Downloaded 309 times

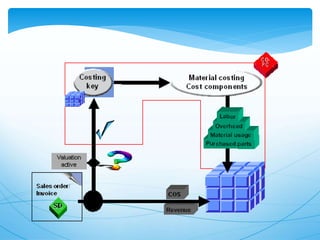

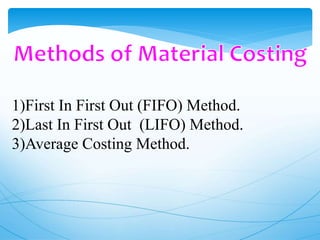

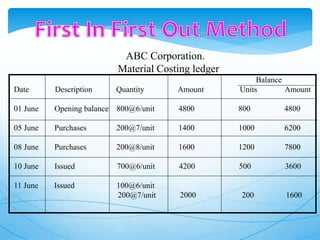

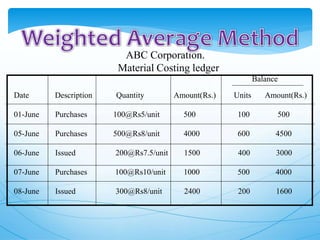

This document discusses material costing methods and inventory management concepts. It provides examples to calculate ordering point, minimum point, maximum point, and danger level using formulas and given values for average daily usage, lead times, minimum/maximum requirements, and economic order quantities. Different material costing methods like FIFO, LIFO, and weighted average are also explained along with examples to demonstrate how to apply each method.