Downloaded 97 times

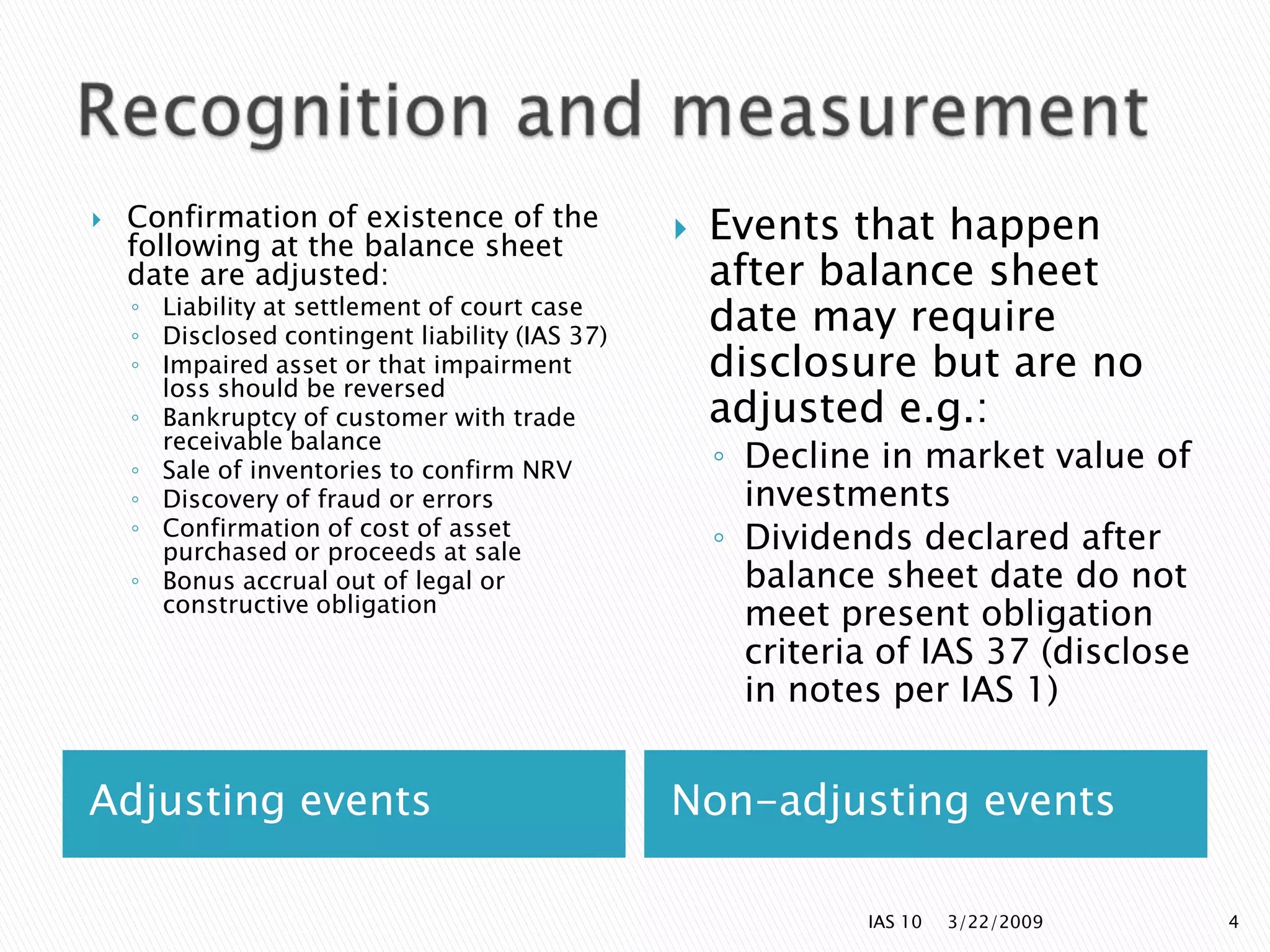

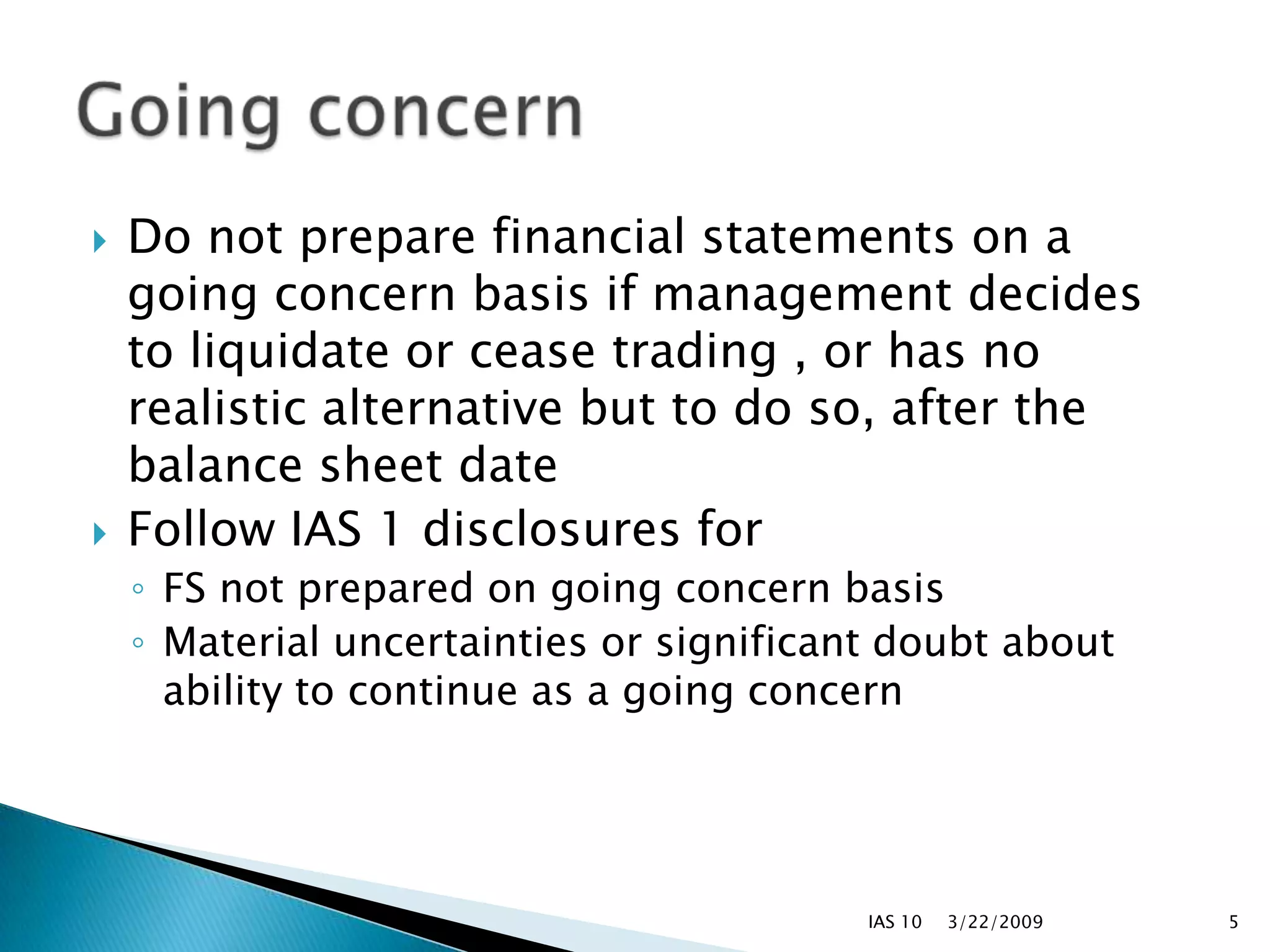

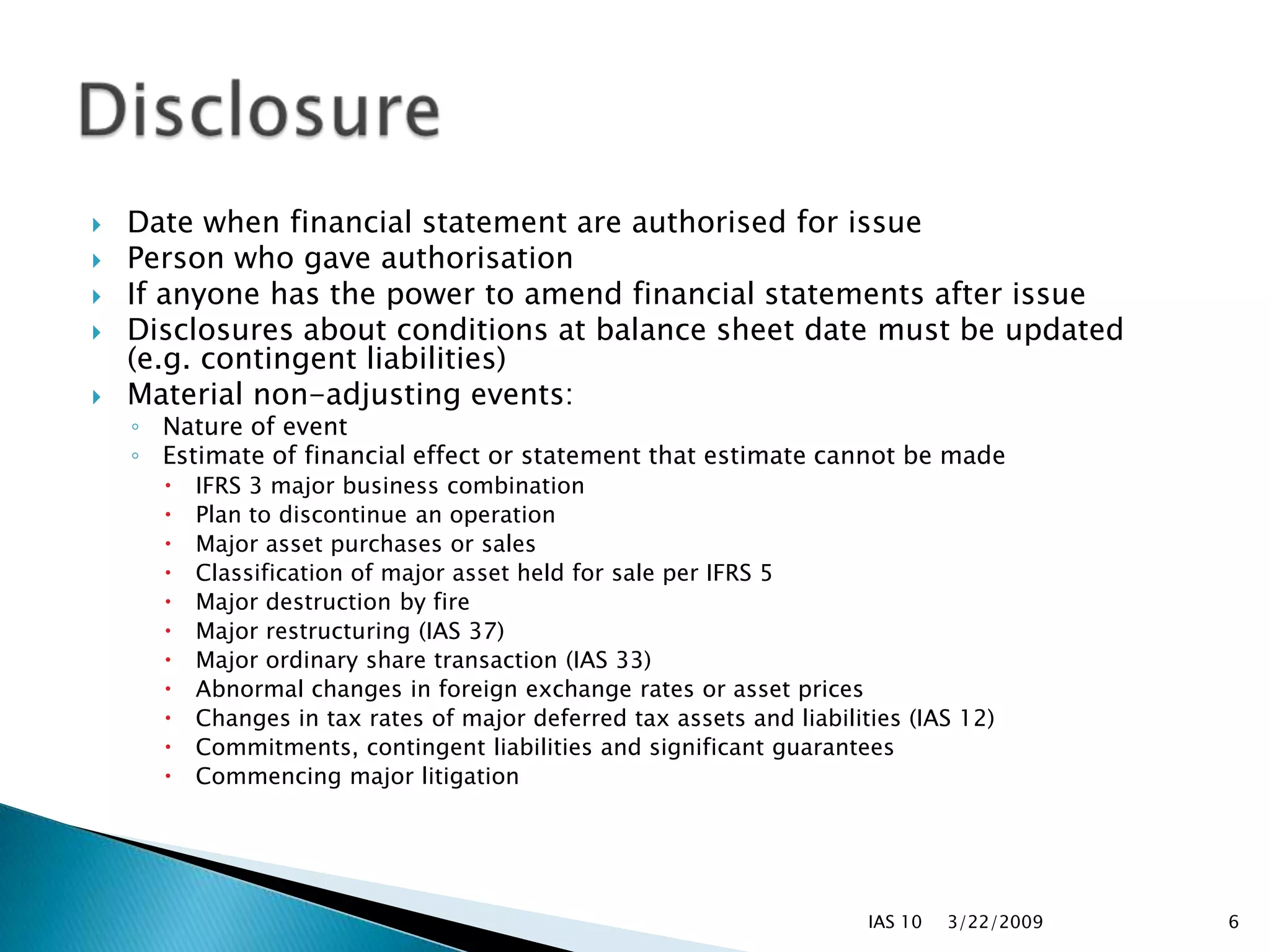

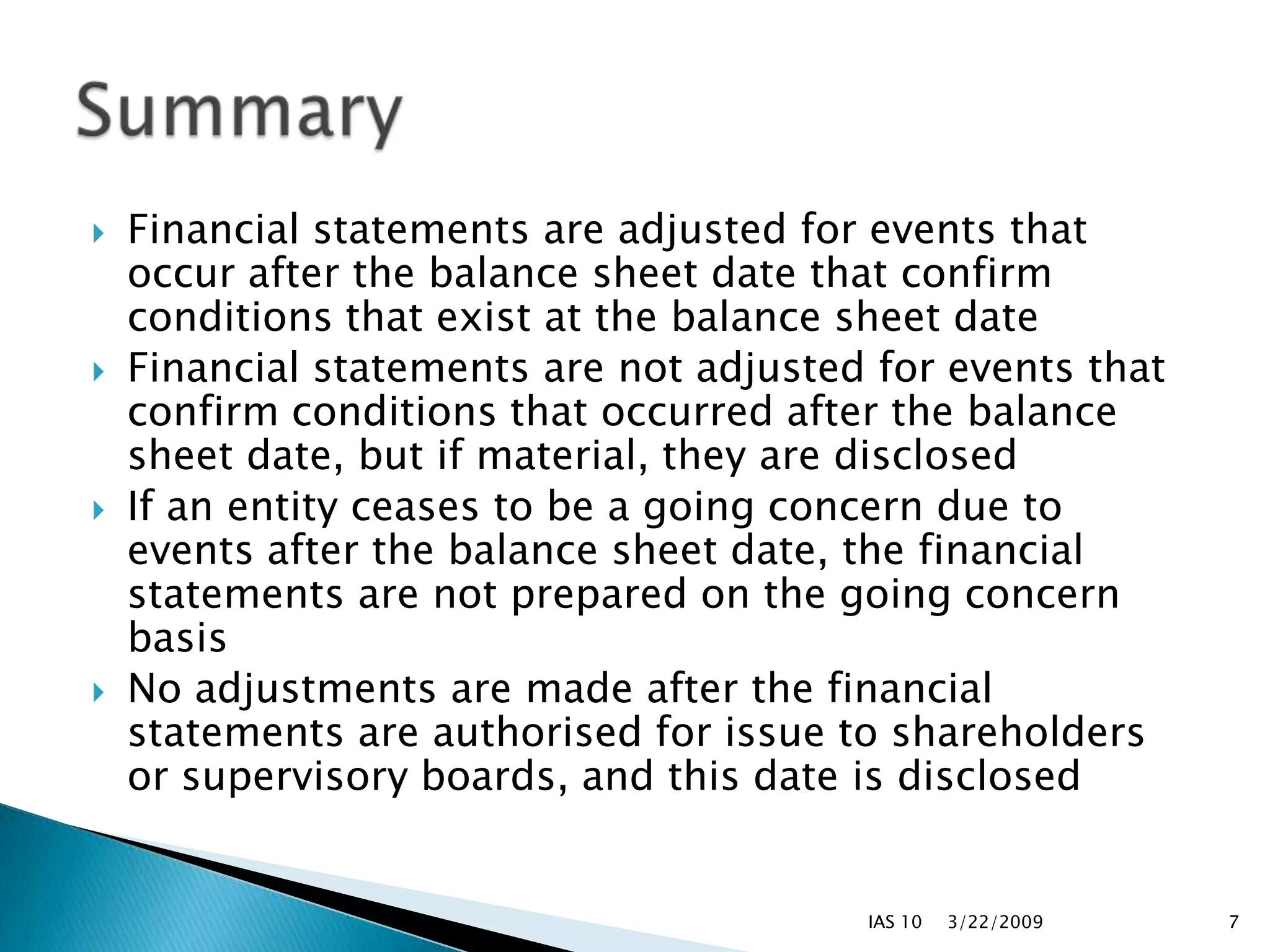

IAS 10 prescribes the accounting treatment and disclosures required for events that occur after the balance sheet date but before financial statements are authorized for issue. It distinguishes between adjusting events that provide evidence of conditions that existed at the balance sheet date and non-adjusting events that are indicative of conditions that arose after that date. Financial statements must be adjusted for subsequent adjusting events, but not for non-adjusting events, although the latter may need to be disclosed. The standard also addresses the assessment of going concern and specifies certain additional disclosures required regarding the authorization date of the financial statements and material post-balance sheet date events or conditions.

![AUDIT REPORT [ AUDITING ]](https://cdn.slidesharecdn.com/ss_thumbnails/auditingtypesofauditreport-210303052610-thumbnail.jpg?width=640&height=640&fit=bounds)

![Definitions[1]](https://cdn.slidesharecdn.com/ss_thumbnails/definitions1-111024070329-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)