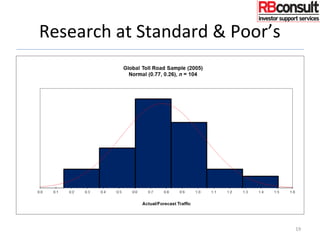

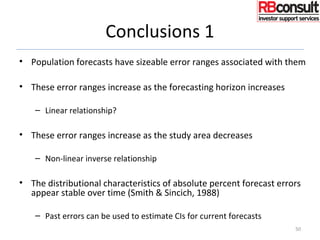

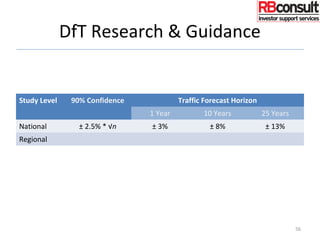

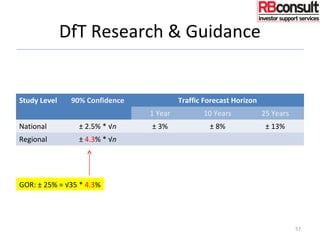

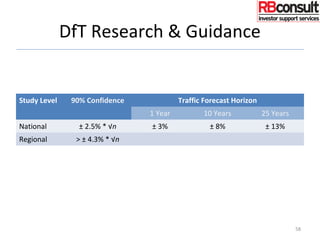

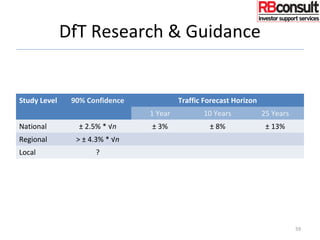

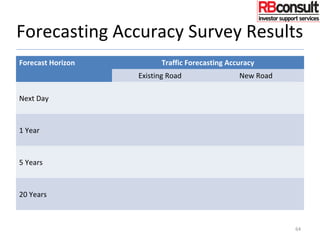

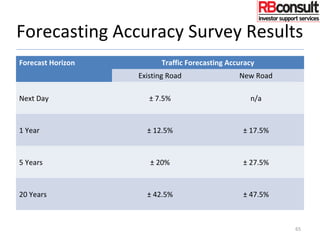

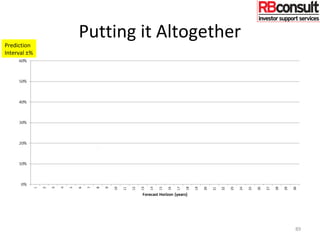

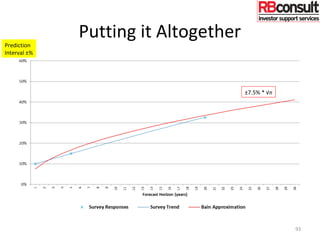

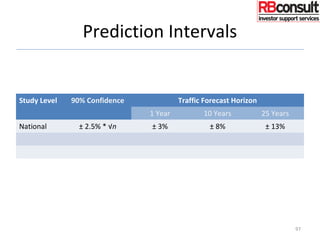

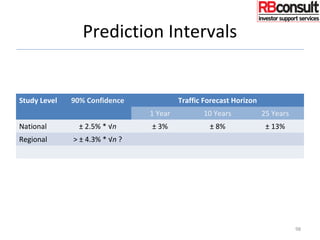

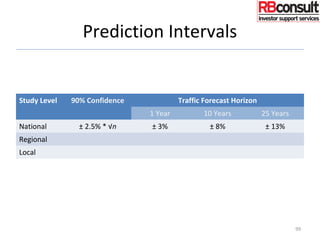

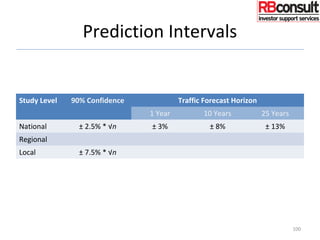

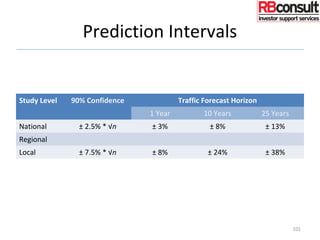

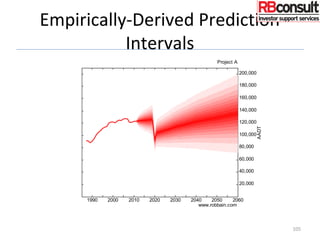

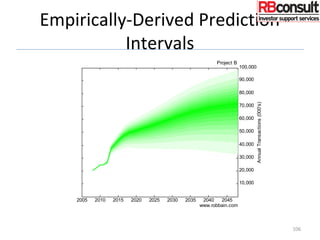

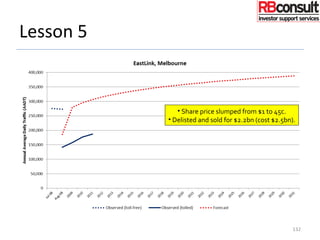

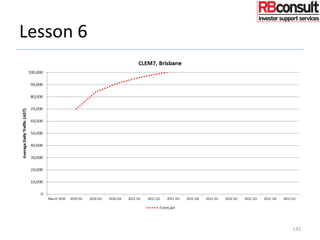

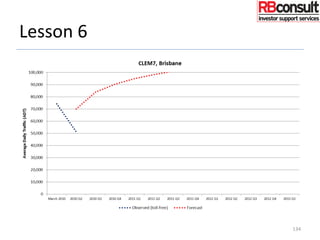

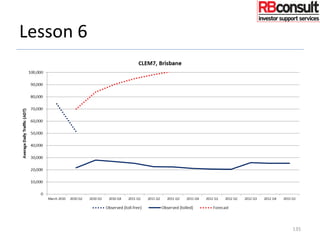

This document summarizes research on traffic forecasting accuracy and developing empirically-derived prediction intervals for traffic forecasts. It finds that traffic forecasts, especially at local levels, have large errors that increase with the forecast horizon. Research on over 100 toll road projects found errors averaged around 35% within 10 years. UK highway agency studies found around a third of local road forecasts were off by over 15% after 10 years. Based on these findings, the document proposes developing prediction intervals for traffic forecasts at national, regional and local levels to convey the uncertainty in forecasts over different time horizons.