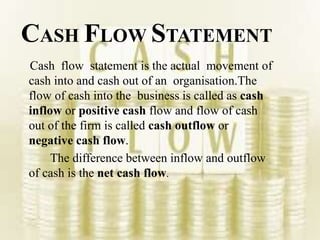

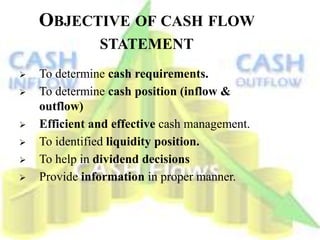

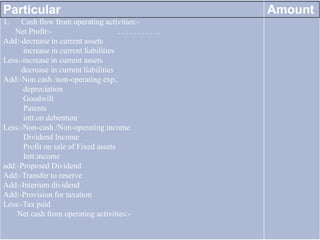

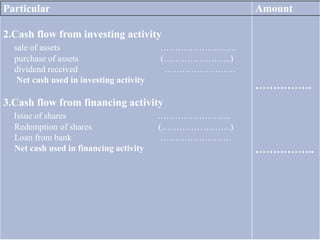

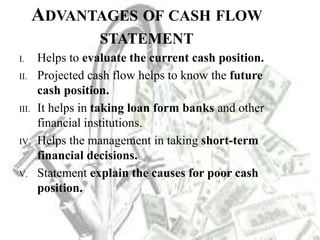

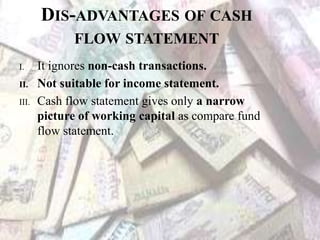

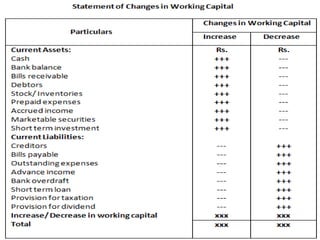

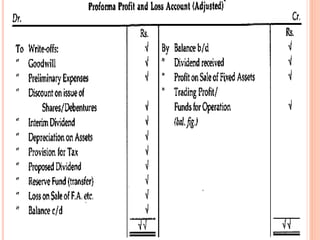

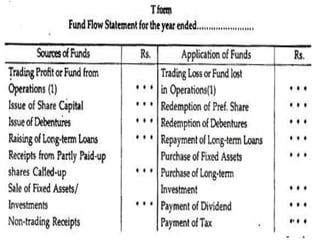

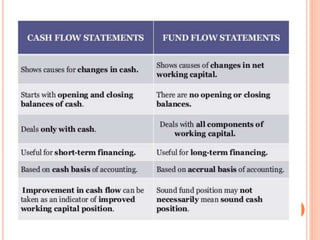

The document discusses cash flow and fund flow statements, explaining their definitions, objectives, and components. It highlights the advantages and disadvantages of each statement, noting that cash flow focuses on the actual movement of cash while fund flow illustrates changes in balance sheet items. The document emphasizes the importance of these statements in financial management and decision-making.