Downloaded 52 times

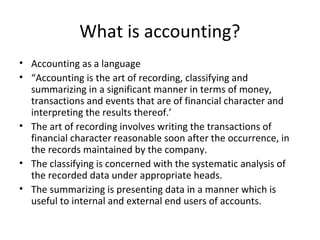

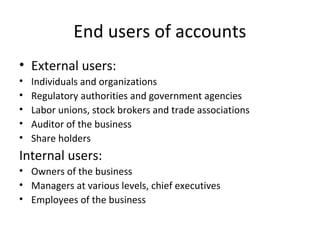

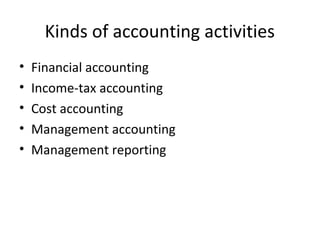

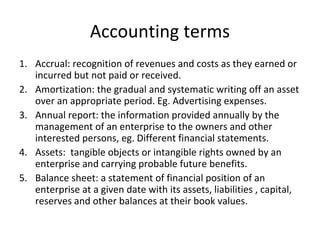

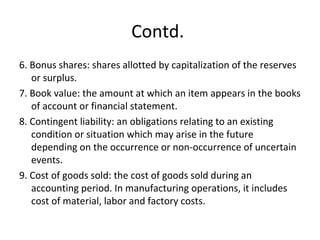

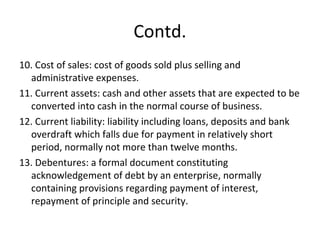

This document provides an introduction to accounting. It defines accounting as recording, classifying, and summarizing financial transactions and events in terms of money. Accounting involves recording transactions, classifying data into appropriate categories, and summarizing data to be useful for internal and external users. It discusses the different types of accounting activities and various accounting terms such as assets, liabilities, revenues, expenses, and financial statements.