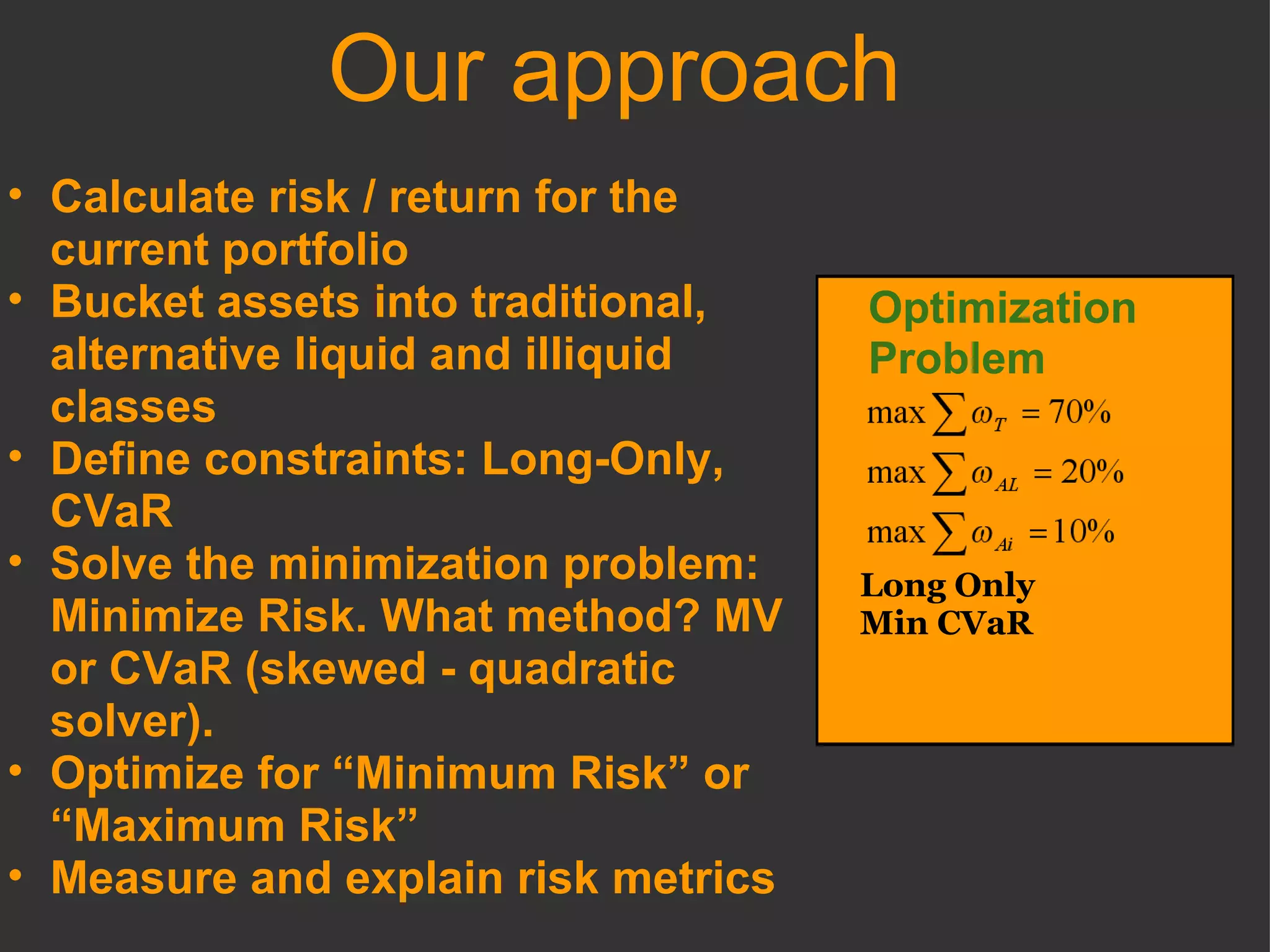

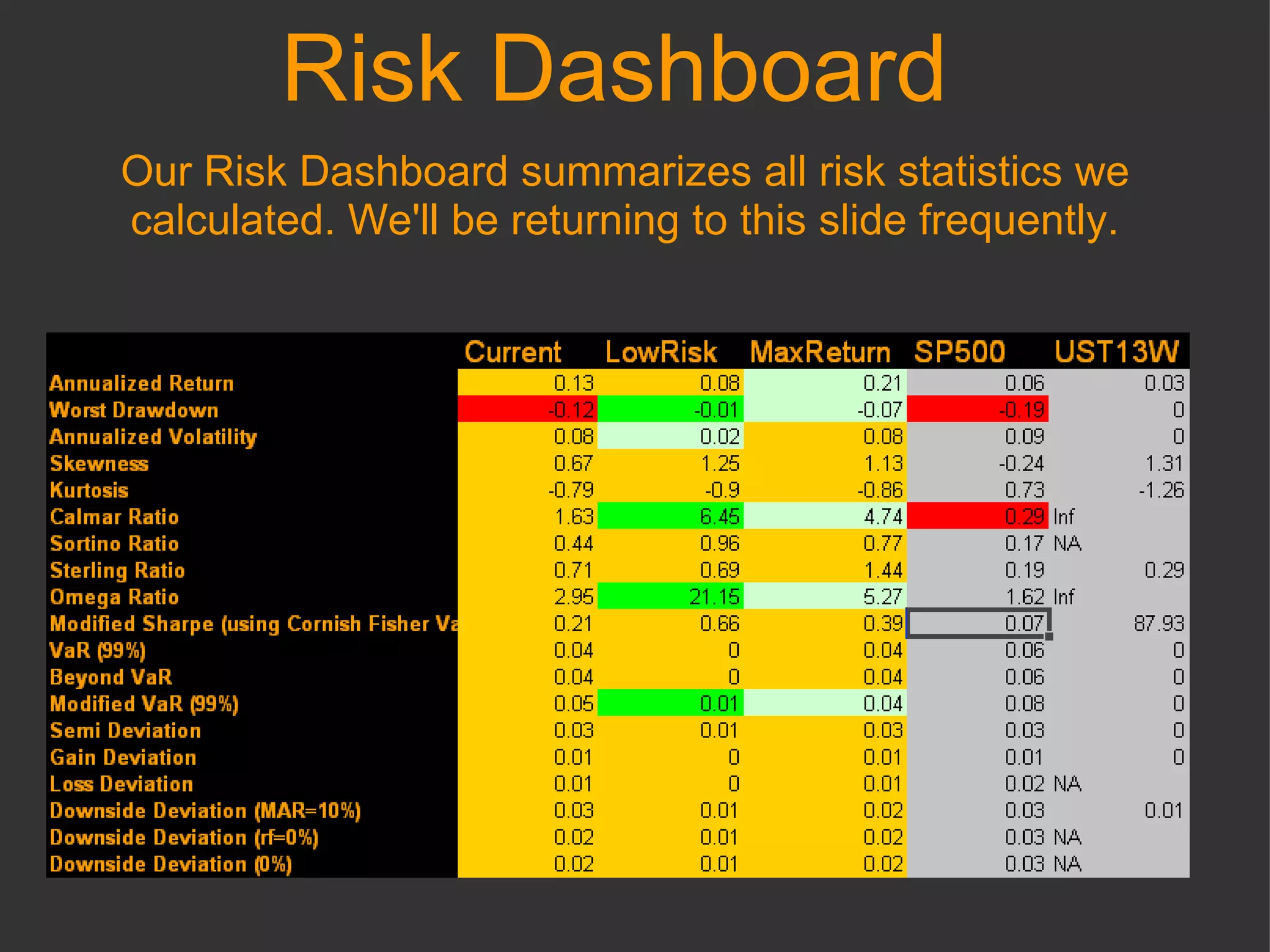

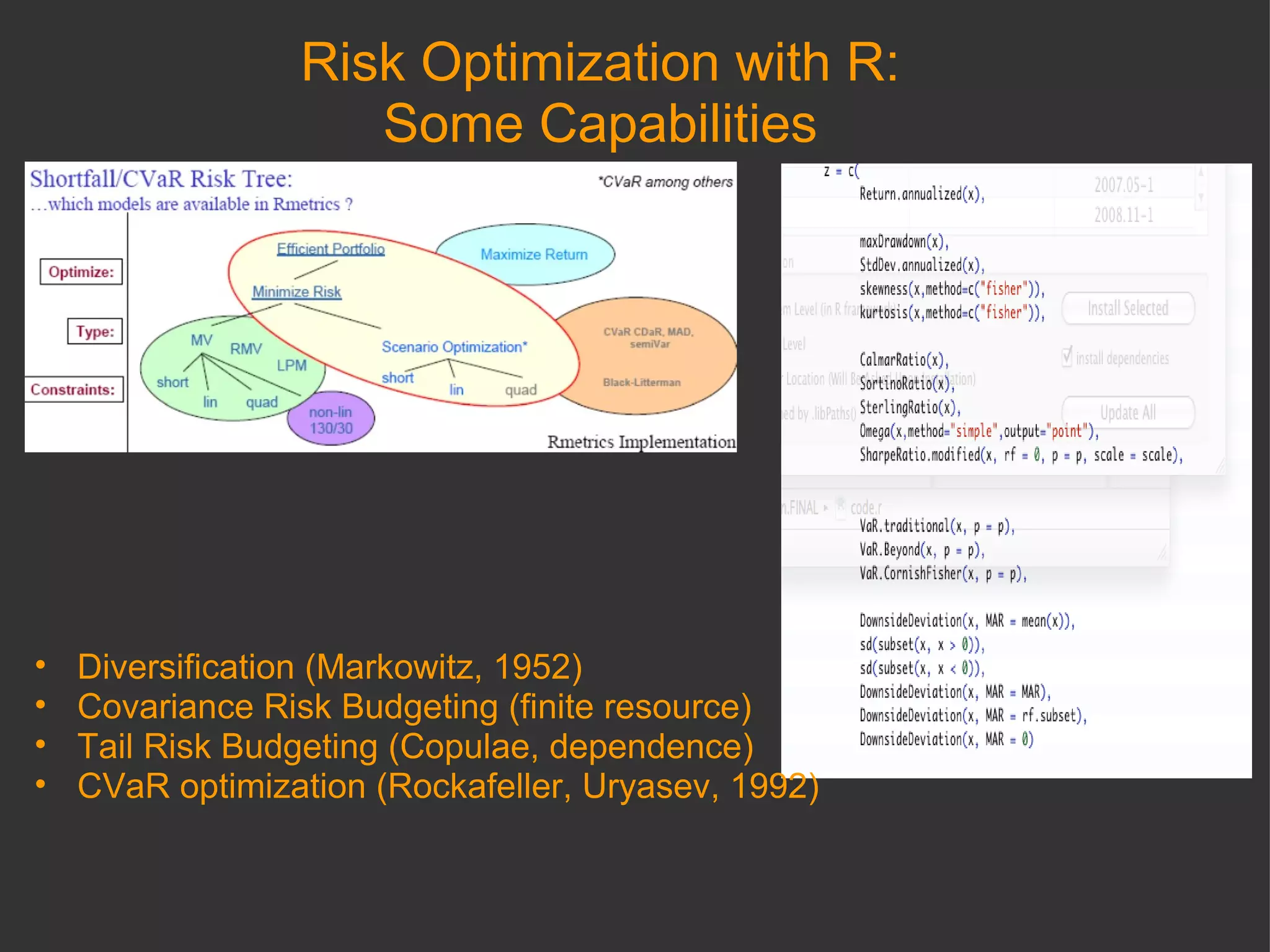

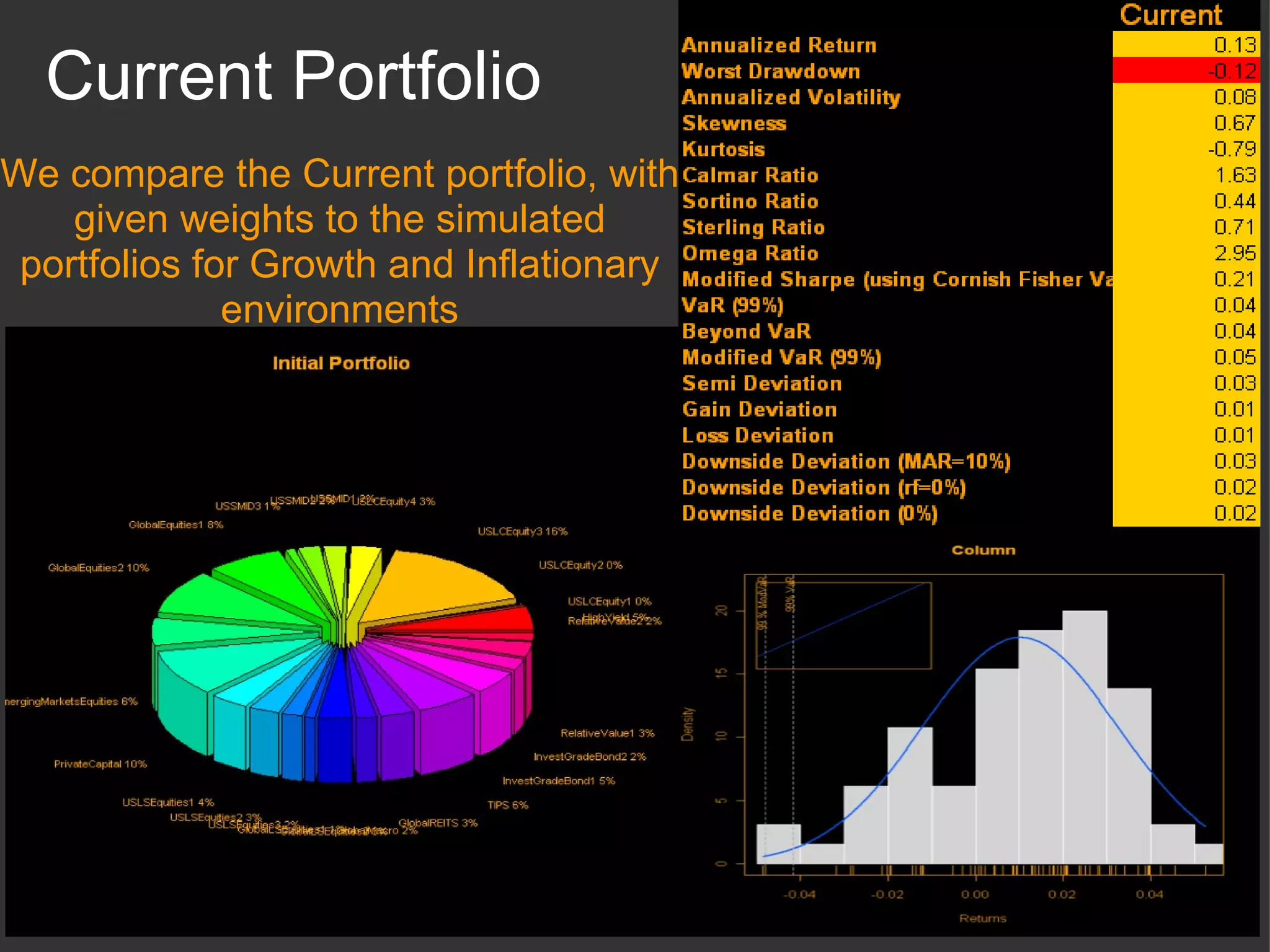

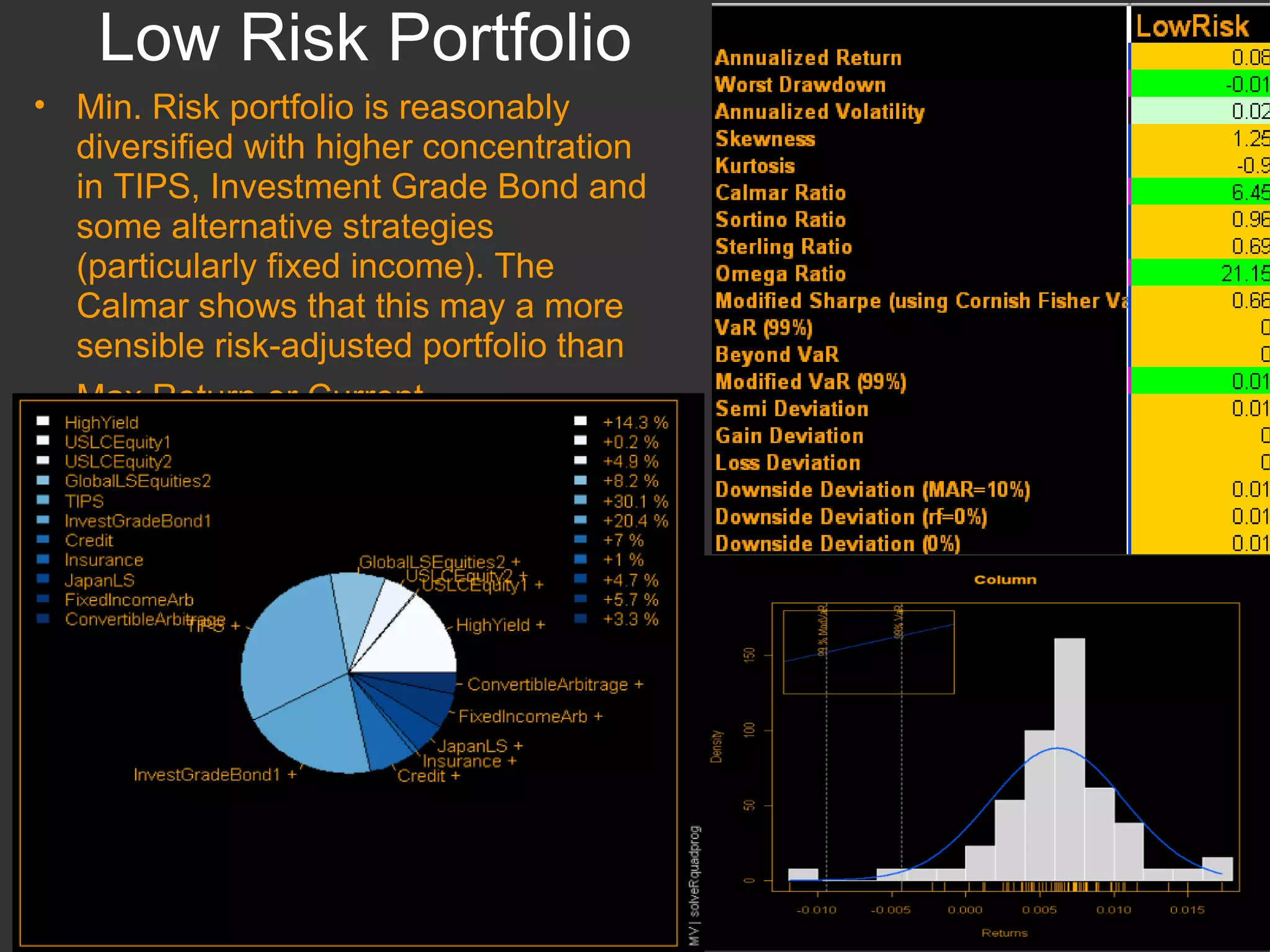

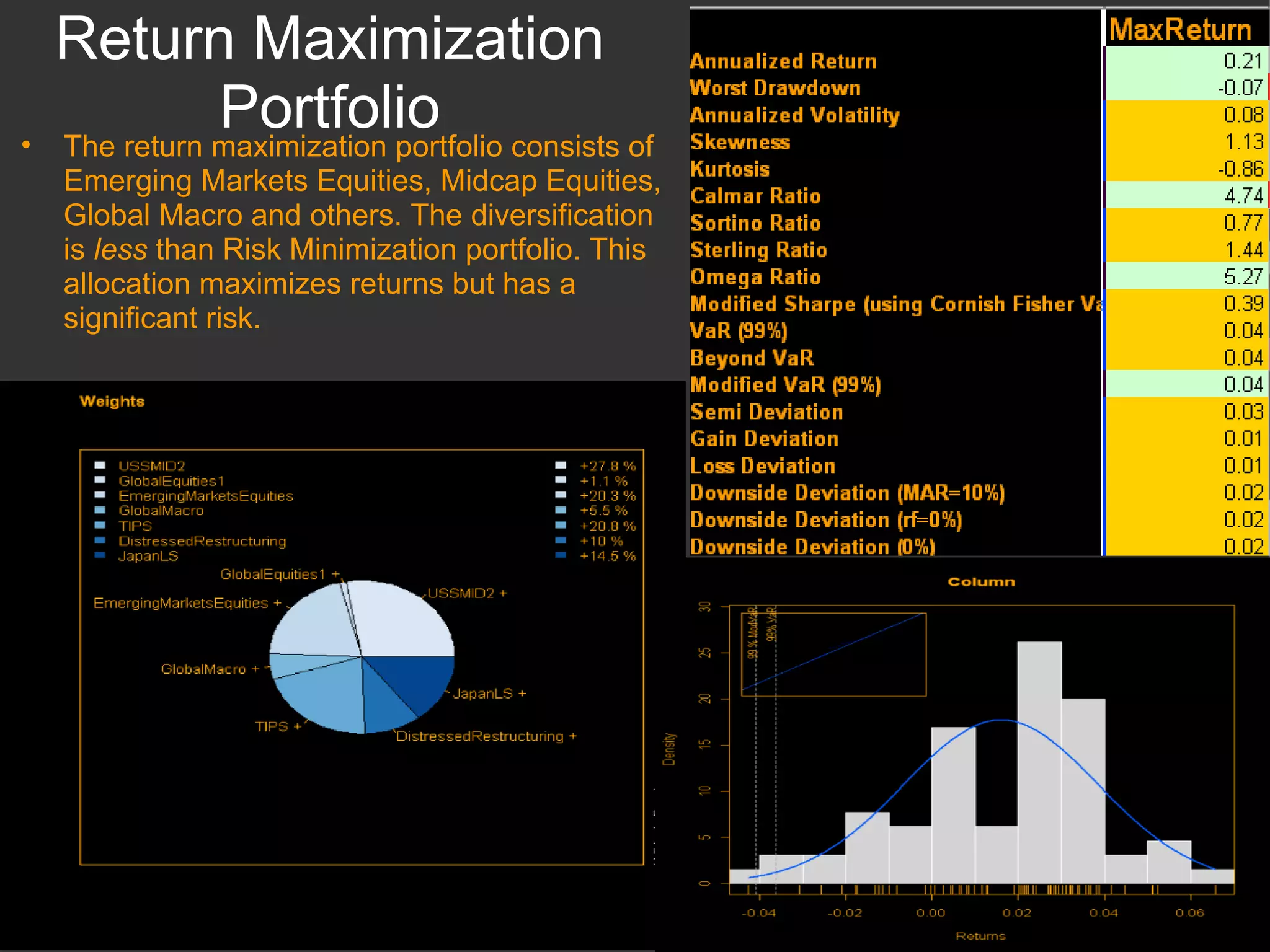

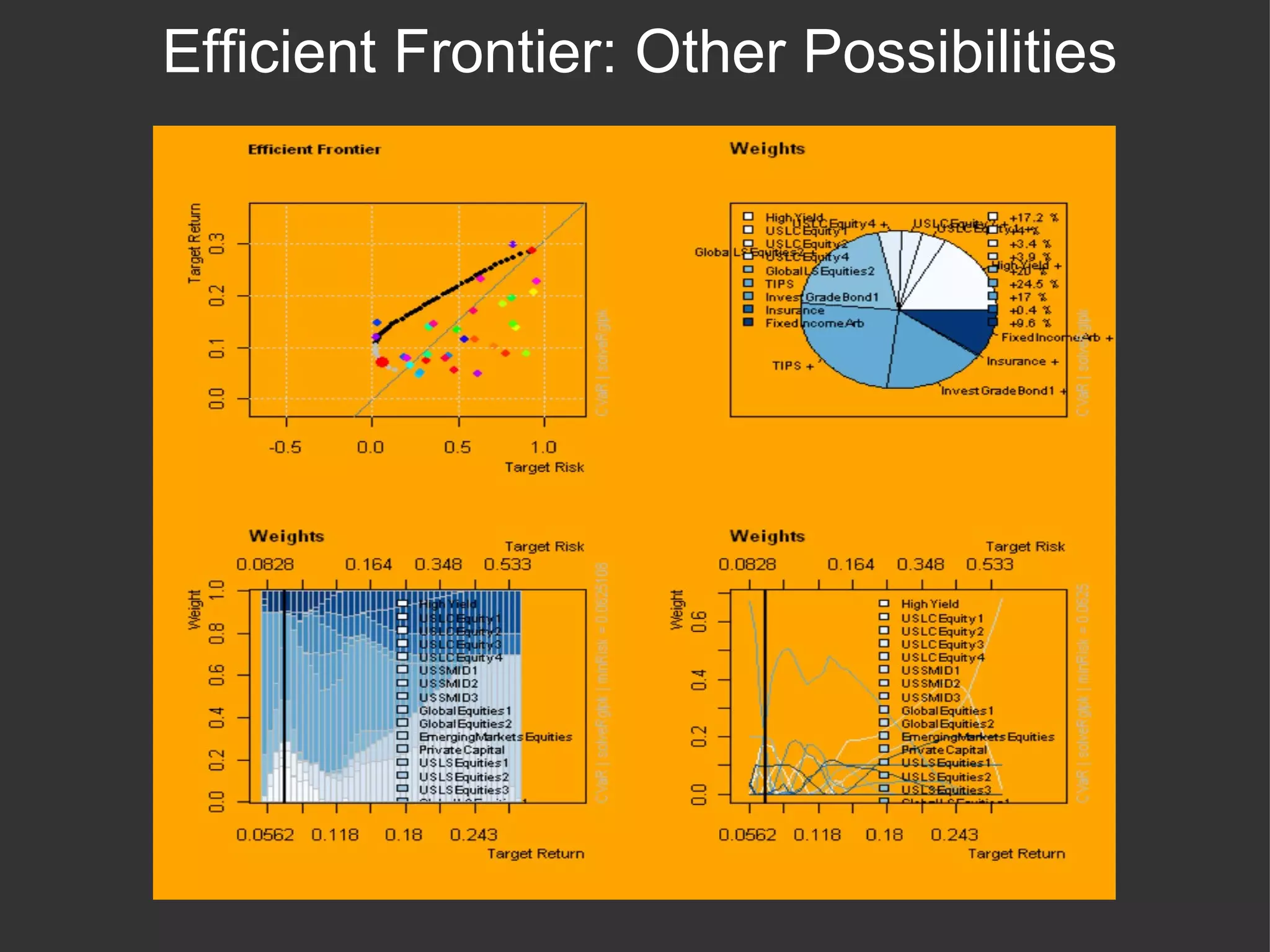

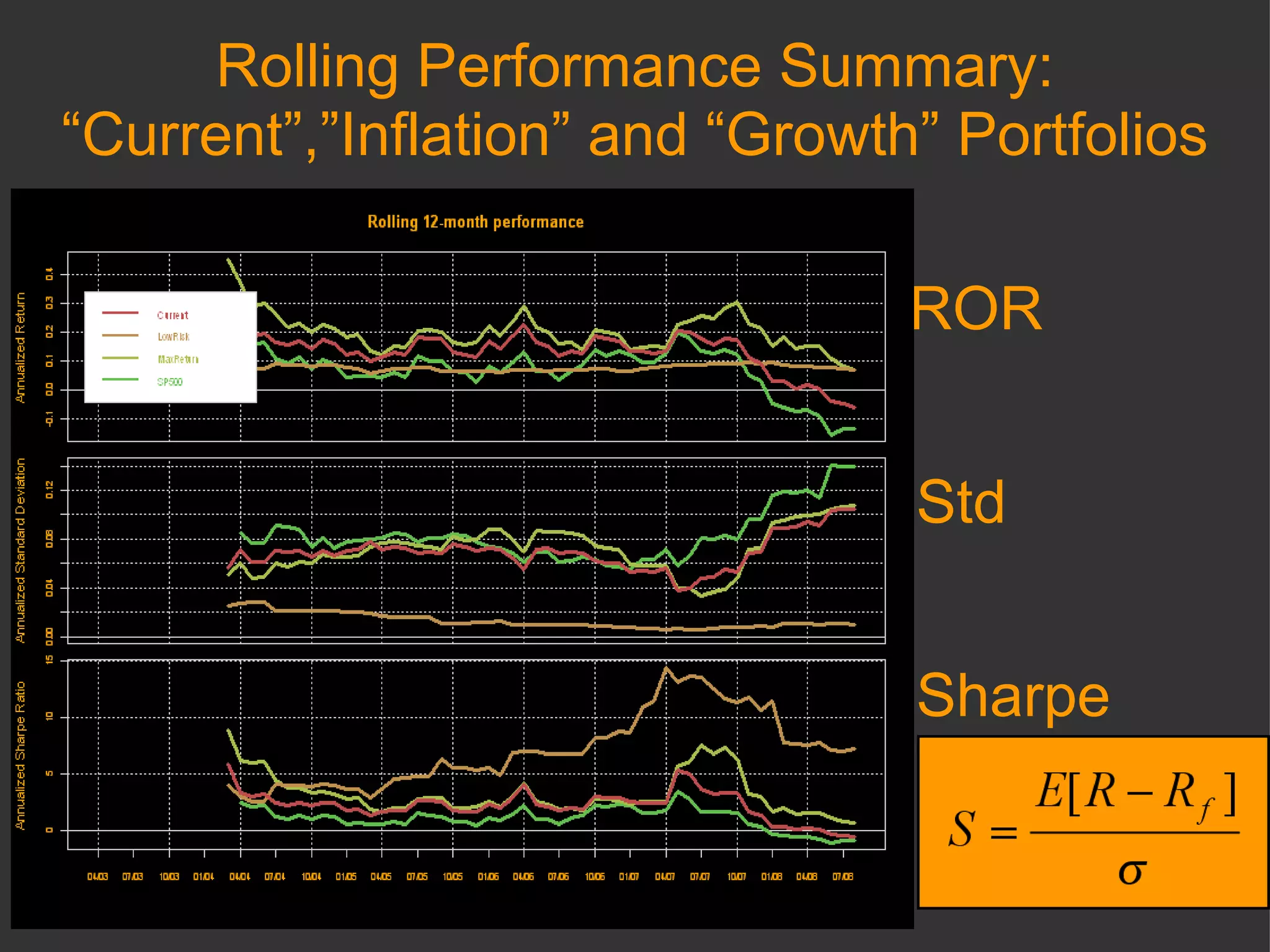

The document discusses using R and RMetrics to simulate portfolios and optimize risk and return. It describes calculating risk metrics, defining constraints like long-only positions, and using CVaR to minimize risk. Optimal "Minimum Risk" and "Maximum Return" portfolios are generated and compared to a current portfolio in terms of risk, return, diversification, correlation, drawdowns, and other measures.

![Omega Plots MAR - minimal acceptable return, 0.1/12 monthly [a,b] interval for which the distribution of the asset return is defined](https://image.slidesharecdn.com/SimulationPresentation-123306183217-phpapp01/75/Hedge-Fund-Risks-Simulation-10-2048.jpg)