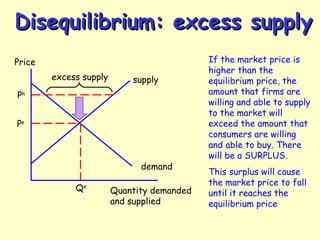

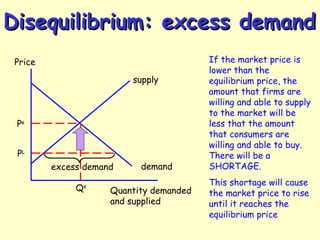

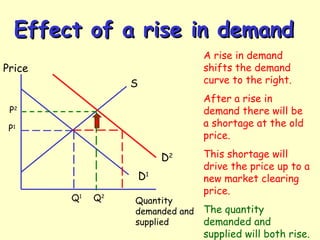

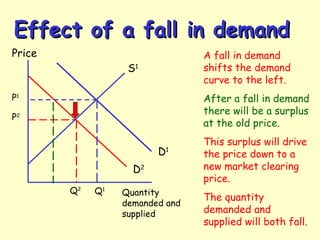

The document discusses market equilibrium and how supply and demand interact to determine price and quantity in competitive markets. It defines equilibrium price as the price where the quantity demanded is equal to the quantity supplied, resulting in no shortages or surpluses. Disequilibrium occurs when demand and supply are not equal at the existing price, resulting in either a shortage or surplus. The document provides examples of how prices and quantities adjust to changes in demand or supply through shifts in the curves to restore equilibrium. Tasks are included applying these concepts to real world market situations.