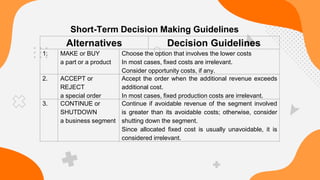

This document discusses relevant costs and their importance in decision making. It defines relevant costs as those that relate specifically to a management decision and will change depending on the decision. Only future costs that differ between alternatives are relevant. Qualitative and quantitative factors must be considered in decisions. Short-term decisions involve determining if costs are incremental, avoidable, or opportunity costs. Common short-term decisions include whether to make or buy a product, accept special orders, or continue or shut down a business segment. Guidelines for these decisions focus on choosing the option with the lowest costs or highest contribution to profits.

![Presentation1 [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/presentation1autosaved-230321131949-06351496-thumbnail.jpg?width=640&height=640&fit=bounds)