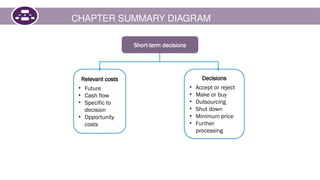

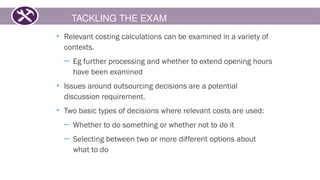

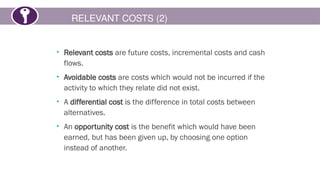

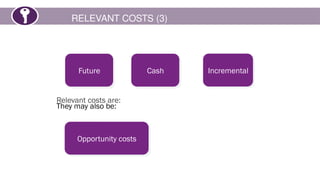

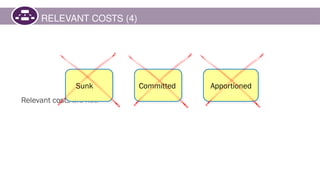

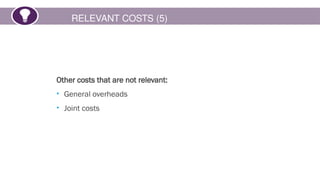

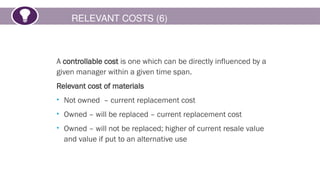

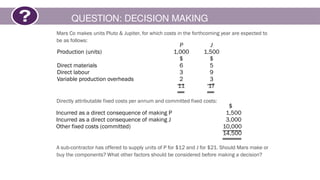

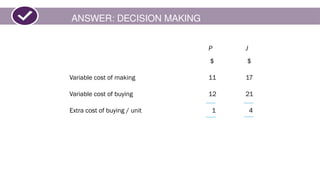

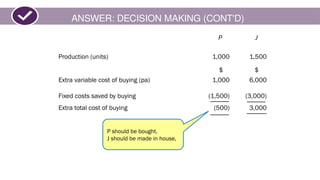

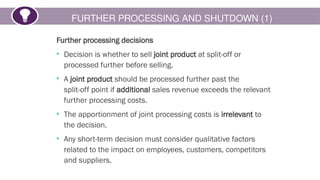

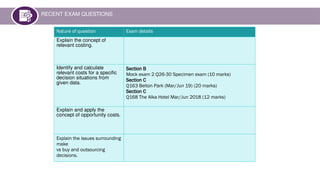

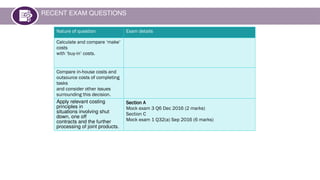

The document discusses relevant costing principles applied to various short-term business decisions such as make or buy, outsourcing, and shutdown scenarios. It covers the identification and calculation of relevant costs, opportunity costs, and qualitative factors that influence decision-making. Key takeaways include that relevant costs are future, incremental, and cash flows, while sunk and committed costs are generally irrelevant.

![Presentation1 [Autosaved].pptx](https://cdn.slidesharecdn.com/ss_thumbnails/presentation1autosaved-230321131949-06351496-thumbnail.jpg?width=640&height=640&fit=bounds)