Downloaded 80 times

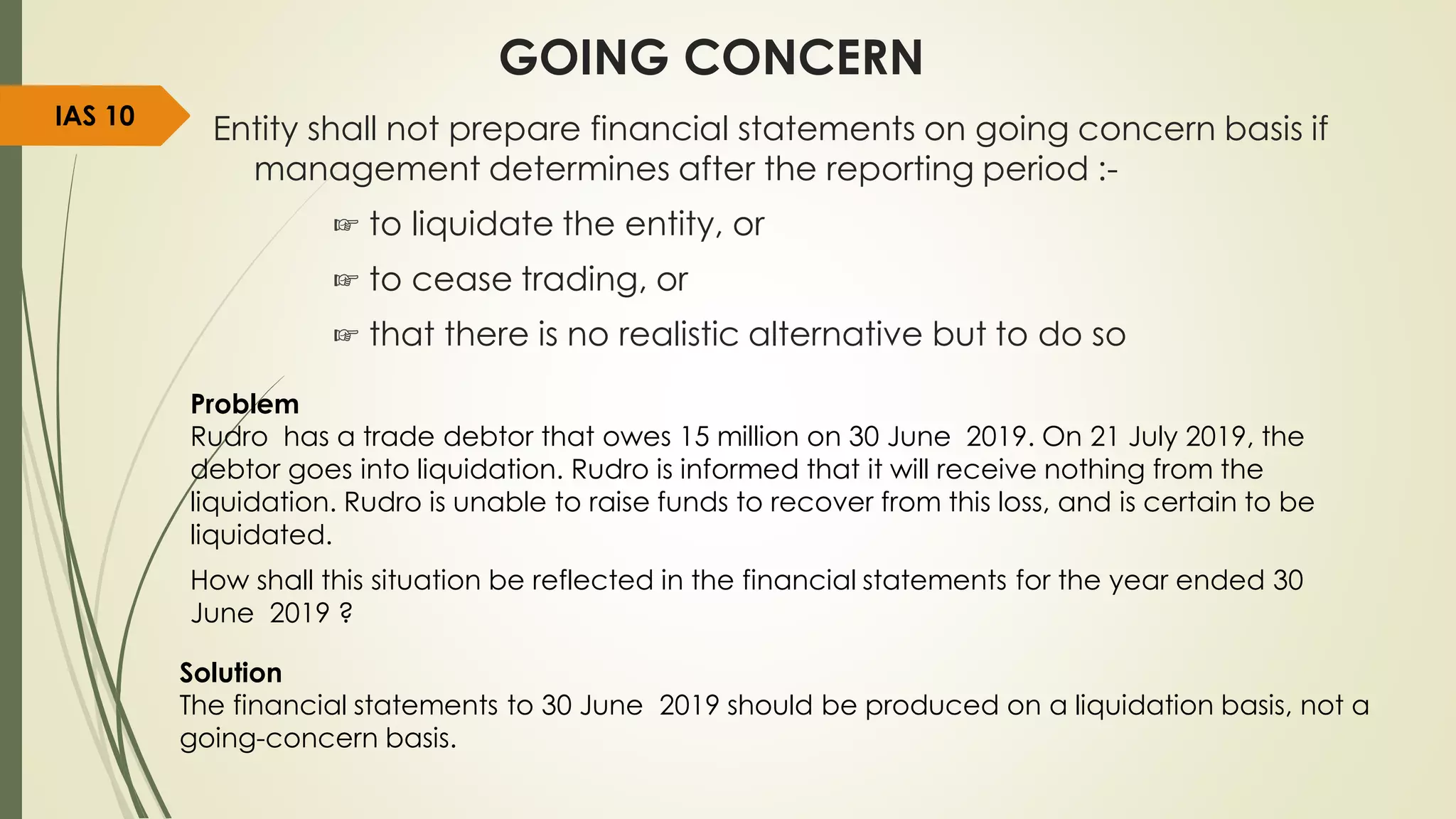

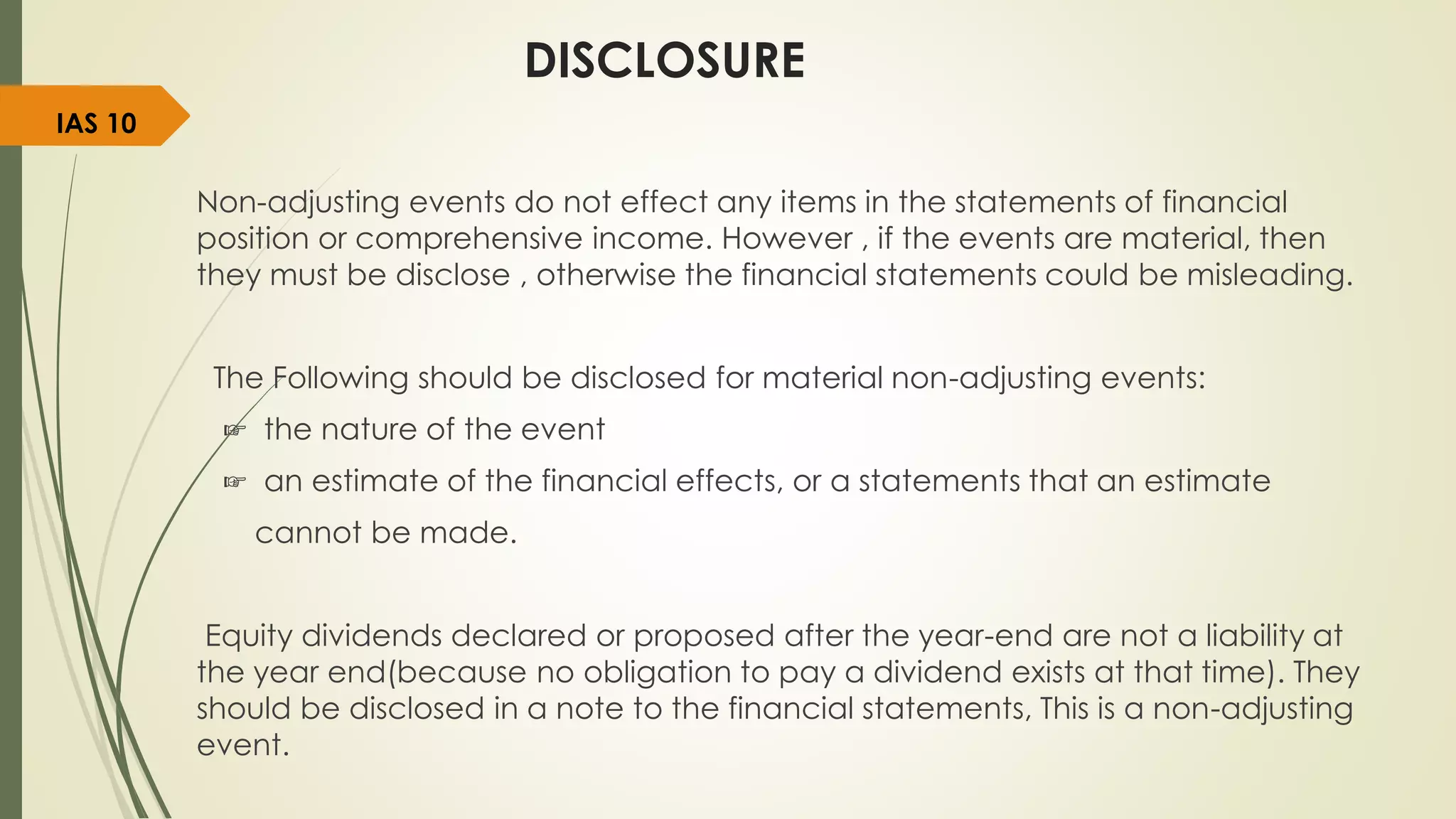

This document summarizes the key points of IAS 10 Events After the Reporting Period. It discusses the definition of an authorized issue date and the two types of events - adjusting events and non-adjusting events. Adjusting events require adjustment to the financial statements if they provide evidence of conditions existing at the reporting date. Non-adjusting events do not result in adjustment but require disclosure of the nature and estimated financial effects. It also covers going concern assessment and treatment of dividends declared after the reporting period.