Downloaded 48 times

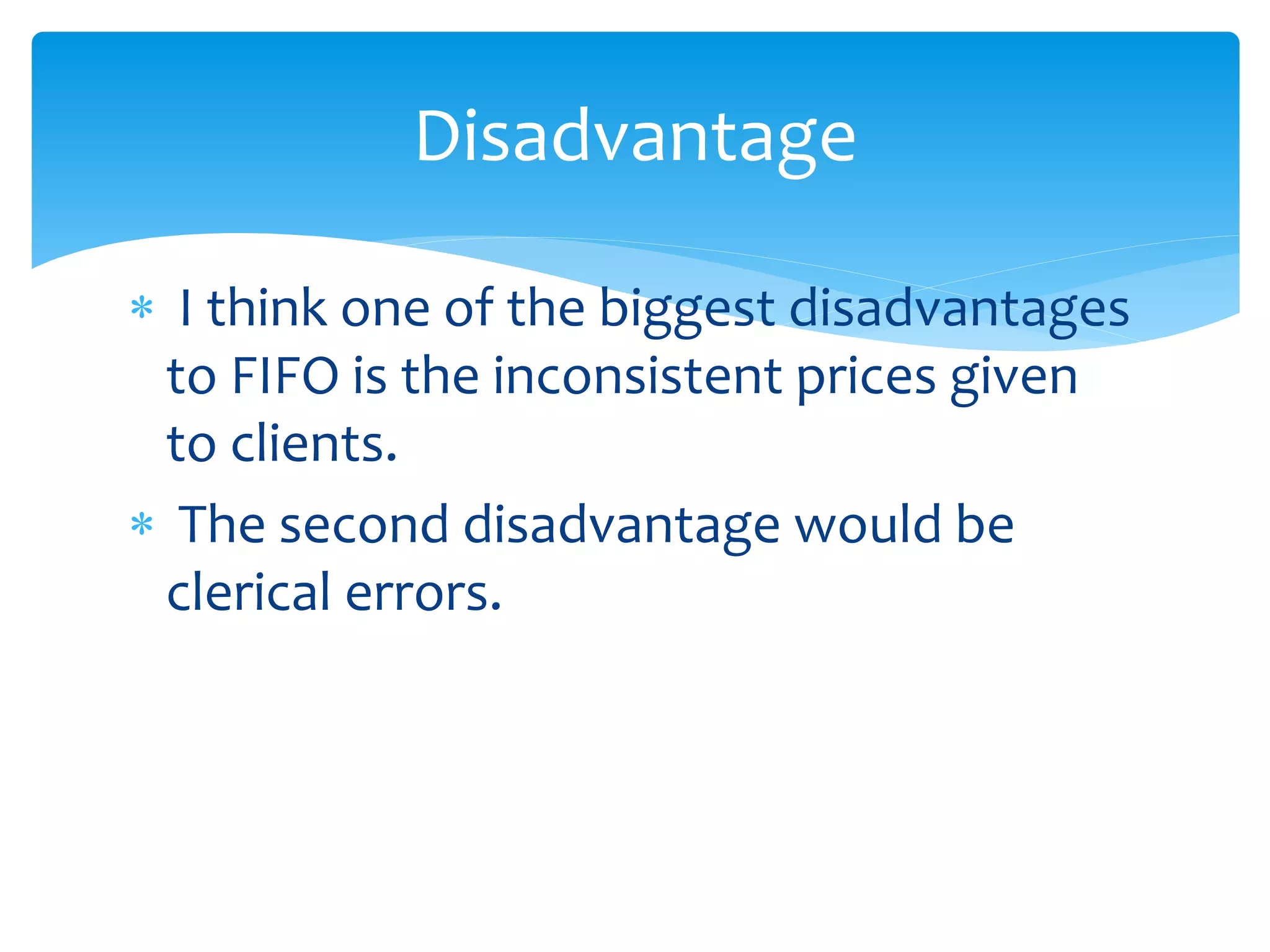

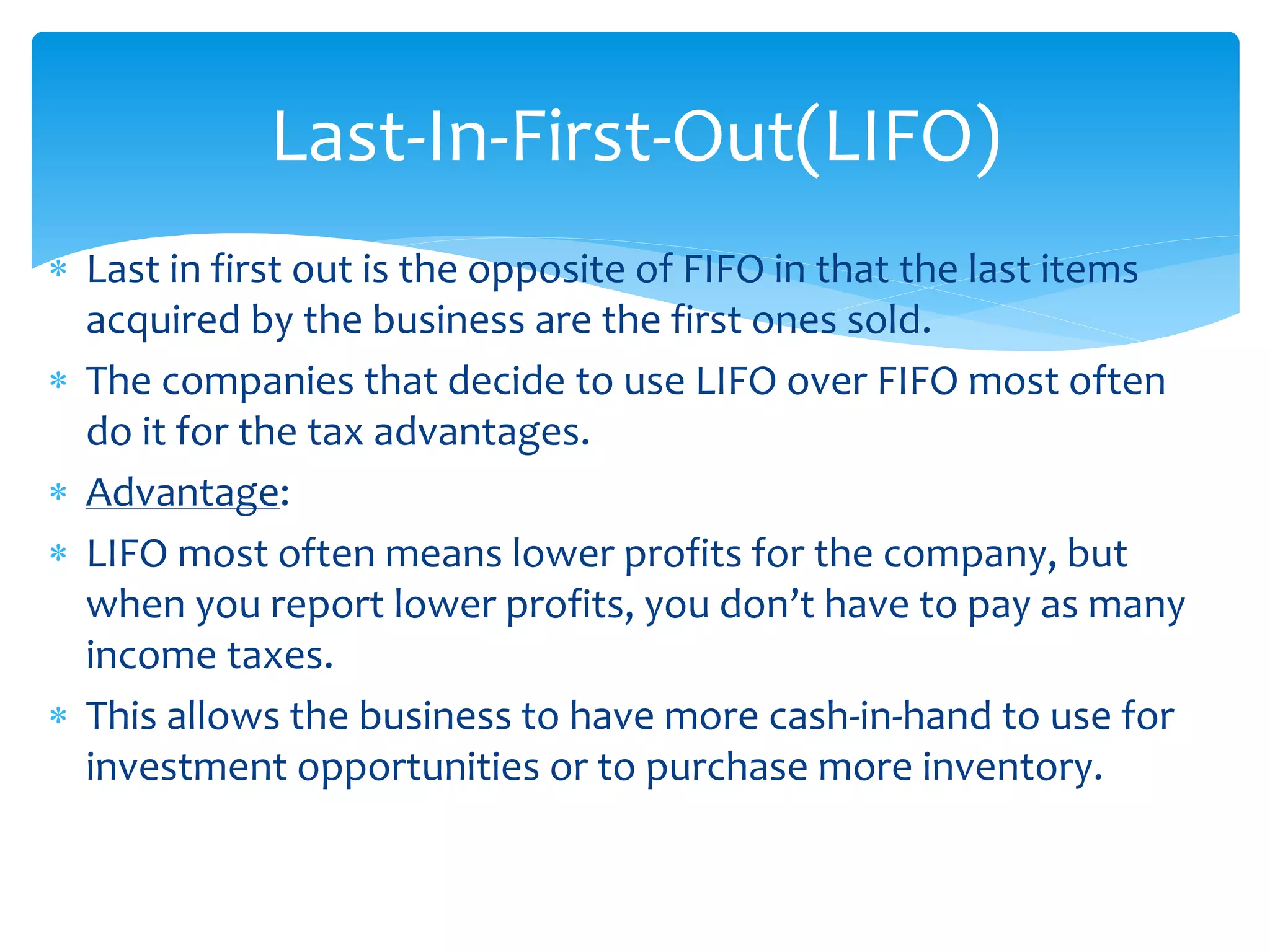

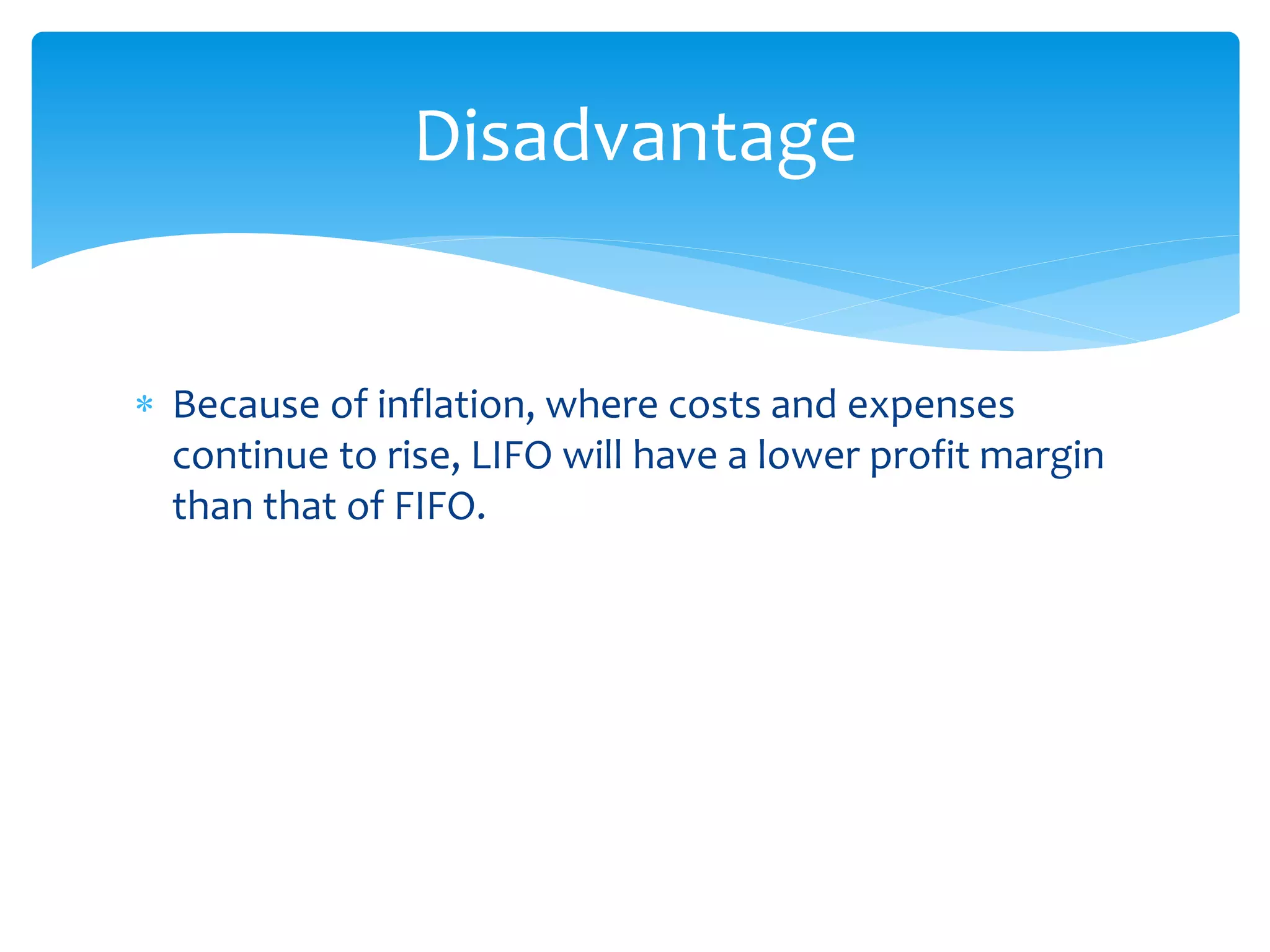

This document discusses material control and inventory valuation methods. It defines materials and supplies that are used in the manufacturing process. Material control aims to ensure adequate quality and quantity of materials for production with minimal costs. The objectives of material control are to prevent overstocking and understocking while protecting materials from loss and waste. Valuation methods like FIFO and LIFO are also covered, where FIFO assumes the first materials purchased are the first sold and LIFO is the opposite.