Downloaded 422 times

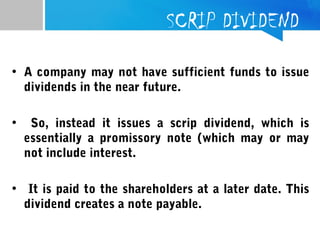

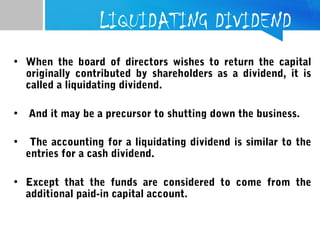

Dividends are a portion of a company's earnings distributed to shareholders, decided by the board of directors, and can be classified into several types: cash, stock, property, scrip, and liquidating dividends. Cash dividends are the most common, while stock dividends involve issuing more shares; property dividends involve distributing physical assets. The board determines the distribution timing, and key dates include declaration, record, and payment dates.

![Fmch17[1]](https://cdn.slidesharecdn.com/ss_thumbnails/fmch171-211219052311-thumbnail.jpg?width=640&height=640&fit=bounds)

![Awareness of digital currency[1] (1).pptx](https://cdn.slidesharecdn.com/ss_thumbnails/awarenessofdigitalcurrency11-260125155504-b1badee4-thumbnail.jpg?width=640&height=640&fit=bounds)