Download to read offline

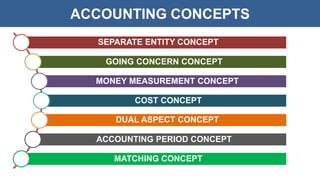

The document outlines fundamental accounting concepts such as the separate entity, going concern, and dual aspect concepts, alongside accounting conventions including conservatism and full disclosure. It emphasizes the significance of accounting principles in recording financial transactions and their implications for financial reporting. Overall, the document serves as a guide to essential accounting notions that ensure accurate and reliable financial statements.

![Acounting Concepts and Conventions [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/acountingconceptsandconventionsautosaved-250421132407-1a5db1b2-thumbnail.jpg?width=640&height=640&fit=bounds)