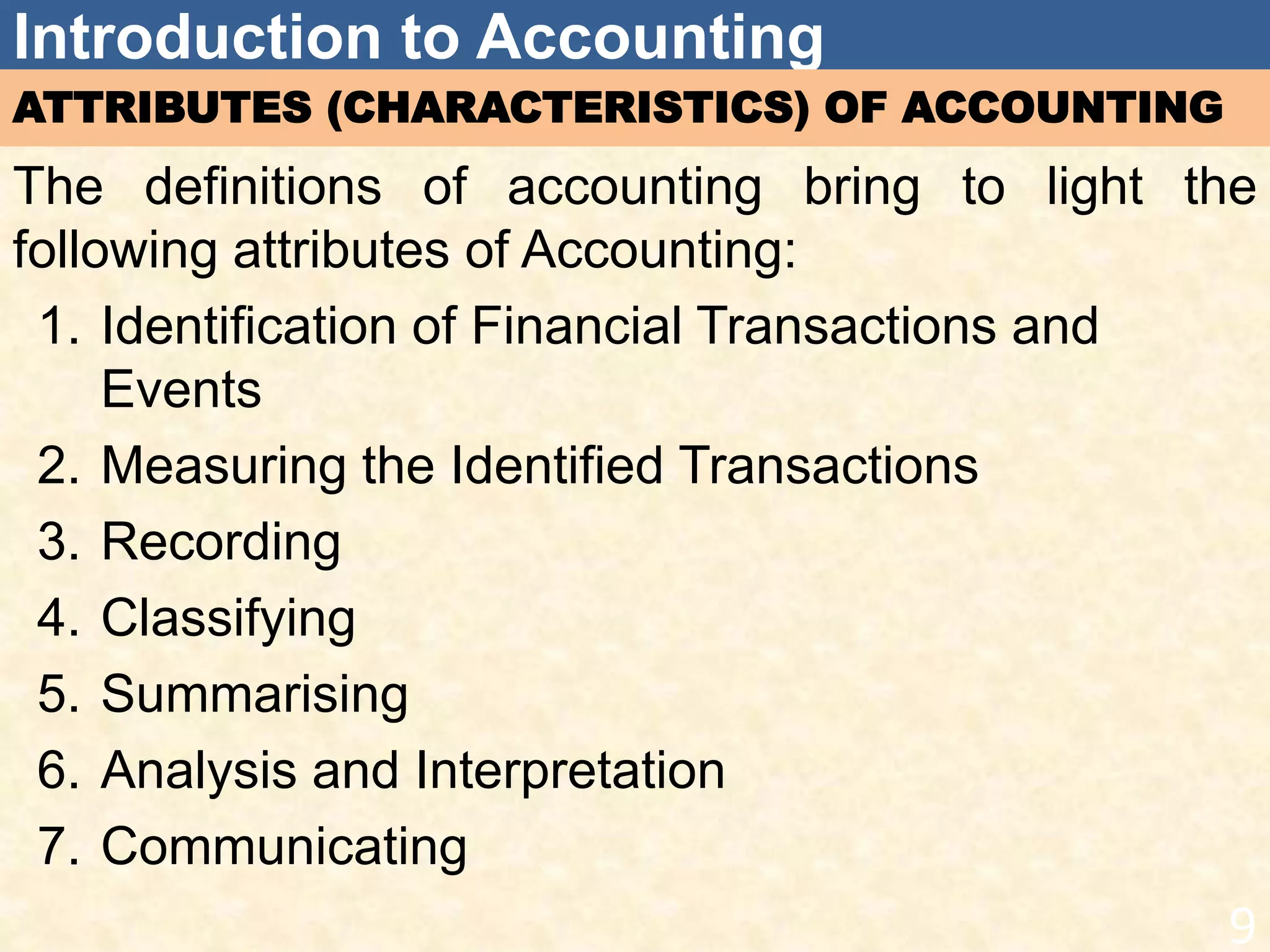

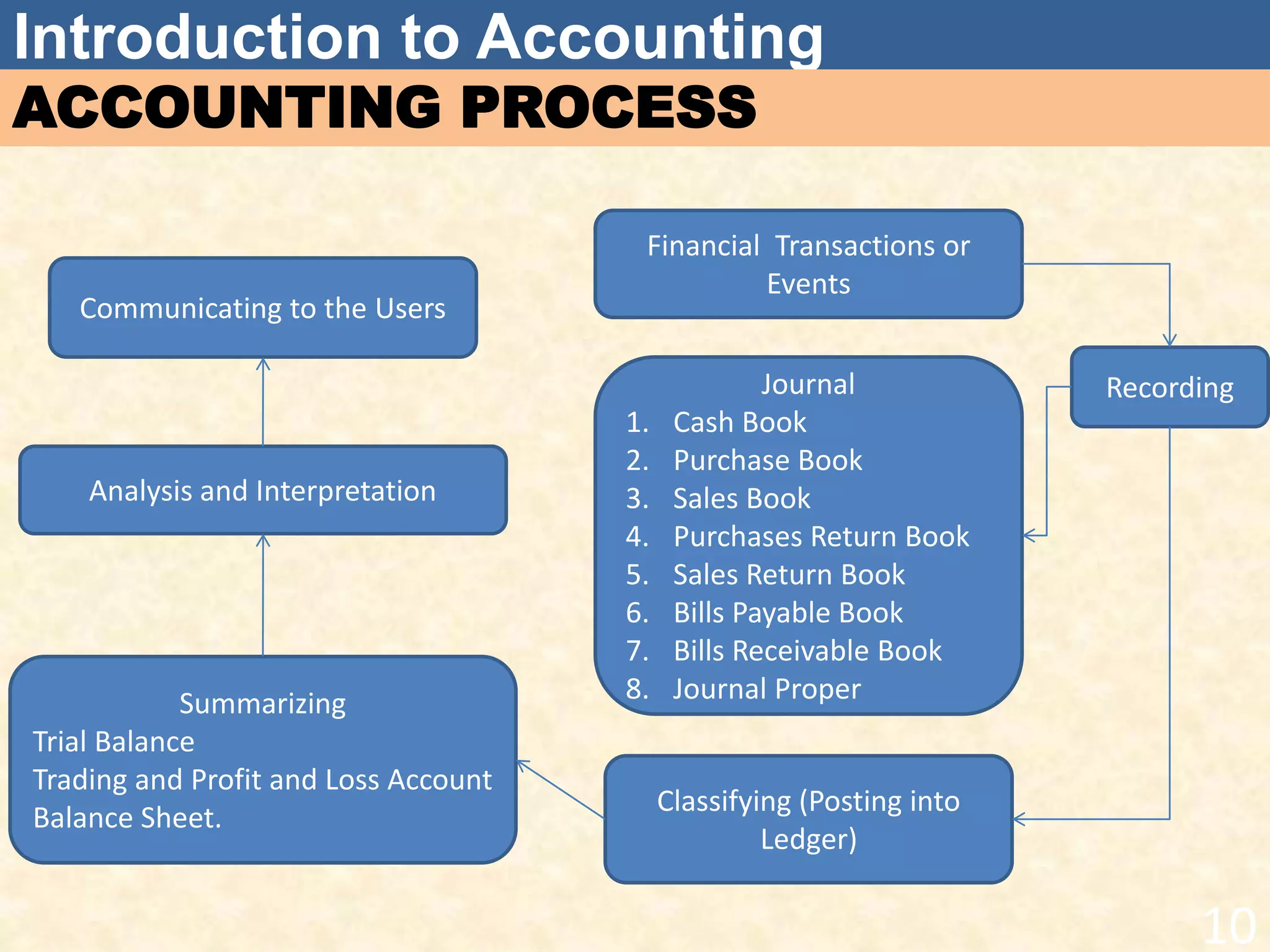

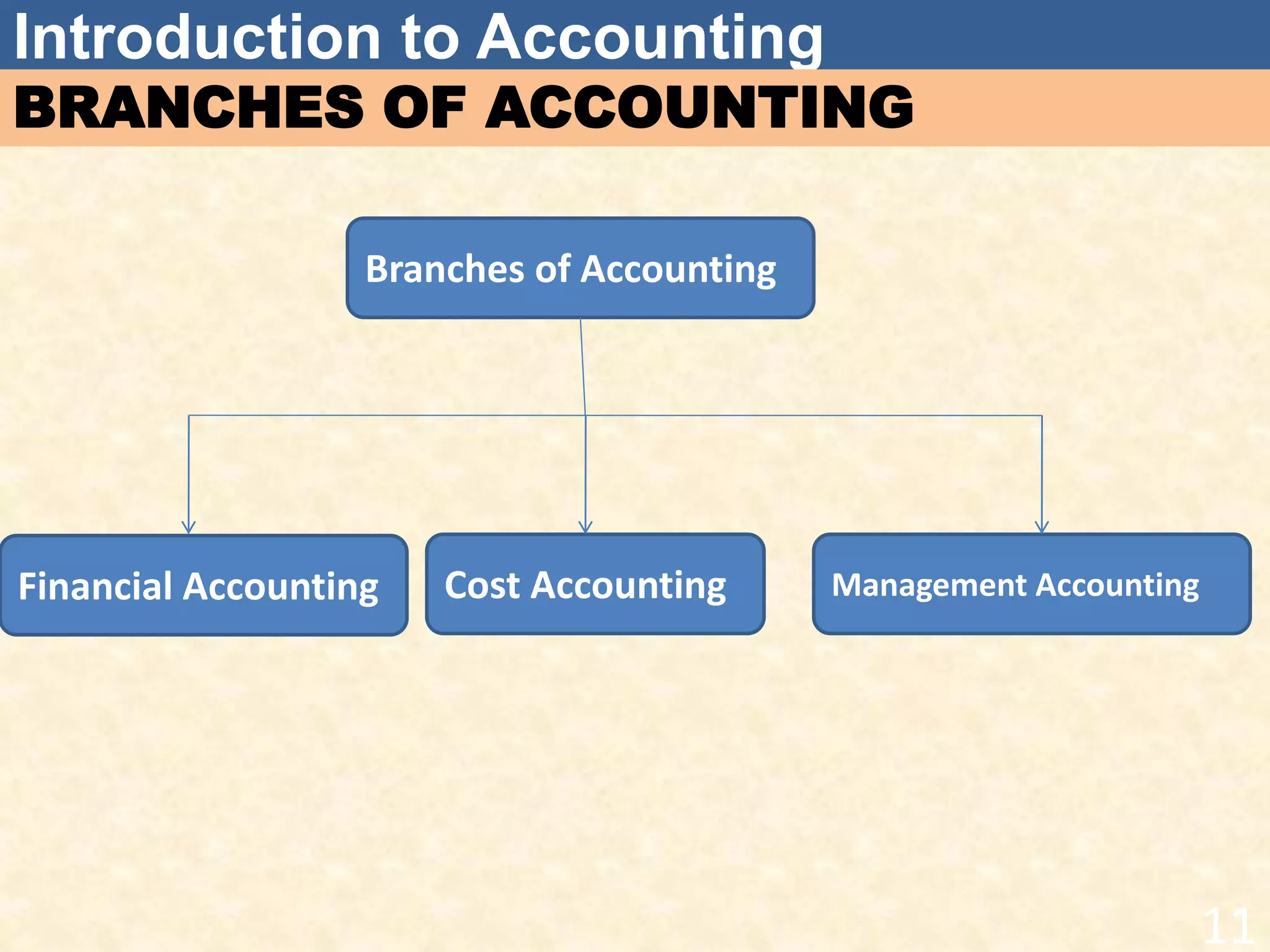

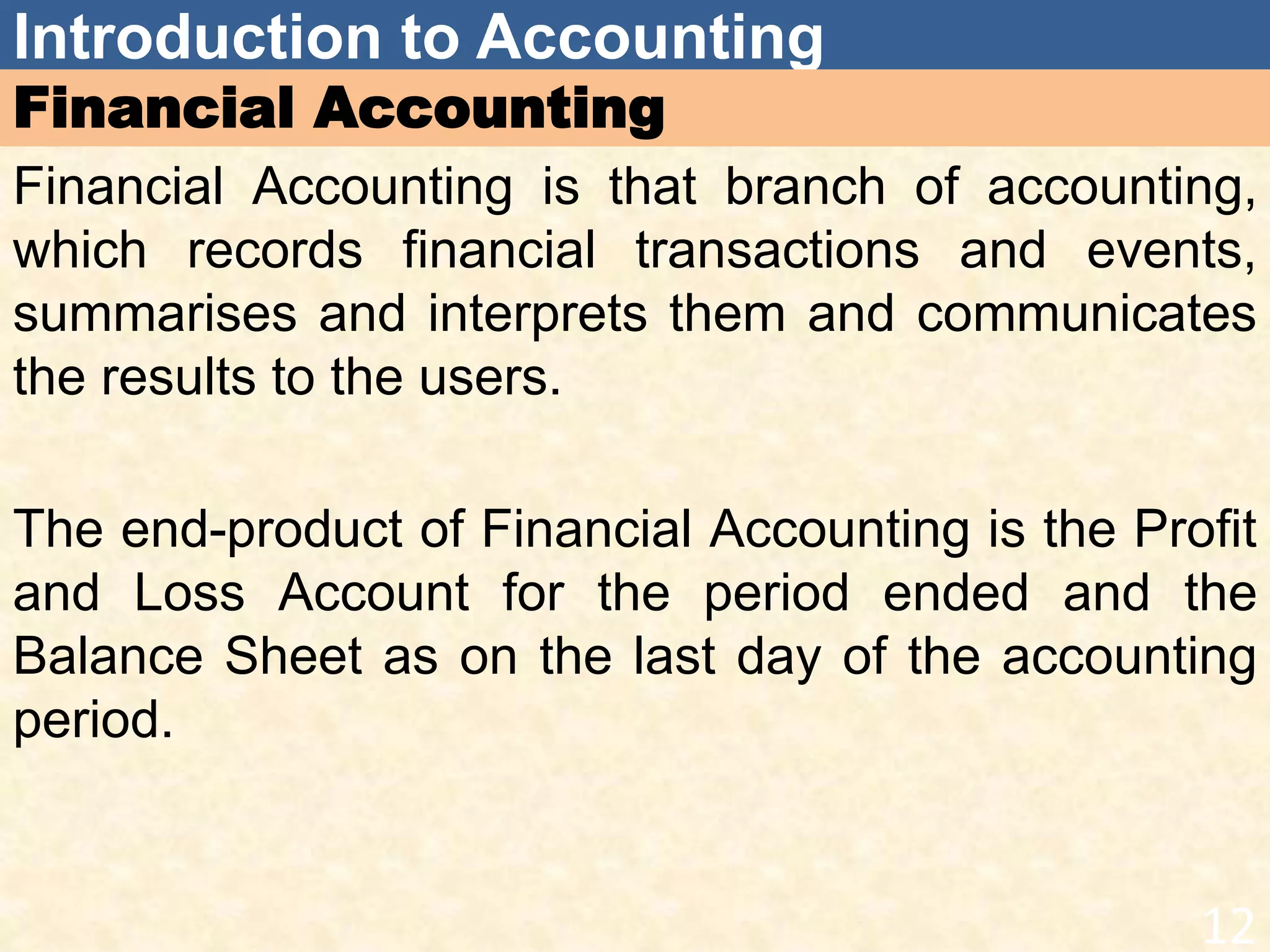

The document provides an introduction to the key concepts of accounting, including: 1. Accounting is defined as the process of recording, classifying, summarizing and communicating financial information to allow for informed decision making. 2. The main branches of accounting are financial accounting, cost accounting, and management accounting. Financial accounting provides financial statements, cost accounting determines product costs, and management accounting aids decision making. 3. The accounting process involves identifying transactions, recording them, classifying posts in ledger accounts, summarizing, analyzing, and communicating results. Double-entry bookkeeping is the standard system used. 4. Accounting objectives are to maintain records, determine profit/loss, financial position, assist management

![MEFA_UNIT-IV_Part-1[1].pptx kkkkkkkkkkkkkkkkkkkkkkk](https://cdn.slidesharecdn.com/ss_thumbnails/mefaunit-ivpart-11-250504093650-39e41996-thumbnail.jpg?width=640&height=640&fit=bounds)