Download to read offline

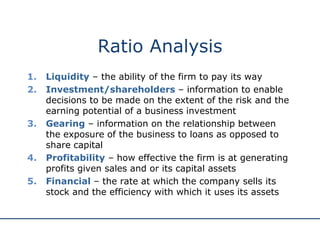

The document provides an overview of financial statement and ratio analysis. It discusses the objectives of ratio analysis which include standardizing financial information, evaluating current operations, and comparing performance. It then examines various types of ratios that can be analyzed including liquidity, investment/shareholders, gearing, profitability, and financial ratios. Specific ratios are defined under each category such as current ratio, quick ratio, debt-to-equity ratio, gross profit margin, return on capital employed, asset turnover, and stock turnover. The document emphasizes that multiple ratios should be analyzed over several years for accurate assessment of a firm's financial condition.