Downloaded 165 times

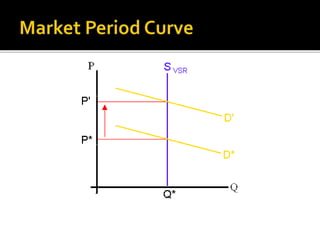

Perfect competition is defined as a market where many firms sell identical products, with no single firm able to influence market prices, characterized by a large number of buyers, homogeneous products, and no barriers to entry or exit. Price determination occurs over three periods: very short run, short run, and long run, during which firms can incur supernormal profits or losses. In the long run, firms typically earn normal profit, where total revenue equals total cost, and prices are primarily influenced by supply and demand changes.