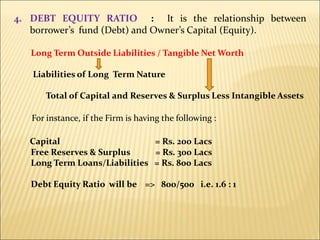

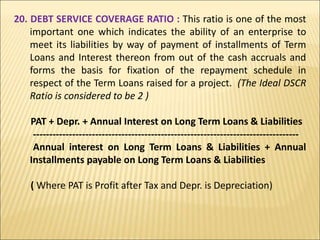

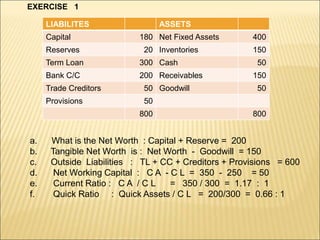

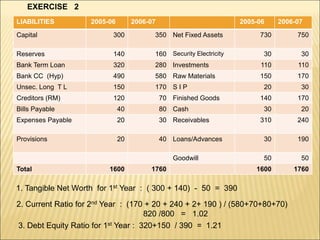

This document provides information on ratio analysis for financial statement evaluation. It defines various types of ratios including liquidity, activity, profitability, leverage and market ratios. Specific ratios discussed include current ratio, quick ratio, debt-equity ratio, gross profit ratio, return on equity, earnings per share and price-earnings ratio. The purpose, calculation and ideal levels of these ratios are explained. Sample balance sheet formats and ratio calculations are also presented to illustrate the concepts.

![5. PROPRIETARY RATIO : This ratio indicates the extent to which

Tangible Assets are financed by Owner’s Fund.

Proprietary Ratio = (Tangible Net Worth/Total Tangible

Assets) x 100

The ratio will be 100% when there is no Borrowing for purchasing

of Assets.

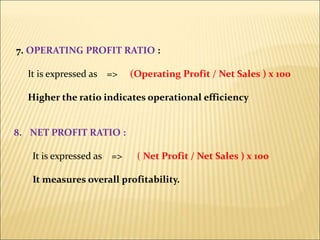

6. GROSS PROFIT RATIO : By comparing Gross Profit percentage to

Net Sales we can arrive at the Gross Profit Ratio which indicates the

manufacturing efficiency as well as the pricing policy of the concern.

Gross Profit Ratio = (Gross Profit / Net Sales ) x 100

Alternatively , since Gross Profit is equal to Sales minus Cost of

Goods Sold, it can also be interpreted as below :

Gross Profit Ratio = [ (Sales – Cost of goods sold)/ Net Sales]

x 100

A higher Gross Profit Ratio indicates efficiency in production of the unit.](https://image.slidesharecdn.com/ratioanalysis-221112135356-d964e6d1/85/RATIO-ANALYSIS-ppt-12-320.jpg)

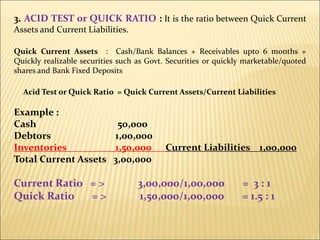

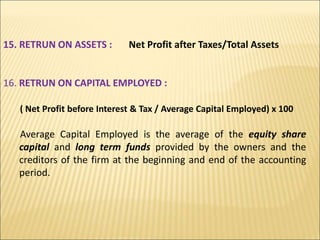

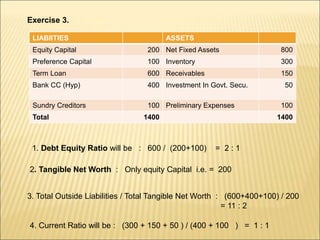

![LIABILITIES ASSETS

Capital + Reserves 355 Net Fixed Assets 265

P & L Credit Balance 7 Cash 1

Loan From S F C 100 Receivables 125

Bank Overdraft 38 Stocks 128

Creditors 26 Prepaid Expenses 1

Provision of Tax 9 Intangible Assets 30

Proposed Dividend 15

550 550

Q . What is the Proprietary Ratio ? Ans : (T NW / Tangible Assets) x 100

[ (362 - 30 ) / (550 – 30)] x 100

(332 / 520) x 100 = 64%

Q . What is the Net Working Capital ?

Ans : C. A - C L. = 255 - 88 = 167

Q . If Net Sales is Rs.15 Lac, then What would be the Stock Turnover

Ratio in Times ? Ans : Net Sales / Average Inventories/Stock

1500 / 128 = 12 times approximately

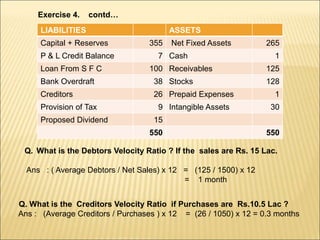

Exercise 4. contd…](https://image.slidesharecdn.com/ratioanalysis-221112135356-d964e6d1/85/RATIO-ANALYSIS-ppt-23-320.jpg)