Downloaded 13 times

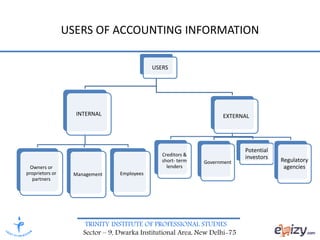

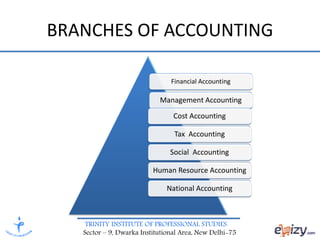

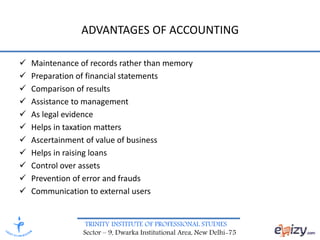

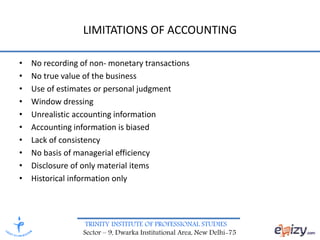

The document provides an overview of accounting and financial accounting, detailing its definition, features, objectives, and significance as an information system. It outlines the various users of accounting information, branches of accounting, as well as the advantages and limitations associated with the practice. Specifically, it emphasizes accounting's role in communication and decision-making for both internal and external stakeholders.