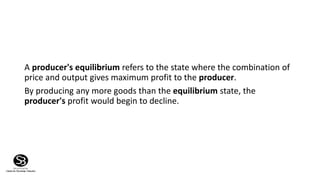

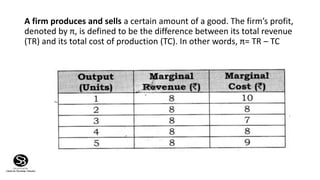

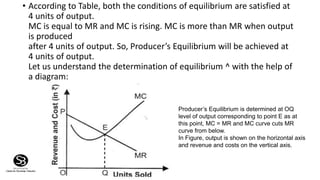

A producer's equilibrium refers to the level of output where the producer earns maximum profits. This occurs where marginal revenue equals marginal cost and marginal cost is rising. There are two approaches to determining producer's equilibrium - the total revenue and total cost approach, and the marginal revenue and marginal cost approach. Under both approaches, equilibrium is reached at the quantity of output where marginal revenue equals marginal cost and marginal cost is rising. This equilibrium can be illustrated using diagrams with output on the x-axis and costs/revenues on the y-axis.