Download to read offline

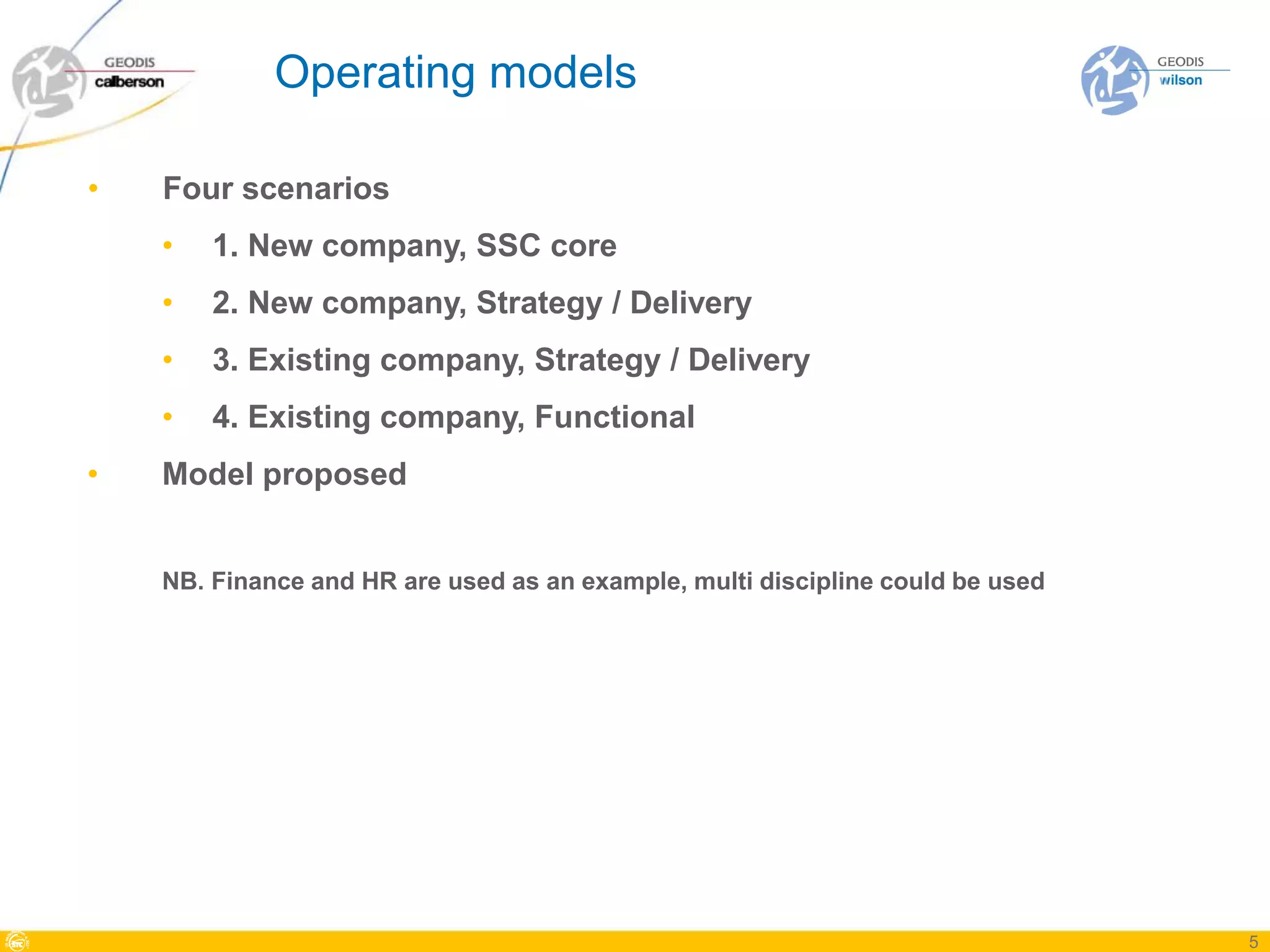

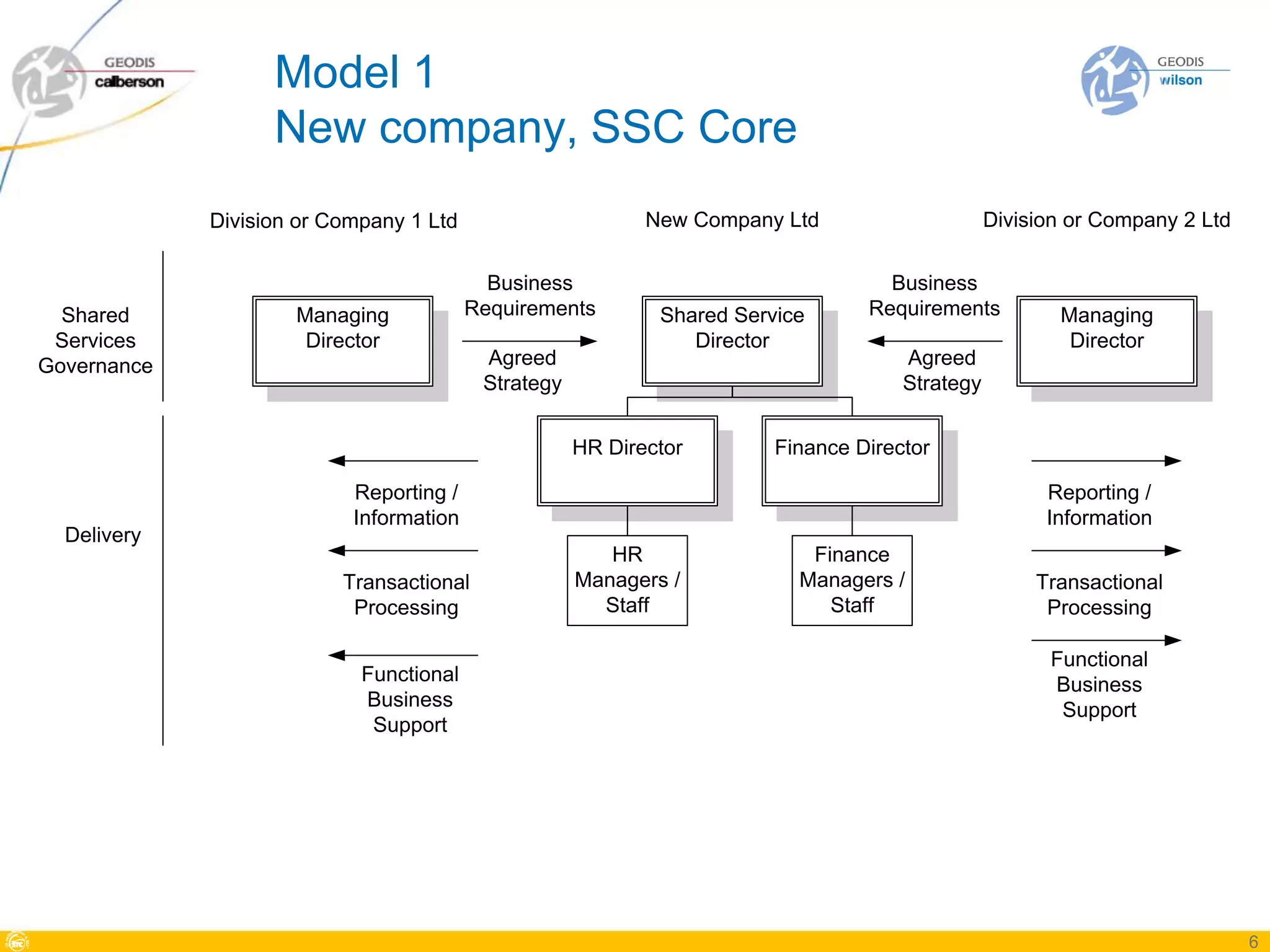

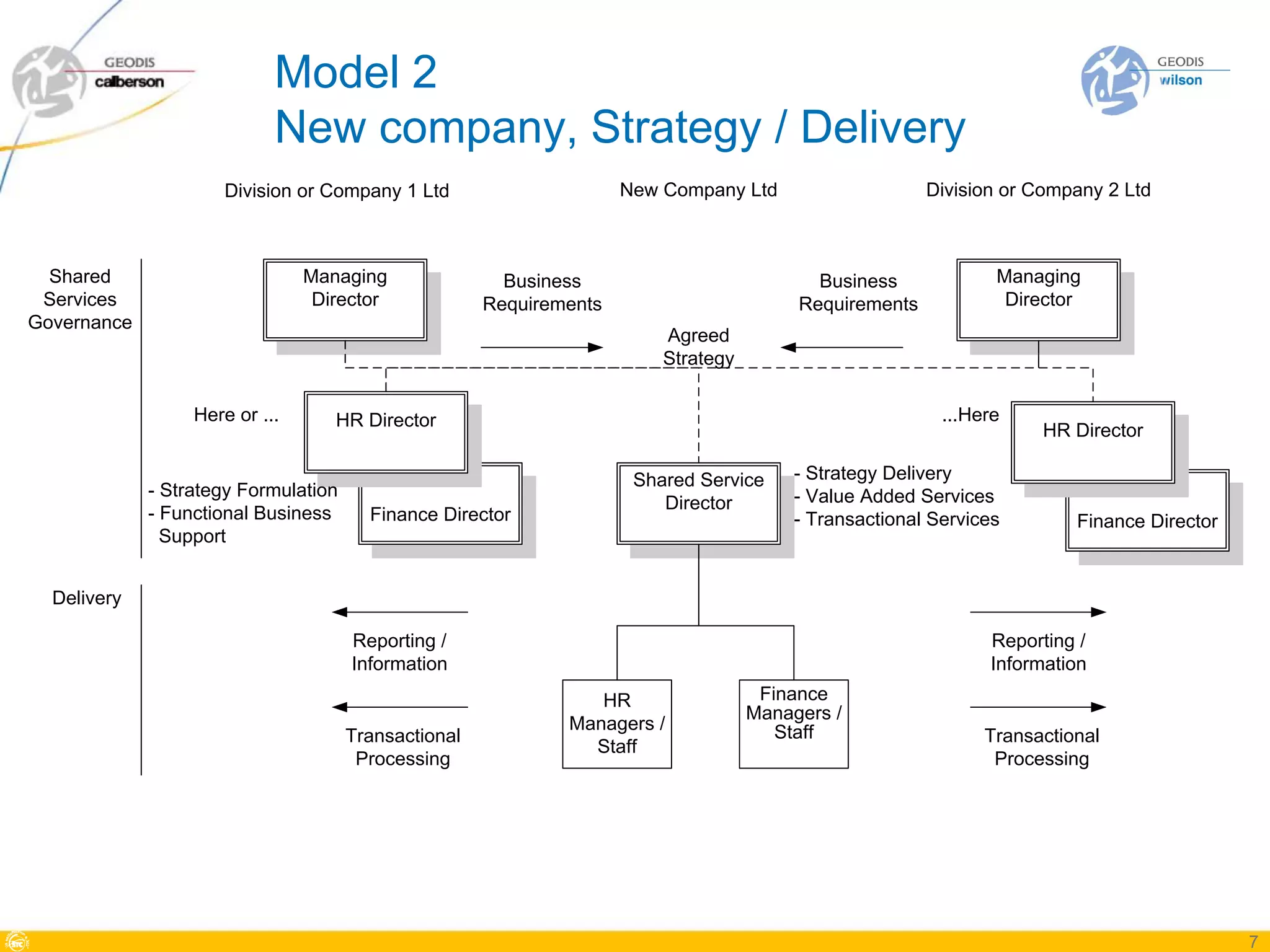

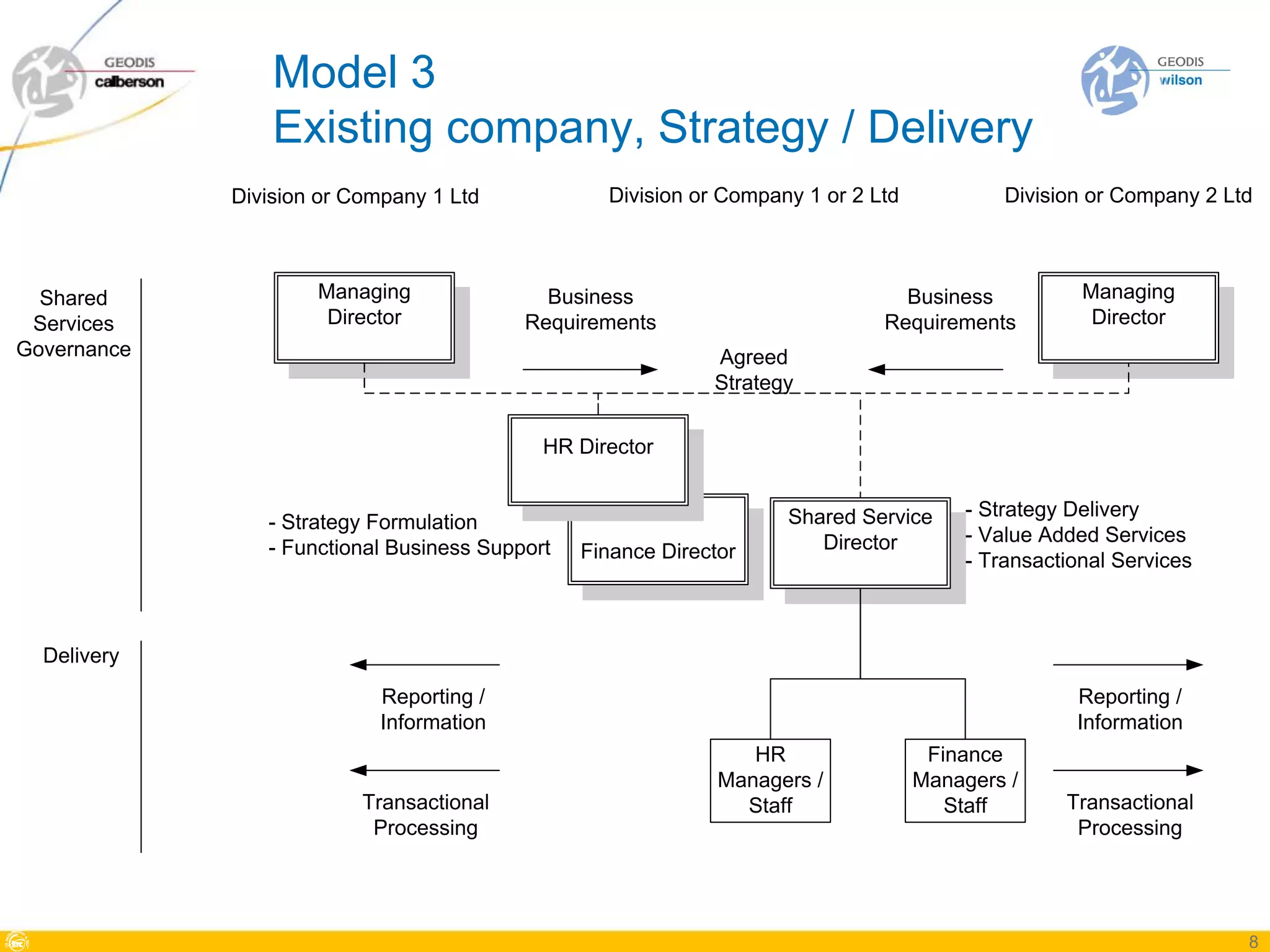

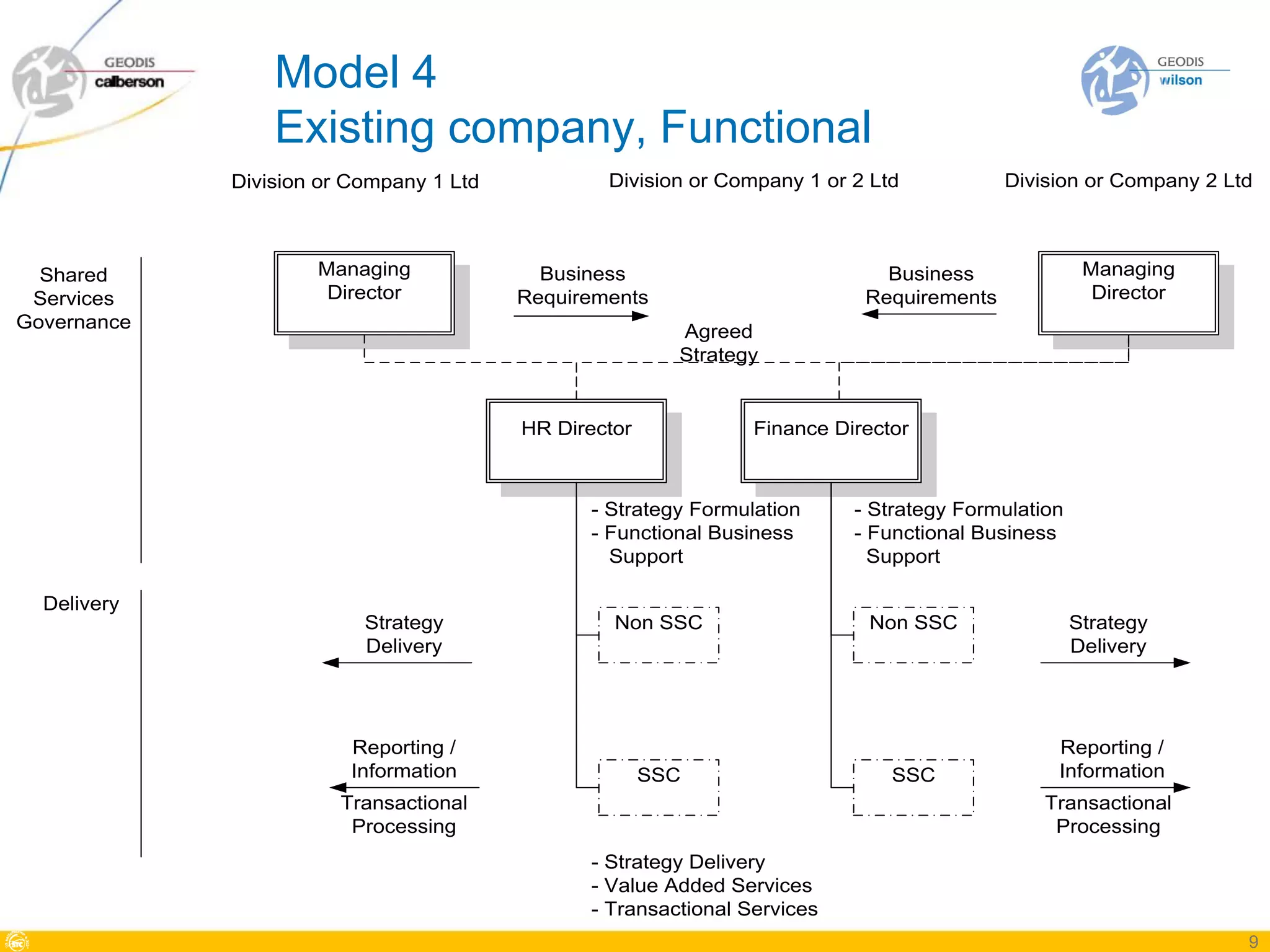

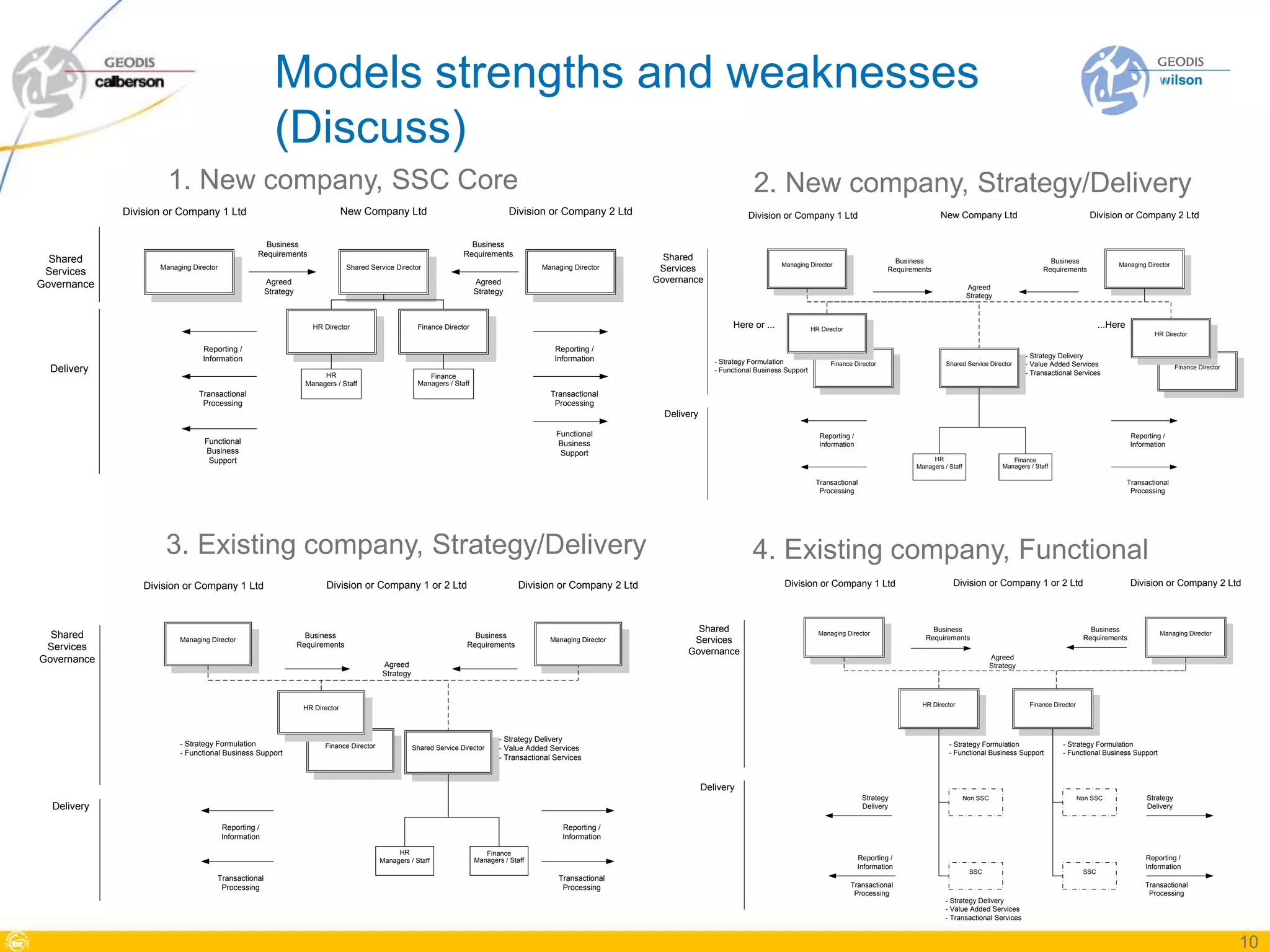

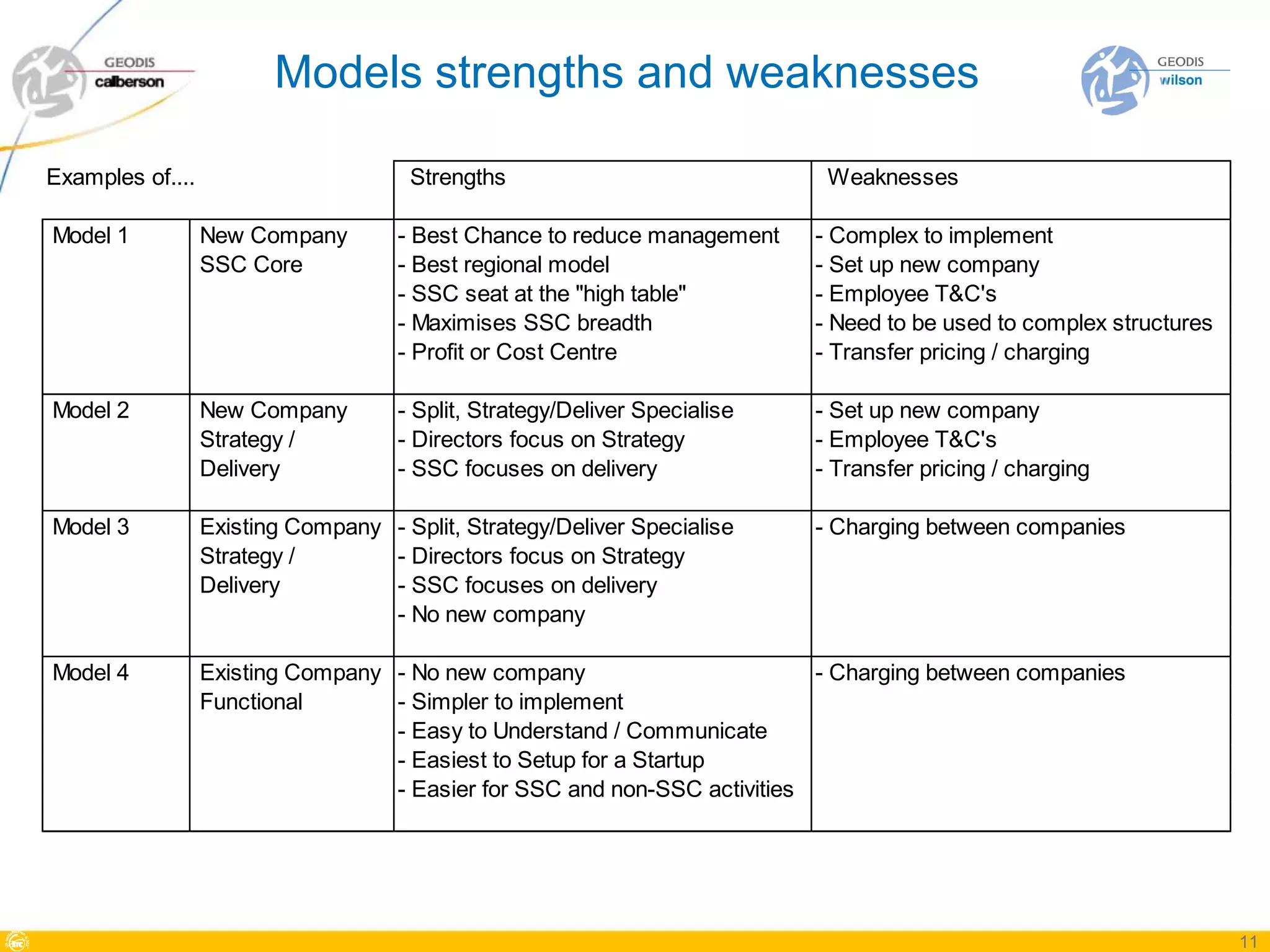

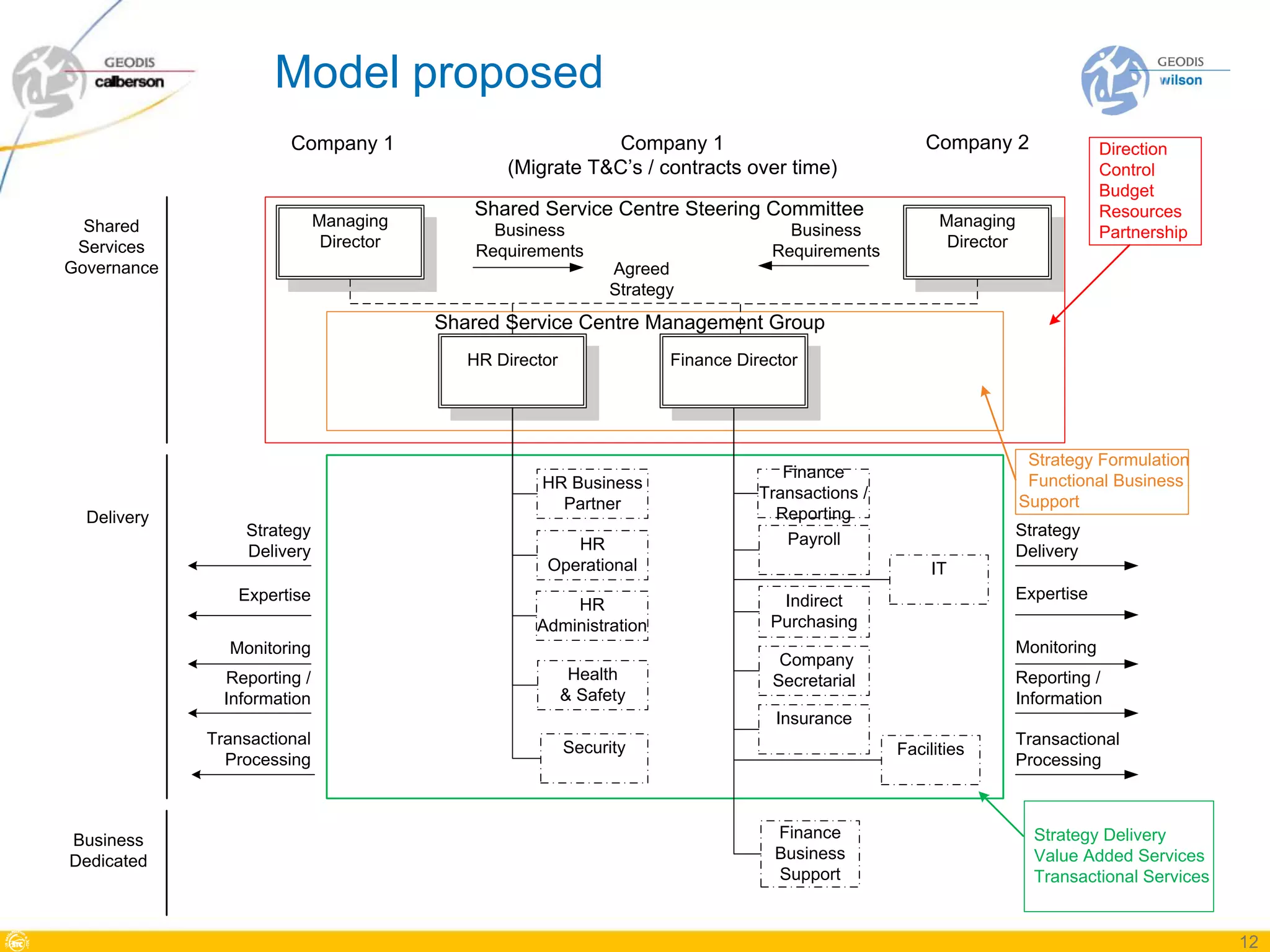

The document discusses four models for shared services: 1) new company with SSC core, 2) new company with strategy/delivery split, 3) existing company with strategy/delivery split, and 4) existing company functional model. It proposes model 3, an existing company strategy/delivery split. Key criteria for decision making include maturity, culture, structure, and tax implications. Selling the chosen model requires evaluating all elements, involving all disciplines, and gaining understanding and buy-in from decision makers.