Downloaded 14 times

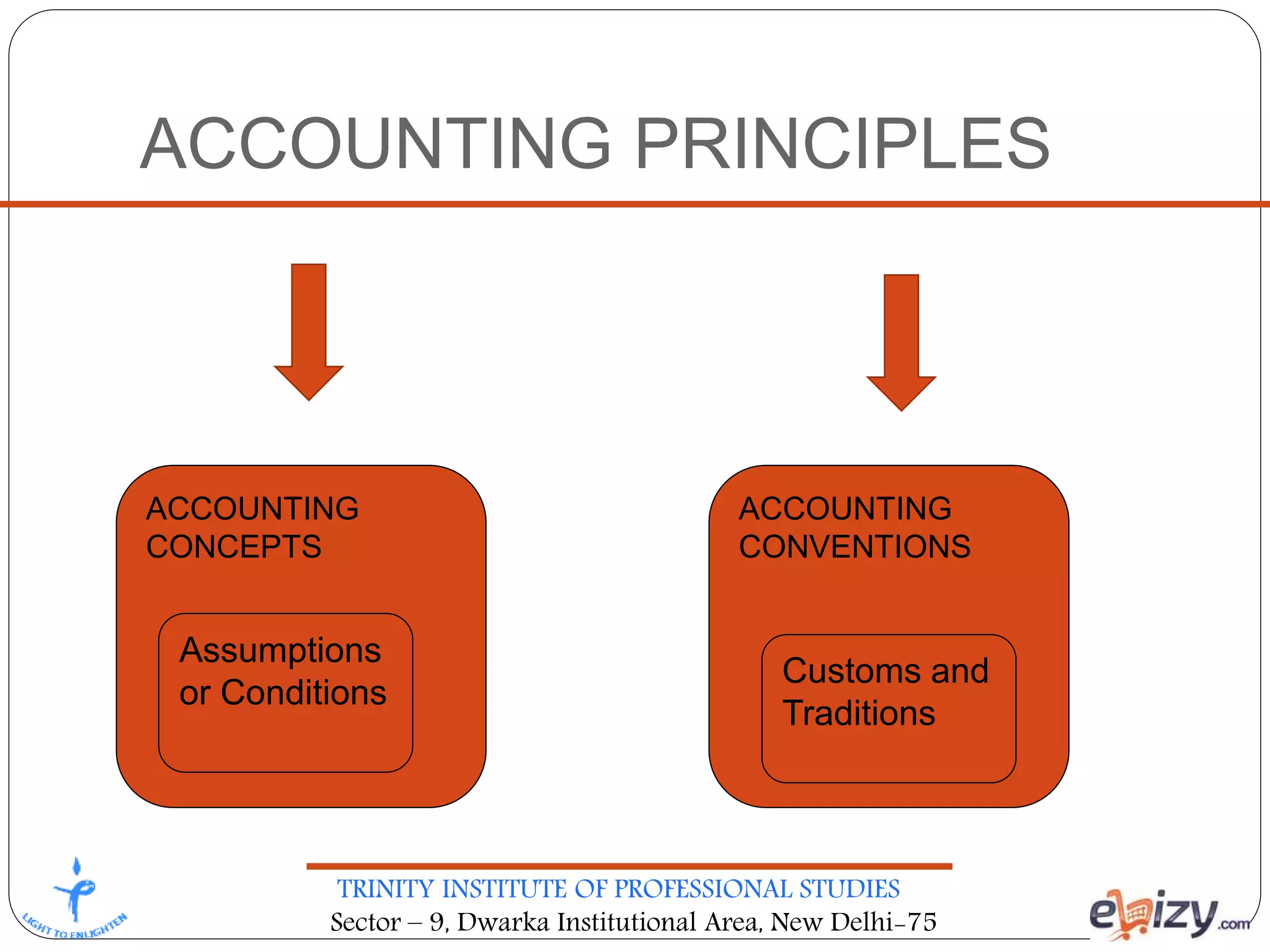

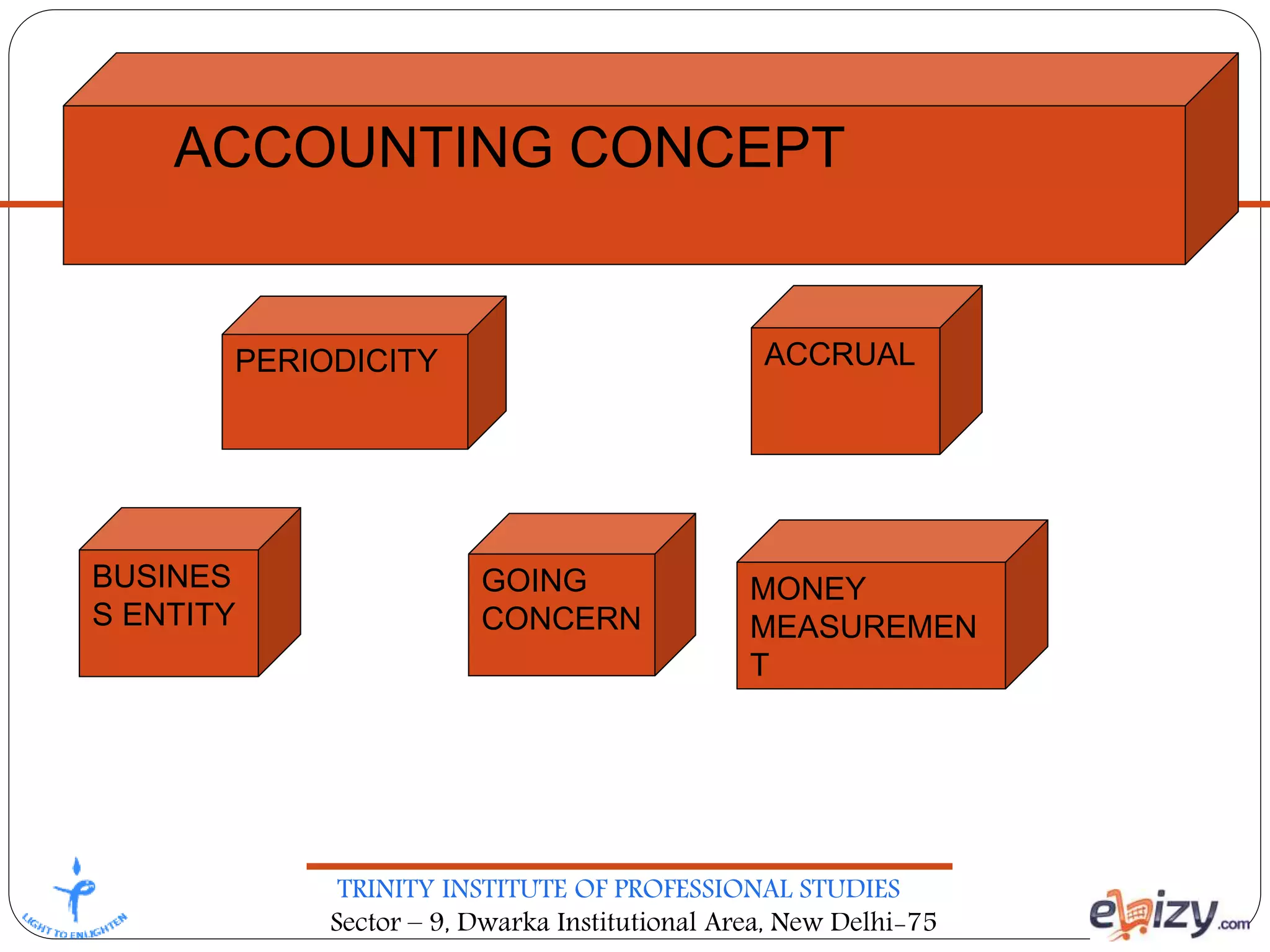

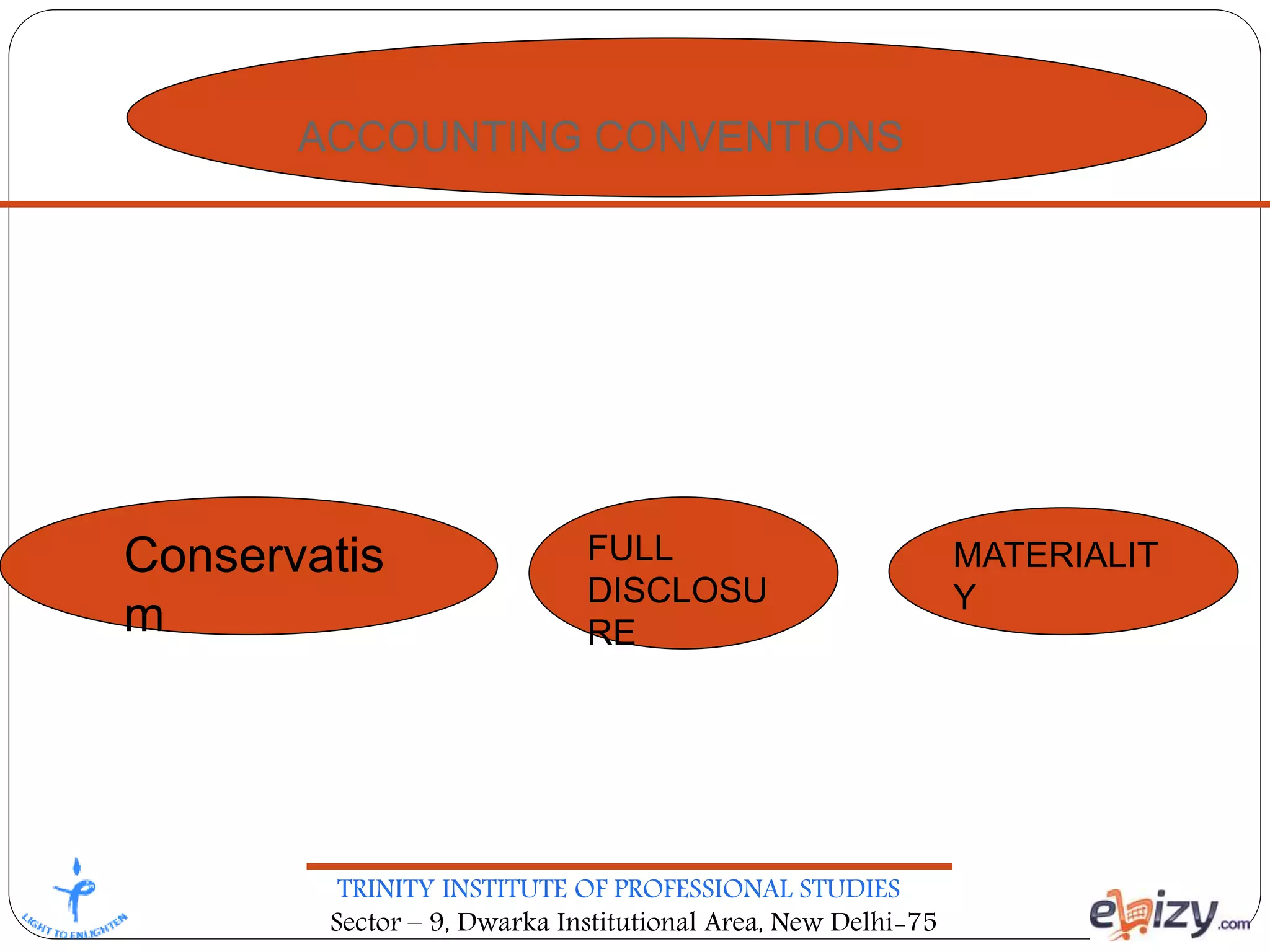

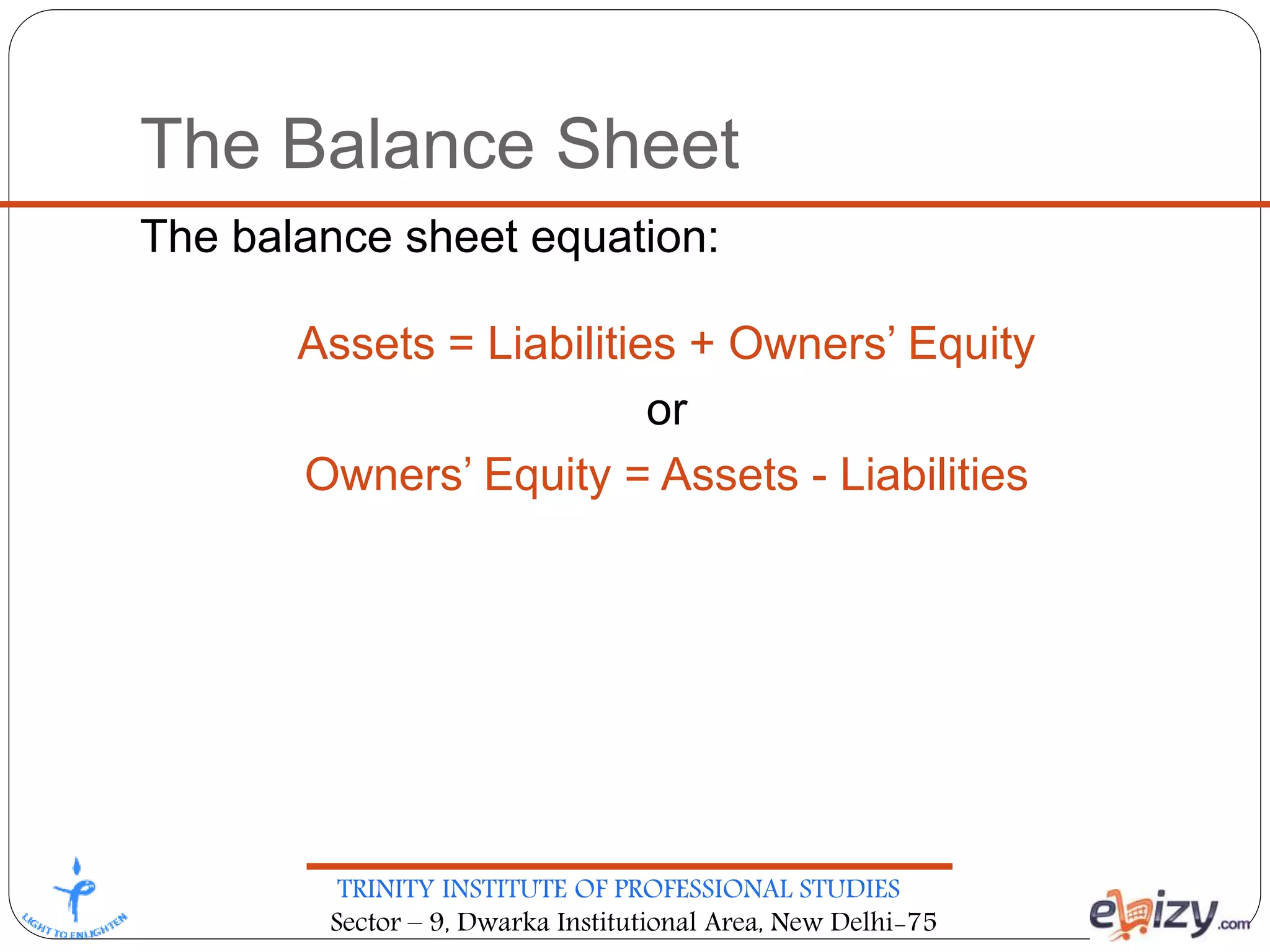

The document outlines the principles of accounting taught at the Trinity Institute of Professional Studies, emphasizing financial accounting as a process for identifying, recording, summarizing, and reporting economic information. The course aims to familiarize students with essential accounting principles and their application in various sectors, aiding decision-making for stakeholders such as managers, investors, and creditors. Key concepts include the balance sheet structure, transaction analysis, and the importance of maintaining accurate financial records.