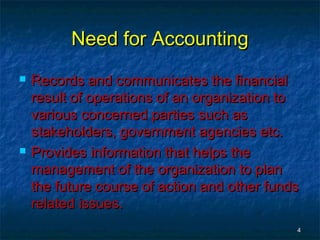

This document provides an overview of an accounting course for managers. It outlines the course objectives, which include understanding management and cost accounting techniques, performing financial analysis, calculating financial ratios, and preparing statements of cash flows and budgets. It also outlines the evaluation criteria and covers topics like the need for accounting, definitions of accounting, the functions and role of accounting/accountants, and accounting services. The overall purpose is to introduce managers to key accounting concepts and financial reporting.

![Pagsasanay,,pagkonsumo [the in war]](https://cdn.slidesharecdn.com/ss_thumbnails/pagsasanaypagkonsumotheinwar-140104225441-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)