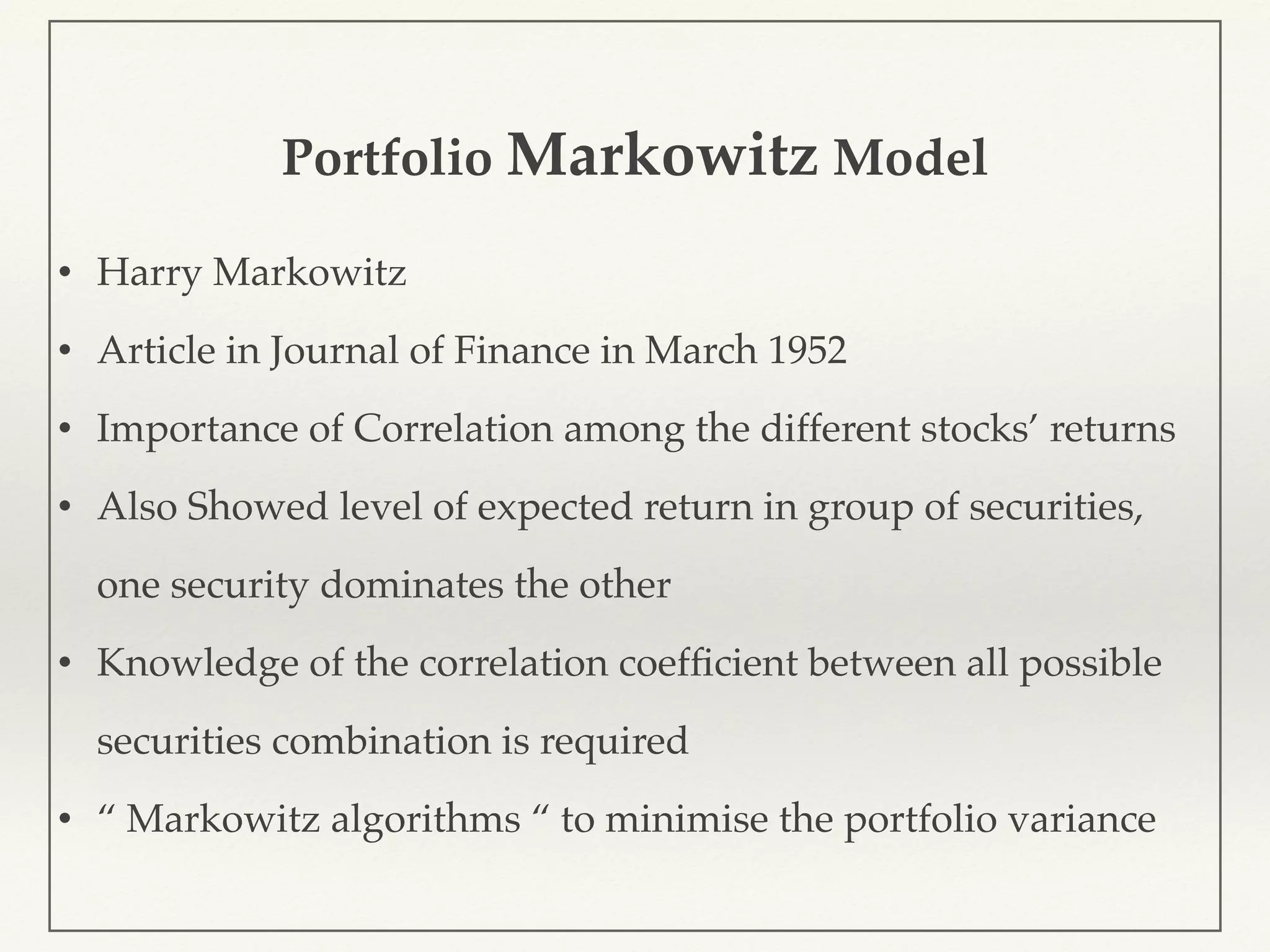

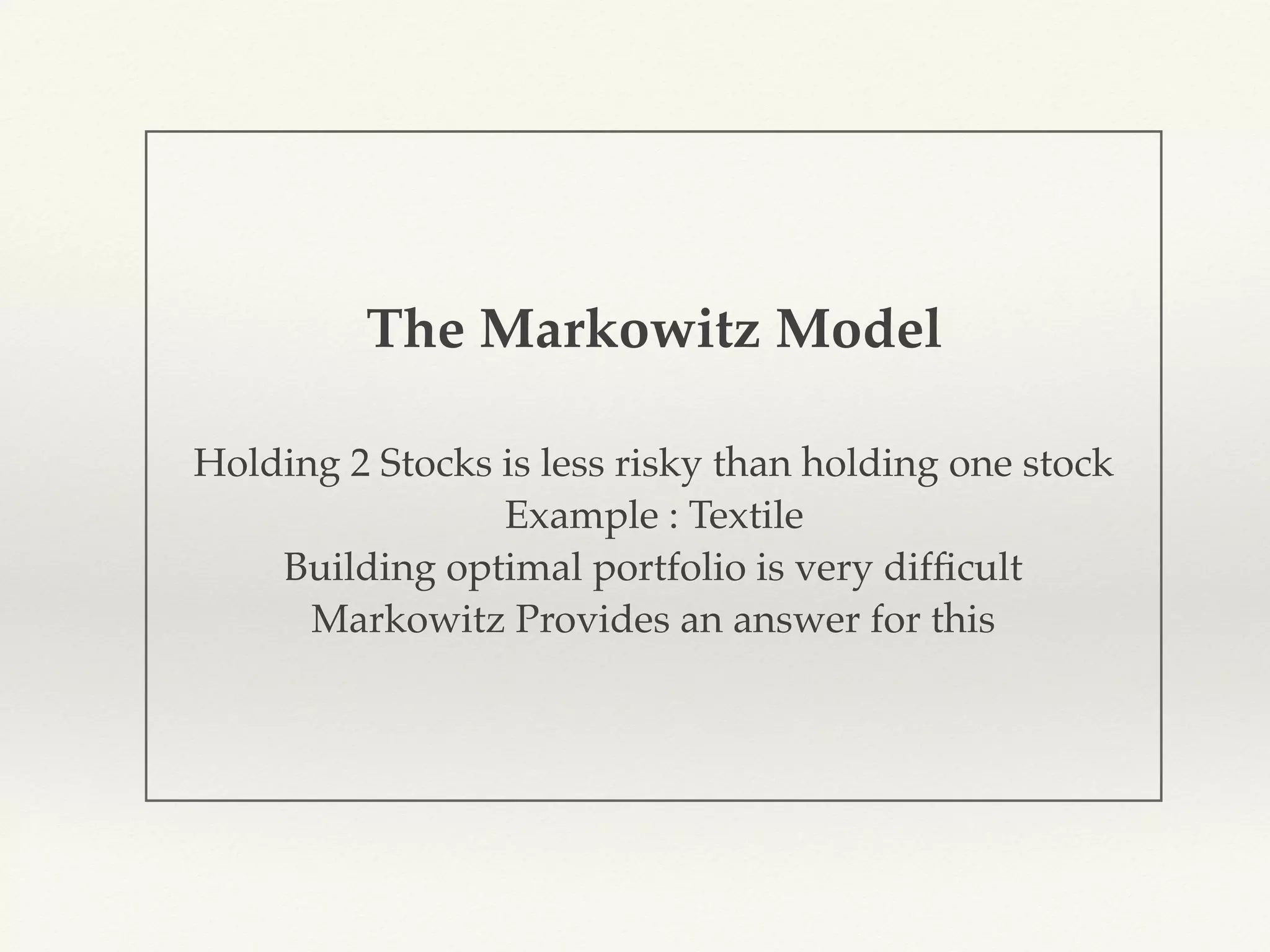

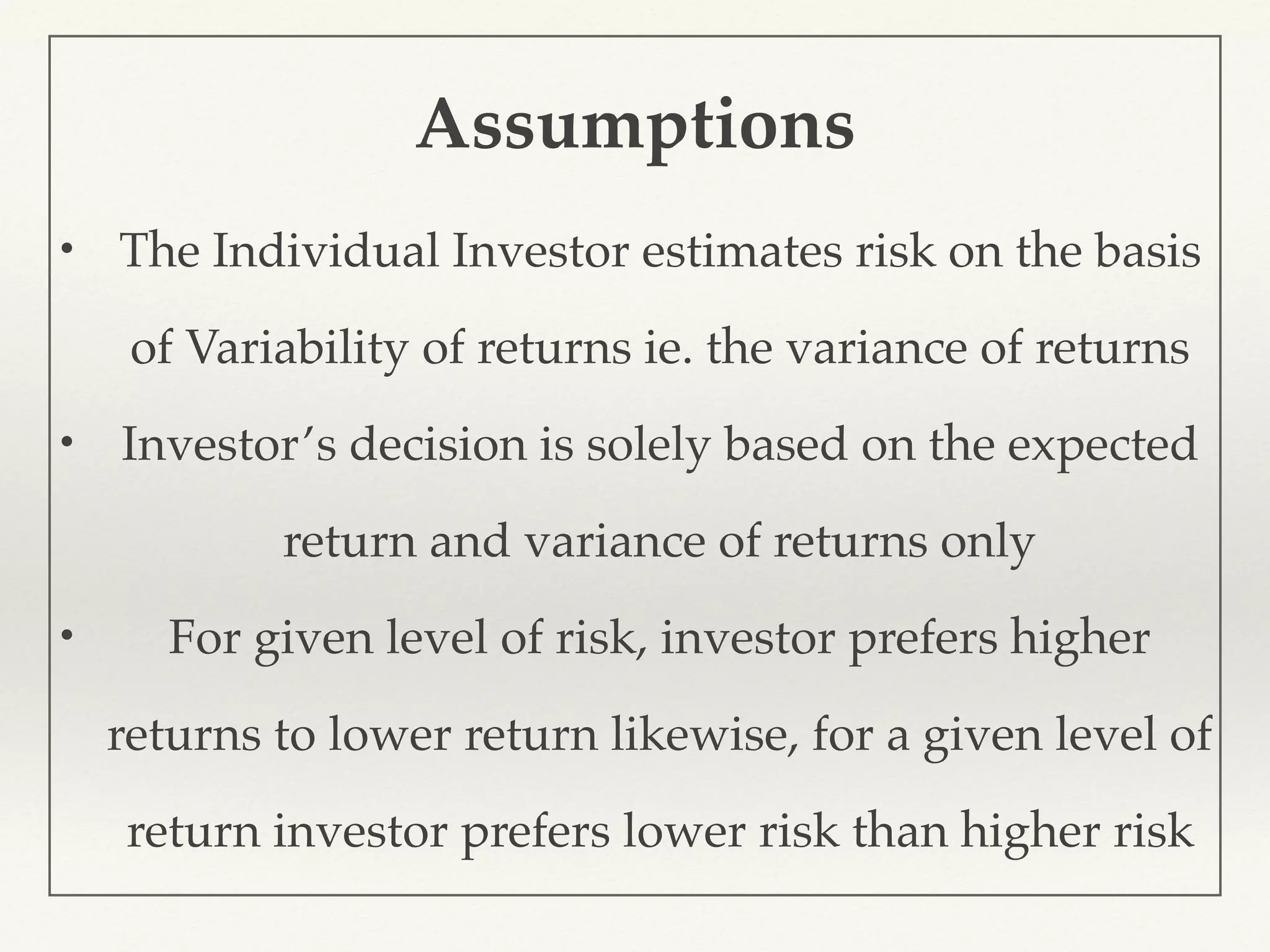

The document discusses the Markowitz portfolio model introduced by Harry Markowitz in March 1952, emphasizing the importance of stock return correlation and expected returns in portfolio management. It highlights how diversification can minimize portfolio risk, particularly unsystematic risk, and provides insights on optimizing portfolios while balancing risk and return preferences for investors. The model suggests that holding multiple securities is generally less risky compared to a single stock, appealing to risk-averse investors.