Working Capital Management

Over view of working capital management.

Cash and marketable securities management.

Accounts receivable and inventory

management.

Short-term financing

Overview of WorkingCapital

Management

• Working Capital Concepts

• Working Capital Issues

• Financing Current Assets: Short-Term

and Long-Term Mix

• Combining Liability Structure and

Current Asset Decisions

4.

Working capital Introduction

•Working capital typically means the firm’s

holding of current or short-term assets such

as cash, receivables, inventory and

marketable securities.

• These items are also referred to as

circulating capital

• Corporate executives devote a considerable

amount of attention to the management of

working capital.

5.

What is workingcapital?

Current assets, which represent the

portion of investment that circulates from one

form to another in the ordinary conduct of

business.

Current assets, commonly called working

capital

6.

Working Capital Concepts

NetWorking Capital: (

(Current Assets- Current

Liabilities) The difference between Current

assets and current liabilities is called working capital.

If current assets > current liabilites is called surplus

or vice a versa. This is one measure of the extent to

which the firm is protected from liquidity problems

Gross Working Capital

The firm’s investment in current assets. like cash

and marketable securities, receivables, and

inventory).

7.

Working Capital Management

WorkingCapital Management

The administration of the firm’s current

assets and the financing needed to support

current assets is called working capital

management or short term financial

management.

Simply management of current assets

and current liabilities.

8.

Significance of WorkingCapital

Management

• In a typical manufacturing firm, current assets

exceed one-half of total assets.

• Excessive levels can result in a substandard

Return on Investment (ROI).

• Current liabilities are the principal source of

external financing for small firms.

• Requires continuous, day-to-day managerial

supervision.

• Working capital management affects the

company’s risk, return, and share price.

9.

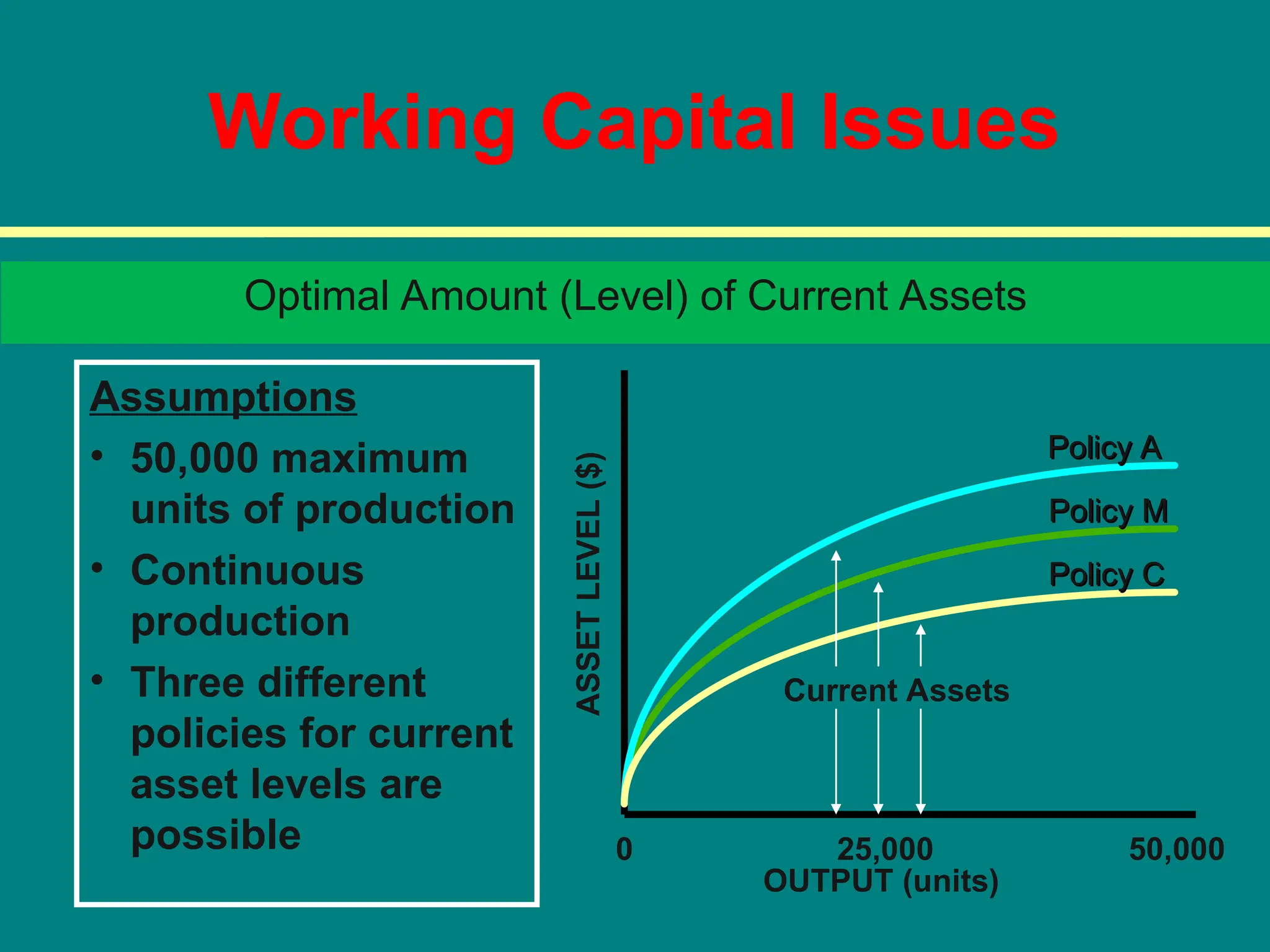

Working Capital Issues

Assumptions

•50,000 maximum

units of production

• Continuous

production

• Three different

policies for current

asset levels are

possible

Optimal Amount (Level) of Current Assets

0 25,000 50,000

OUTPUT (units)

ASSET

LEVEL

($)

Current Assets

Policy C

Policy C

Policy A

Policy A

Policy M

Policy M

10.

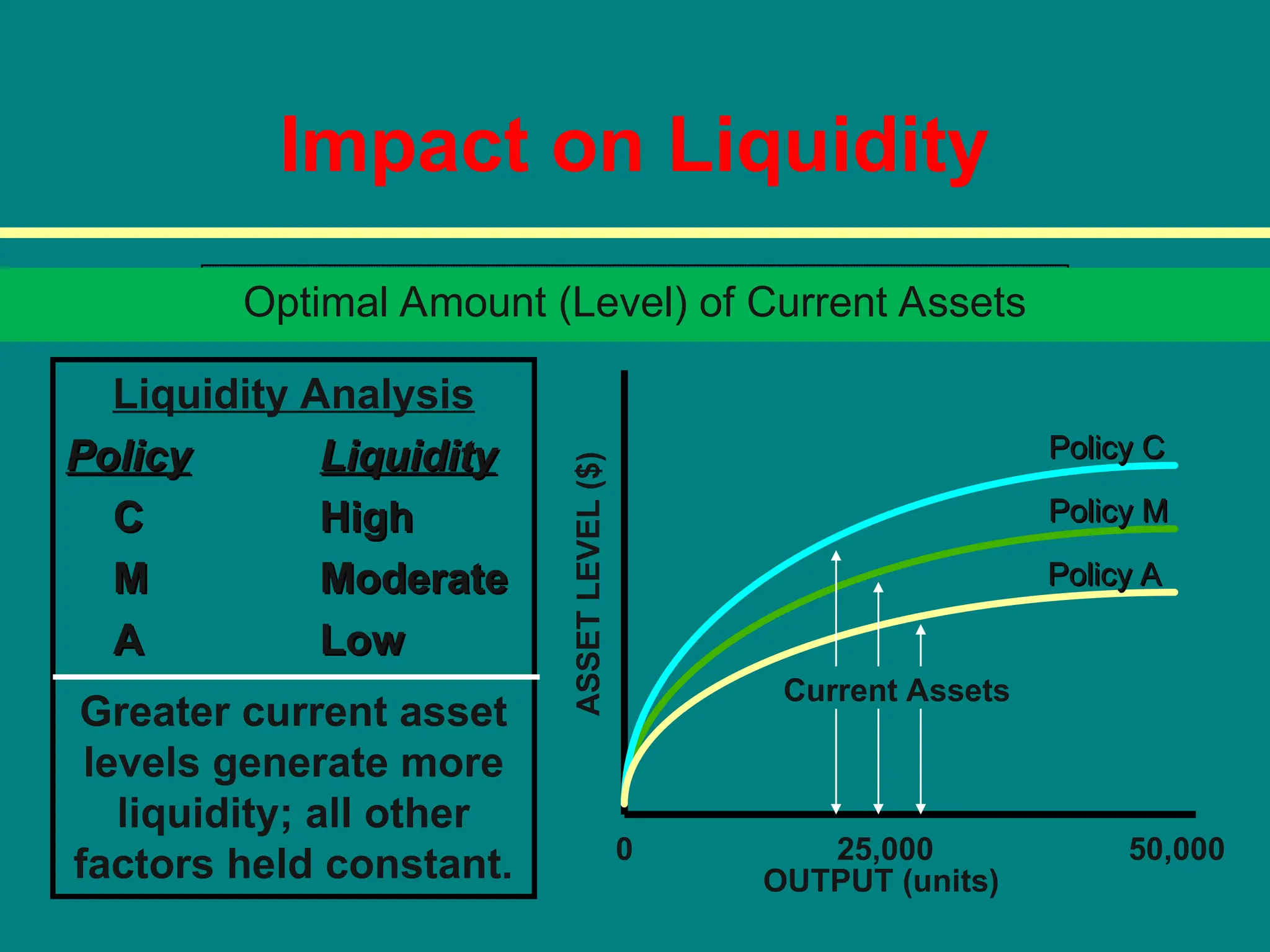

Impact on Liquidity

LiquidityAnalysis

Policy

Policy Liquidity

Liquidity

C

C High

High

M

M Moderate

Moderate

A

A Low

Low

Greater current asset

levels generate more

liquidity; all other

factors held constant.

Optimal Amount (Level) of Current Assets

0 25,000 50,000

OUTPUT (units)

ASSET

LEVEL

($)

Current Assets

Policy A

Policy A

Policy C

Policy C

Policy M

Policy M

11.

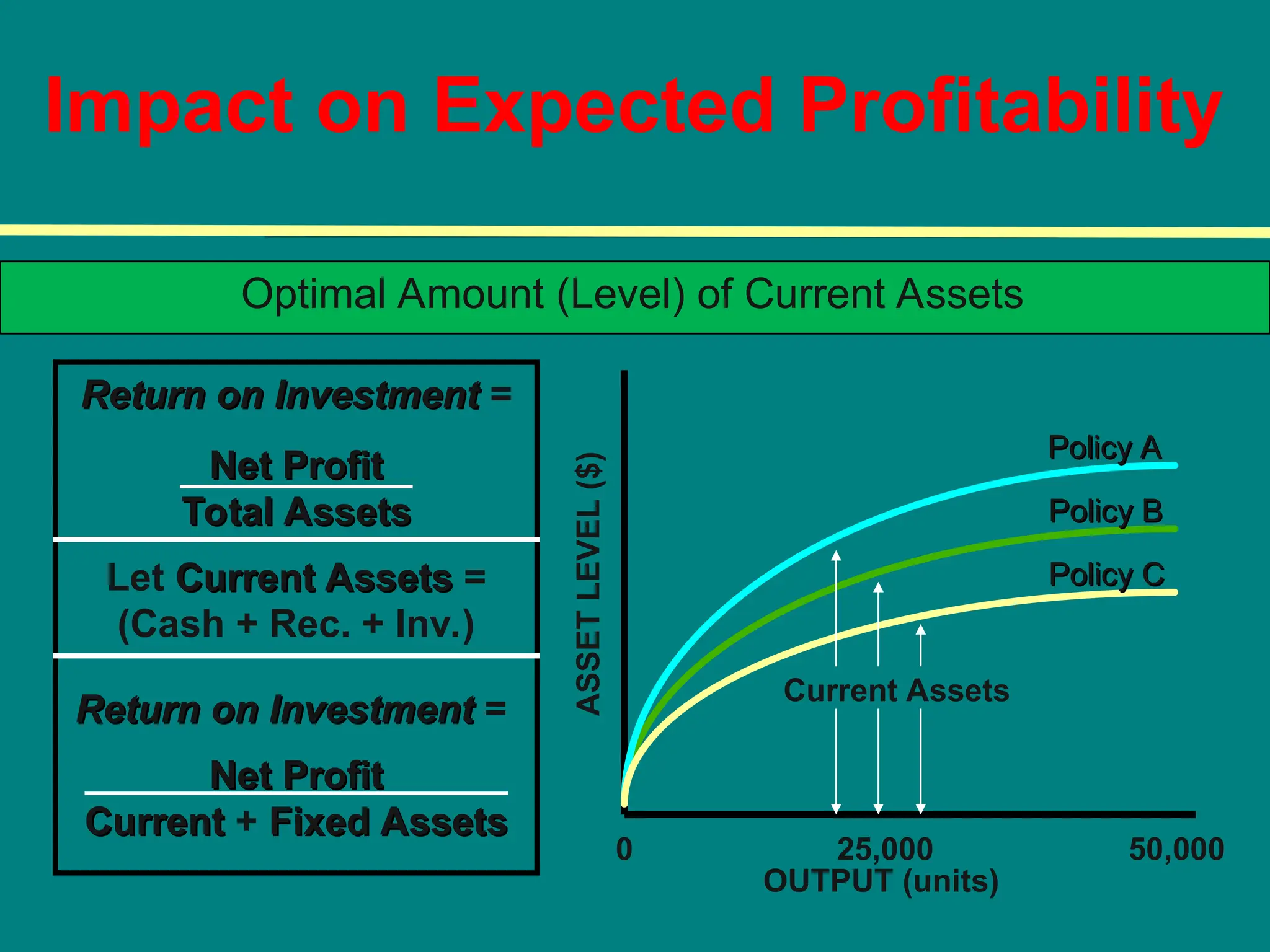

Impact on ExpectedProfitability

Return on Investment

Return on Investment =

Net Profit

Net Profit

Total Assets

Total Assets

Let Current Assets

Current Assets =

(Cash + Rec. + Inv.)

Return on Investment

Return on Investment =

Net Profit

Net Profit

Current

Current + Fixed Assets

Fixed Assets

Optimal Amount (Level) of Current Assets

0 25,000 50,000

OUTPUT (units)

ASSET

LEVEL

($)

Current Assets

Policy C

Policy C

Policy A

Policy A

Policy B

Policy B

12.

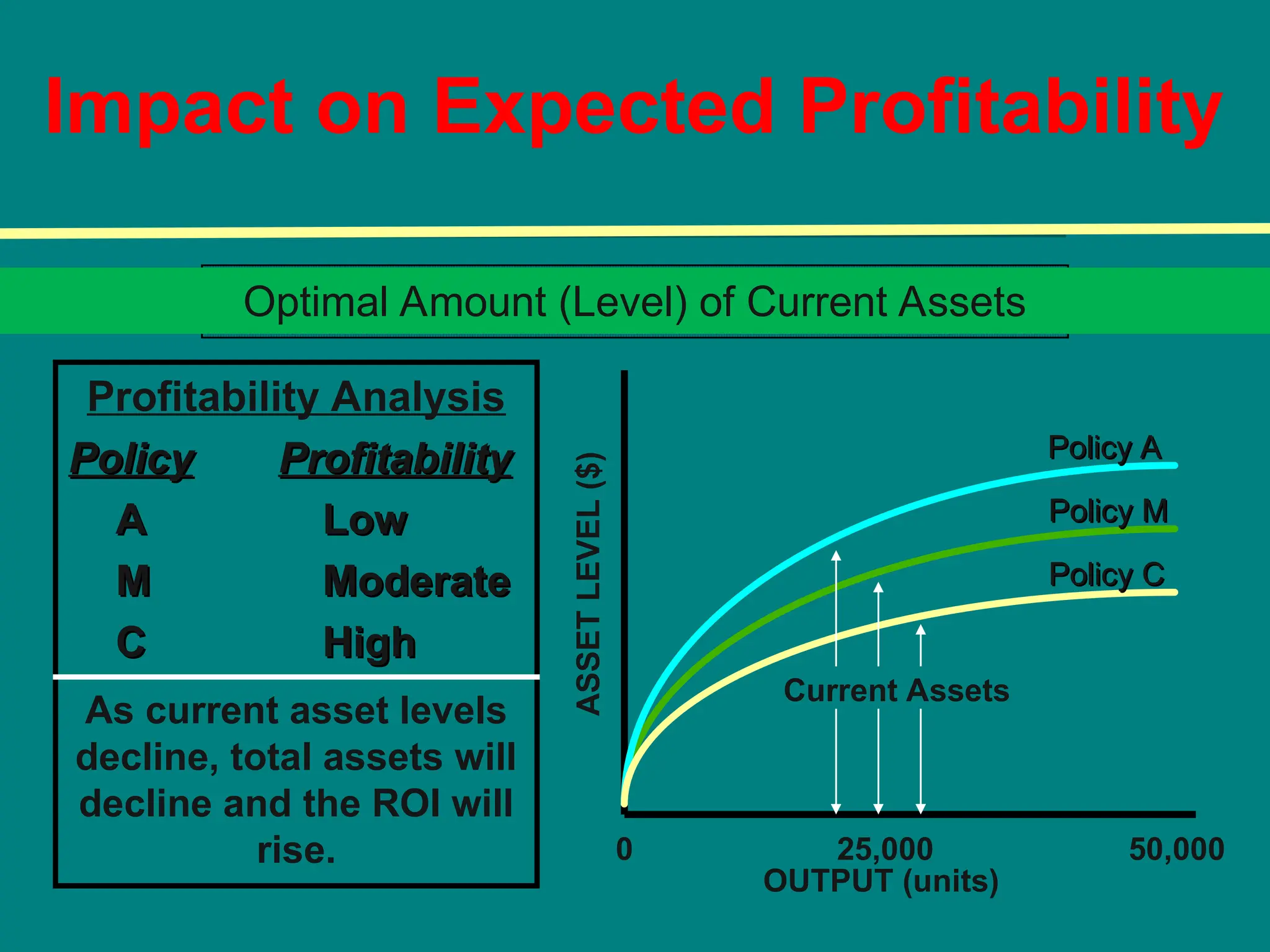

Impact on ExpectedProfitability

Profitability Analysis

Policy

Policy Profitability

Profitability

A

A Low

Low

M

M Moderate

Moderate

C

C High

High

As current asset levels

decline, total assets will

decline and the ROI will

rise.

Optimal Amount (Level) of Current Assets

0 25,000 50,000

OUTPUT (units)

ASSET

LEVEL

($)

Current Assets

Policy C

Policy C

Policy A

Policy A

Policy M

Policy M

13.

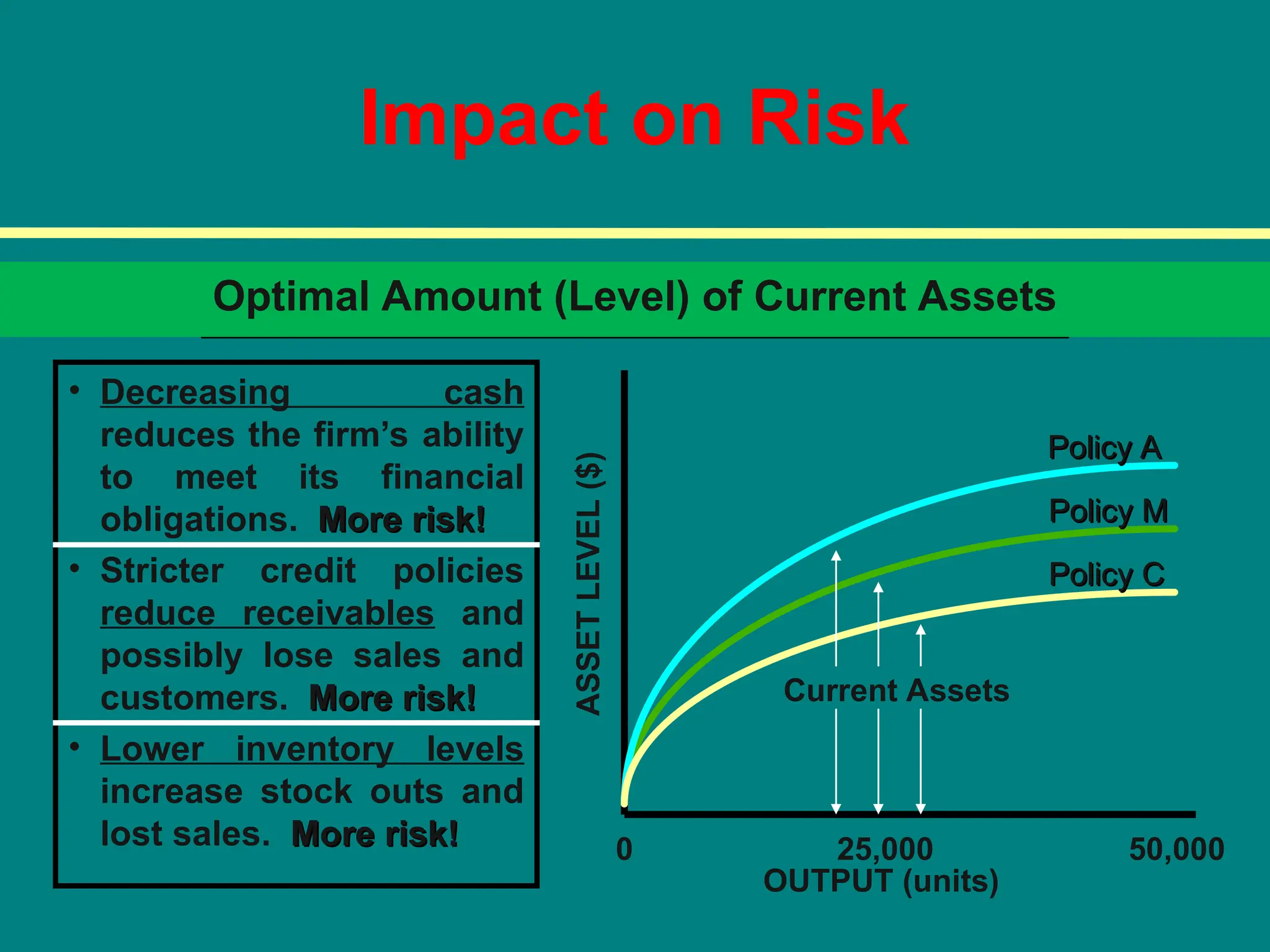

Impact on Risk

•Decreasing cash

reduces the firm’s ability

to meet its financial

obligations. More risk!

More risk!

• Stricter credit policies

reduce receivables and

possibly lose sales and

customers. More risk!

More risk!

• Lower inventory levels

increase stock outs and

lost sales. More risk!

More risk!

Optimal Amount (Level) of Current Assets

0 25,000 50,000

OUTPUT (units)

ASSET

LEVEL

($)

Current Assets

Policy C

Policy C

Policy A

Policy A

Policy M

Policy M

14.

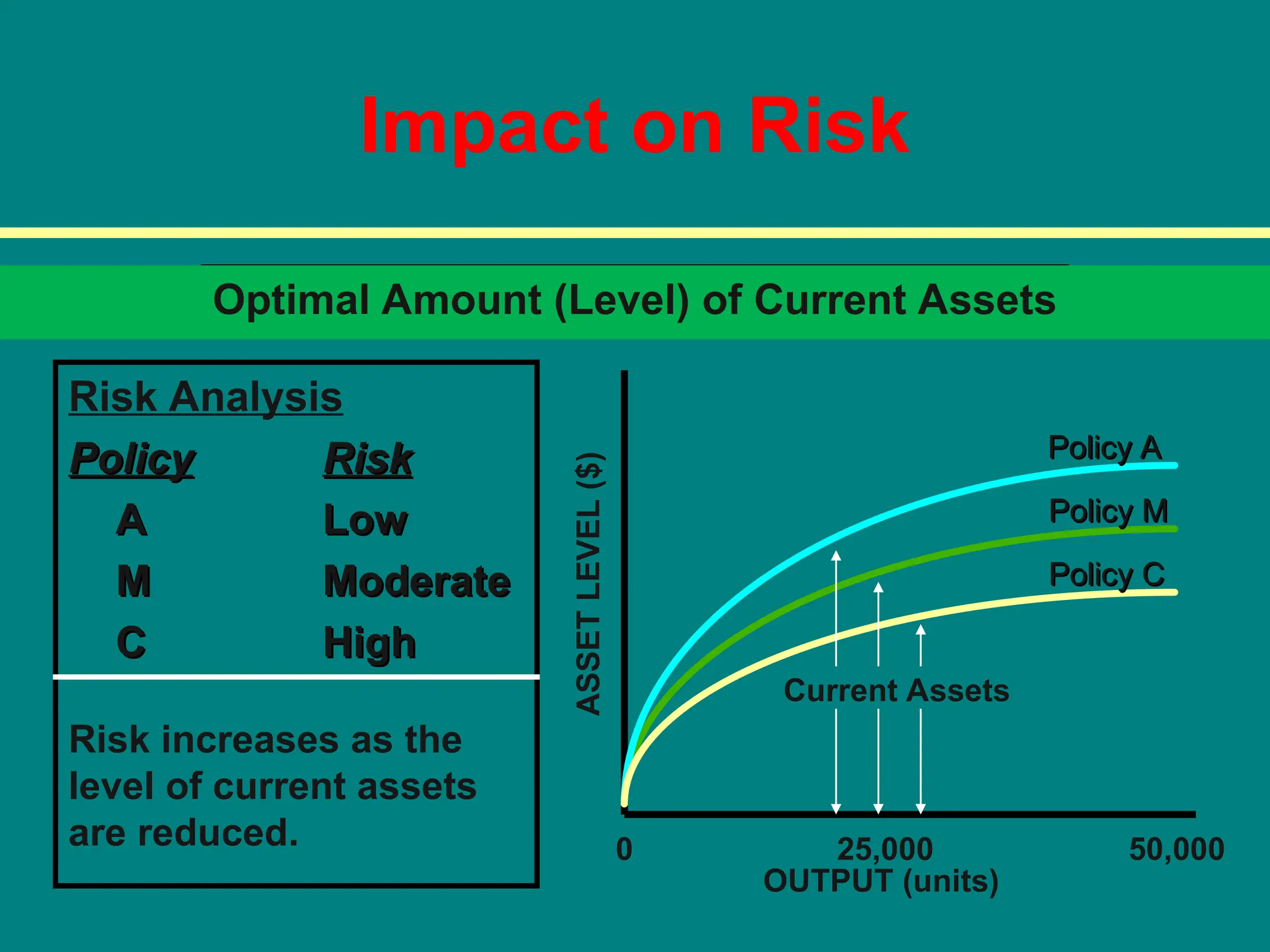

Impact on Risk

RiskAnalysis

Policy

Policy Risk

Risk

A

A Low

Low

M

M Moderate

Moderate

C

C High

High

Risk increases as the

level of current assets

are reduced.

Optimal Amount (Level) of Current Assets

0 25,000 50,000

OUTPUT (units)

ASSET

LEVEL

($)

Current Assets

Policy C

Policy C

Policy A

Policy A

Policy M

Policy M

15.

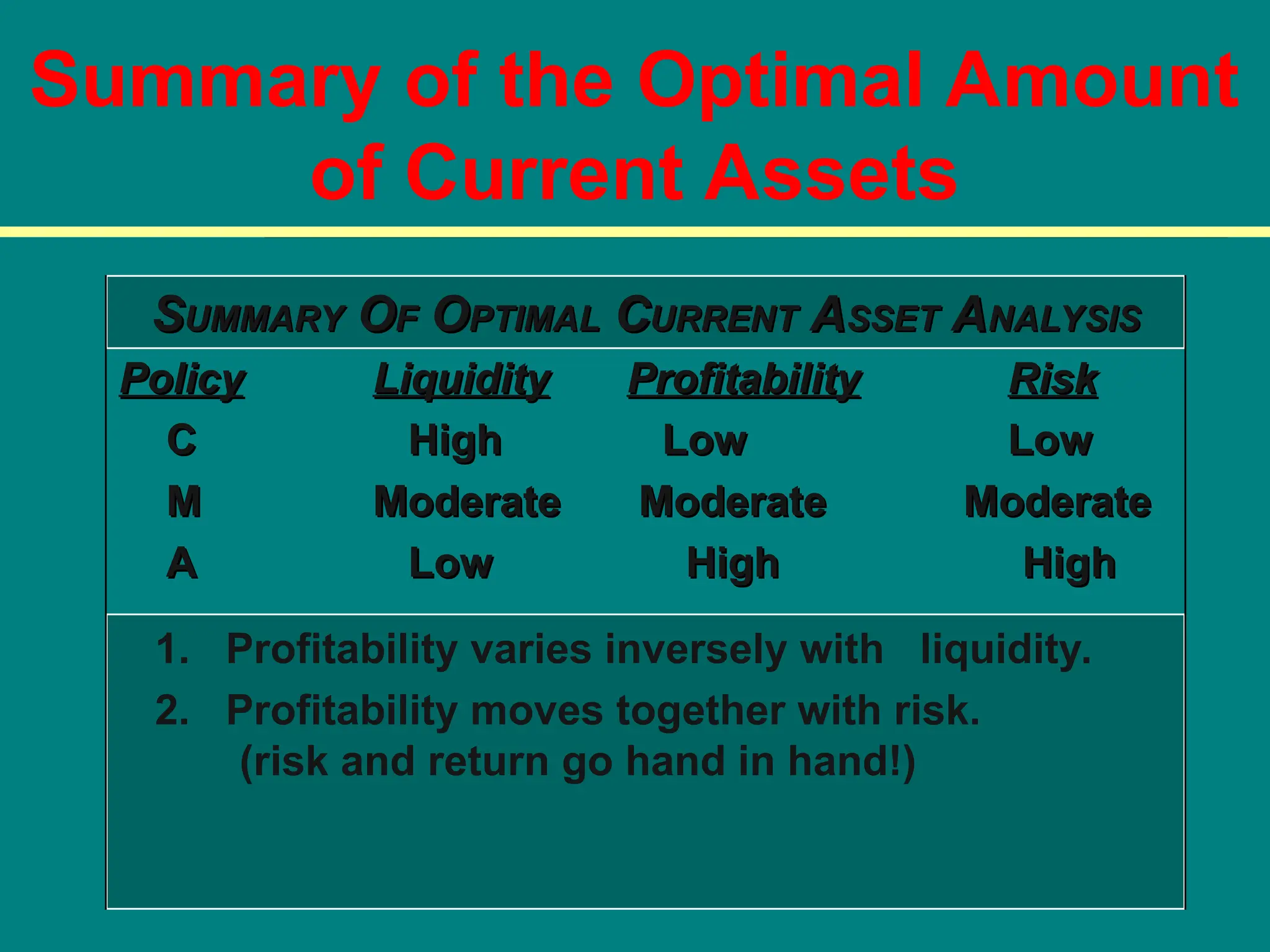

Summary of theOptimal Amount

of Current Assets

S

SUMMARY

UMMARY O

OF

F O

OPTIMAL

PTIMAL C

CURRENT

URRENT A

ASSET

SSET A

ANALYSIS

NALYSIS

Policy

Policy Liquidity

Liquidity Profitability

Profitability Risk

Risk

C

C High

High Low

Low Low

Low

M

M Moderate

Moderate Moderate

Moderate Moderate

Moderate

A

A Low

Low High

High High

High

1. Profitability varies inversely with liquidity.

2. Profitability moves together with risk.

(risk and return go hand in hand!)

16.

Classifications of Working

Capital

•Time

Time

– Permanent Current Assets

– Temporary Short Time Investment or

Marketable Securities

Components

Components

Cash, marketable securities,

receivables, and inventory

17.

Permanent Working Capital

Theamount of current assets required to meet a firm’s

long-term minimum needs. You might call this “bare bones”

working capital.

Permanent working capital is similar to the firm’s fixed

assets in two important respects. First, the dollar investment

is long term, despite the seeming contradiction that the

assets being financed are called “current.” Second, for a

growing firm, the level of permanent work ing capital needed

will increase over time in the same way that a firm’s fixed

assets will need to increase over time. However, permanent

working capital is different from fixed assets in one very

important respect – it is constantly changing.

18.

Temporary Working Capital

Theamount of current assets that varies with

seasonal requirements.

Like permanent working capital, temporary

working capital also consists of current assets in a

constantly changing form. However, because the

need for this portion of the firm’s total current

assets is seasonal, we may want to consider

financing this level of current assets from a source

which can itself be seasonal or temporary in nature.

19.

Financing Current Assets:Short-Term

and Long-Term Mix

Spontaneous Financing

Spontaneous Financing:

: Trade credit, and

other payables and accruals, that arise

spontaneously in the firm’s day-to-day

operations.

– Based on policies regarding payment for

purchases, labor, taxes, and other expenses.

– We are concerned with managing non-

spontaneous financing of assets.

20.

Hedging (or MaturityMatching)

Approach

A method of financing where each asset would

be offset with a financing instrument of the same

approximate maturity.

21.

Financing Needs and

theHedging Approach

• Fixed assets and the non-seasonal portion of

current assets are financed with long-term debt

and equity (long-term profitability of assets to

cover the long-term financing costs of the firm).

• Seasonal needs are financed with short-term

loans (under normal operations sufficient cash

flow is expected to cover the short-term financing

cost).

22.

Self-Liquidating Nature of

Short-TermLoans

• Seasonal orders require the purchase of inventory

beyond current levels.

• Increased inventory is used to meet the increased

demand for the final product.

• Sales become receivables.

• Receivables are collected and become cash.

• The resulting cash funds can be used to pay off

the seasonal short-term loan and cover associated

long-term financing costs.

23.

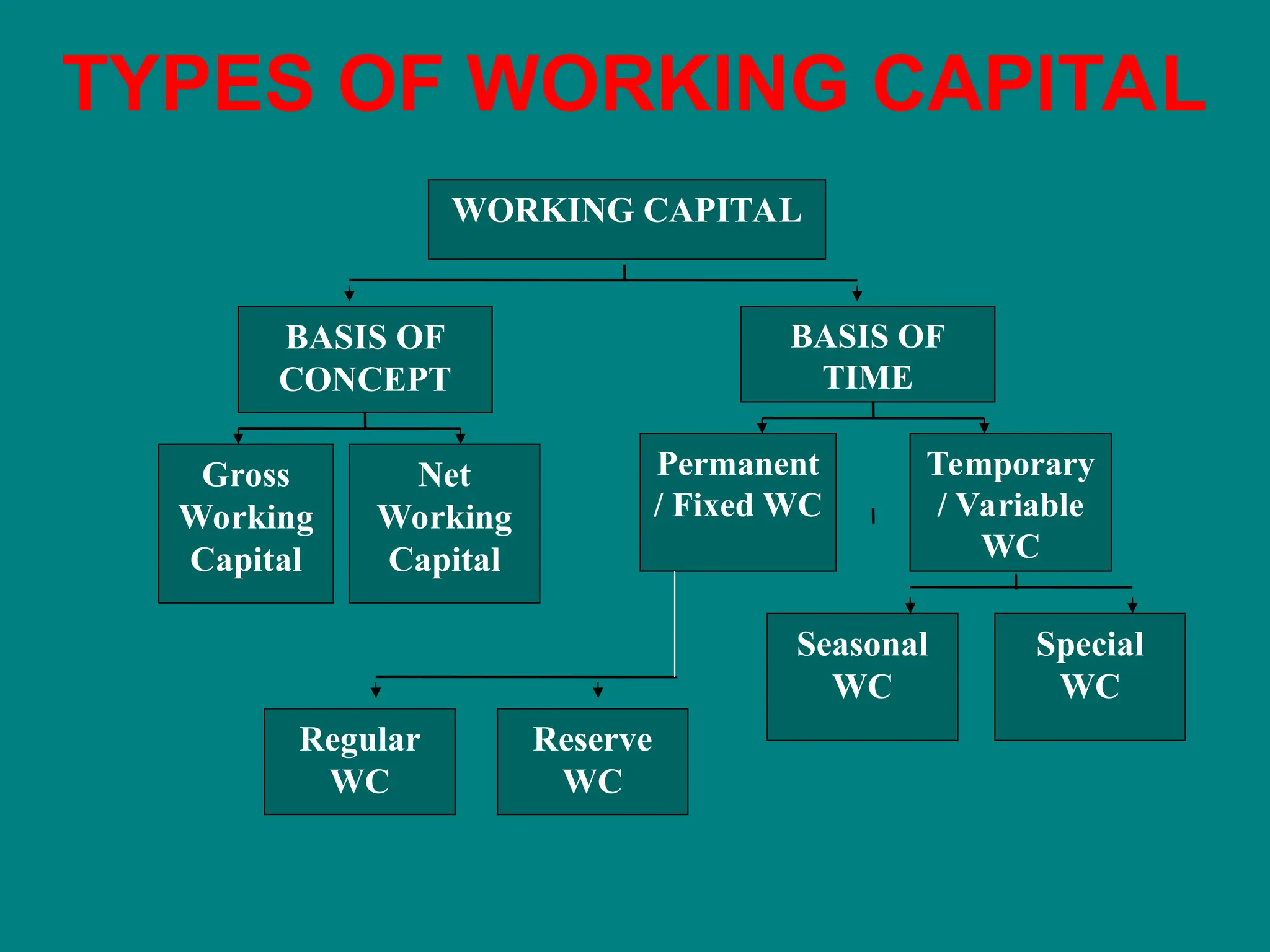

TYPES OF WORKINGCAPITAL

WORKING CAPITAL

BASIS OF

CONCEPT

BASIS OF

TIME

Gross

Working

Capital

Net

Working

Capital

Permanent

/ Fixed WC

Temporary

/ Variable

WC

Regular

WC

Reserve

WC

Special

WC

Seasonal

WC

24.

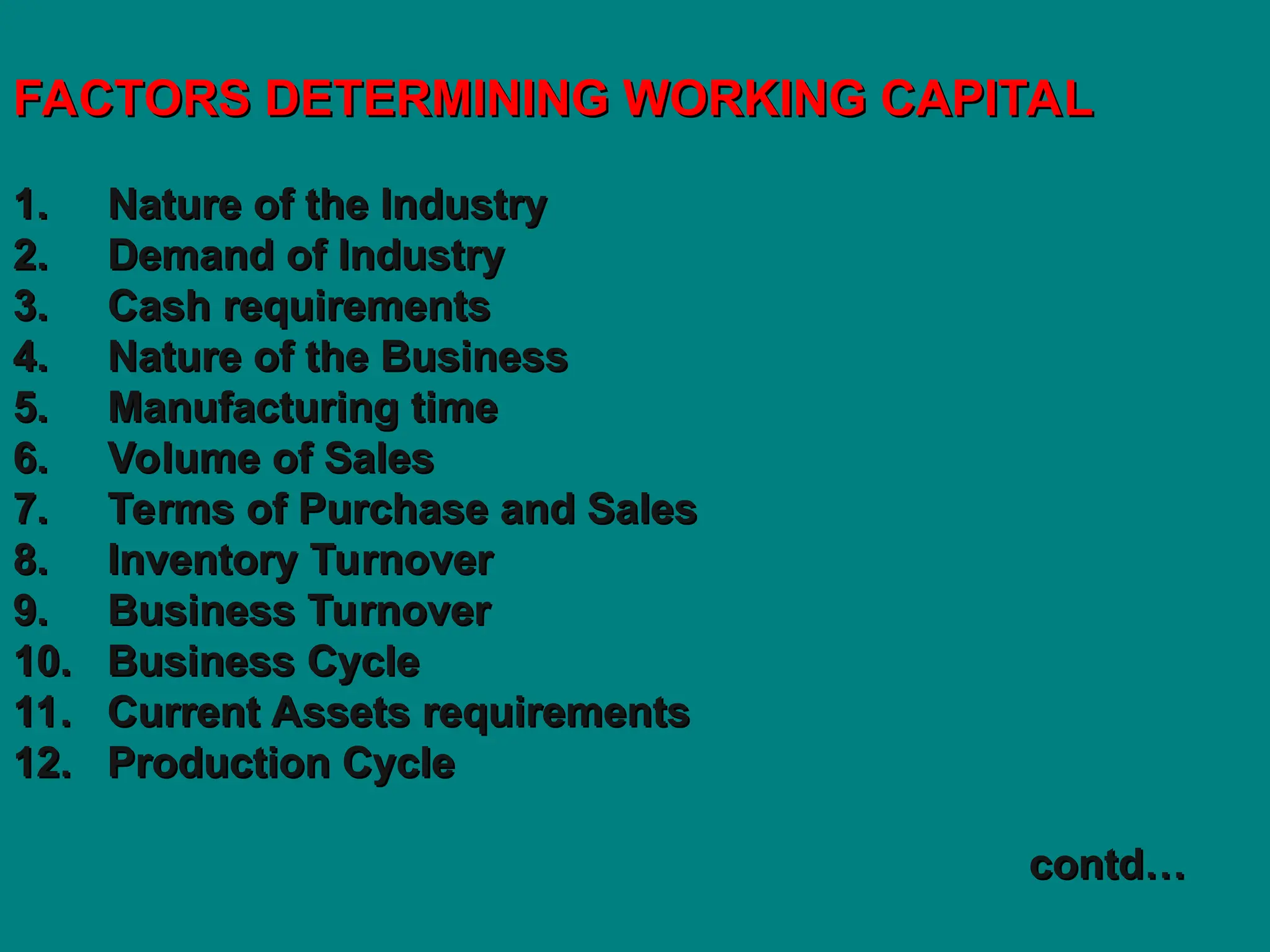

FACTORS DETERMINING WORKINGCAPITAL

FACTORS DETERMINING WORKING CAPITAL

1. Nature of the Industry

1. Nature of the Industry

2. Demand of Industry

2. Demand of Industry

3. Cash requirements

3. Cash requirements

4. Nature of the Business

4. Nature of the Business

5. Manufacturing time

5. Manufacturing time

6. Volume of Sales

6. Volume of Sales

7. Terms of Purchase and Sales

7. Terms of Purchase and Sales

8. Inventory Turnover

8. Inventory Turnover

9. Business Turnover

9. Business Turnover

10. Business Cycle

10. Business Cycle

11. Current Assets requirements

11. Current Assets requirements

12. Production Cycle

12. Production Cycle

contd…

contd…

25.

Working Capital Determinants(Contd…)

Working Capital Determinants (Contd…)

13. Credit control

13. Credit control

14. Inflation or Price level changes

14. Inflation or Price level changes

15. Profit planning and control

15. Profit planning and control

16. Repayment ability

16. Repayment ability

17. Cash reserves

17. Cash reserves

18. Operation efficiency

18. Operation efficiency

19. Change in Technology

19. Change in Technology

20. Firm’s finance and dividend policy

20. Firm’s finance and dividend policy

21. Attitude towards Risk

21. Attitude towards Risk

26.

EXCESS OR INADEQUATEWORKING CAPITAL

Every business concern should have adequate

working capital to run its business operations. It

should have neither redundant or excess working

capital nor inadequate or shortage of working

capital.

Both excess as well as shortage of working capital

situations are bad for any business. However, out of

the two, inadequacy or shortage of working capital

is more dangerous from the point of view of the firm.

27.

Disadvantages of Redundantor Excess Working

Capital

Idle funds, non-profitable for business, poor ROI

Idle funds, non-profitable for business, poor ROI

Unnecessary purchasing & accumulation of

Unnecessary purchasing & accumulation of

inventories over required level

inventories over required level

Excessive debtors and defective credit policy,

Excessive debtors and defective credit policy,

higher incidence of B/D.

higher incidence of B/D.

Overall inefficiency in the organization.

Overall inefficiency in the organization.

When there is excessive working capital, Credit

When there is excessive working capital, Credit

worthiness suffers

worthiness suffers

Due to low rate of return on investments, the

Due to low rate of return on investments, the

market value of shares may fall

market value of shares may fall

28.

Disadvantages or Dangersof Inadequate or Short

Disadvantages or Dangers of Inadequate or Short

Working Capital

Working Capital

Can’t pay off its short-term liabilities in time.

Can’t pay off its short-term liabilities in time.

Economies of scale are not possible.

Economies of scale are not possible.

Difficult for the firm to exploit favorable market

Difficult for the firm to exploit favorable market

situations

situations

Day-to-day liquidity worsens

Day-to-day liquidity worsens

Improper utilization the fixed assets and

Improper utilization the fixed assets and

ROA/ROI falls sharply

ROA/ROI falls sharply

29.

MANAGEMENT OF WORKINGCAPITAL ( WCM )

MANAGEMENT OF WORKING CAPITAL ( WCM )

Management of working capital is concerned with

Management of working capital is concerned with

the problems that arise in attempting to manage the

the problems that arise in attempting to manage the

current assets, the current liabilities and the inter-

current assets, the current liabilities and the inter-

relationship that exists between them.

relationship that exists between them. In other

In other

words, it refers to all aspects of administration of CA

words, it refers to all aspects of administration of CA

and CL.

and CL.

Working Capital Management Policies of a firm have

Working Capital Management Policies of a firm have

a great effect on its

a great effect on its profitability, liquidity and

profitability, liquidity and

structural health of the organization.

structural health of the organization.