Downloaded 55 times

The document discusses IFRS 2, which provides guidance on accounting for share-based payment transactions. It summarizes key aspects of IFRS 2 including scope, valuation techniques, vesting conditions, journal entries, tax treatment, transition, and disclosure requirements. Valuation of share options requires estimation and the use of models, with complexity depending on factors like performance conditions. An expense is recognized over the vesting period and adjustments made if fair value estimates change.

Example of a media group offering share options to align employee incentives with company goals.

IFRS 2 applies broadly, but excludes certain transactions under Business Combinations and IAS 39.

Fair value valuation is required but lacks specified procedures, often needing expert assistance.

Valuation can be expensive; intrinsic value is used if market value is unavailable, needing careful assessment.

Key components like date of grant, vesting period, conditions, and exercise date of share options detailed.

Following option exercise, expense is recorded, affecting accounts and requiring estimates of total costs.

Example calculation for share option liability accounting when employees don't all remain with the company.

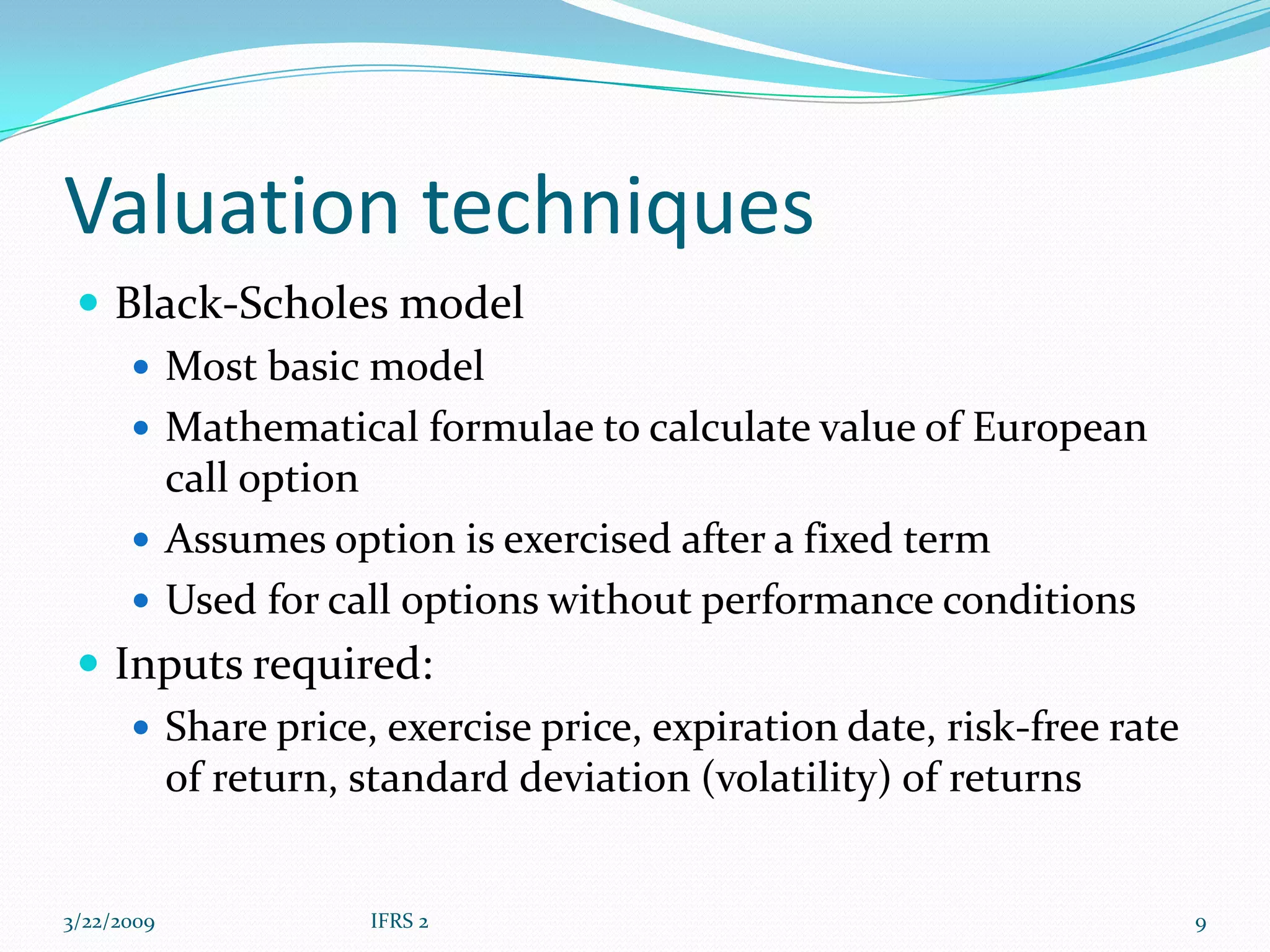

Black-Scholes model explained for European call options, requiring various market inputs for calculations.

Binomial and Monte-Carlo models as alternative approaches for option valuation, each with distinct capabilities.

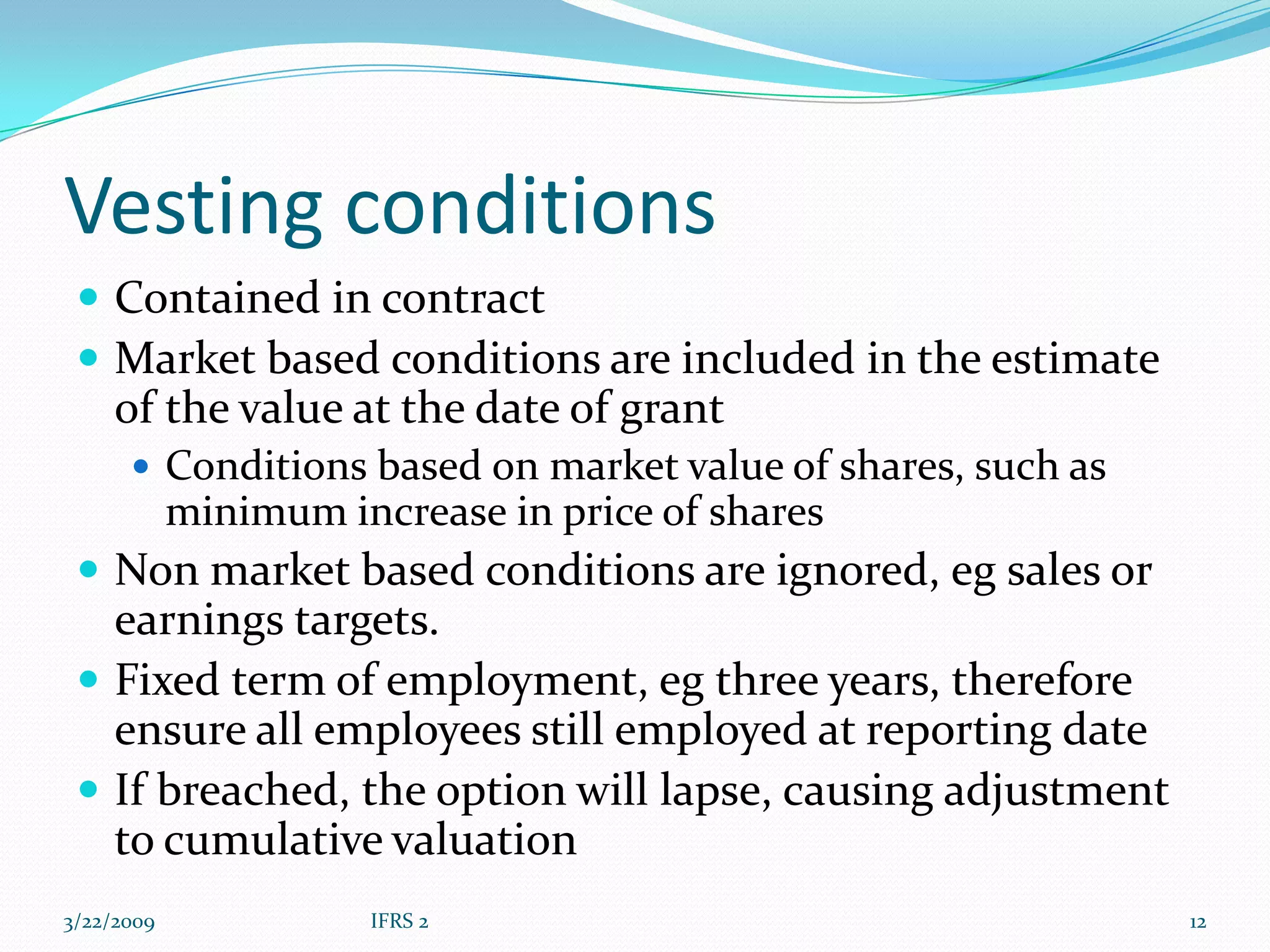

Details on market vs. non-market vesting conditions included in valuation and the importance of employment status.

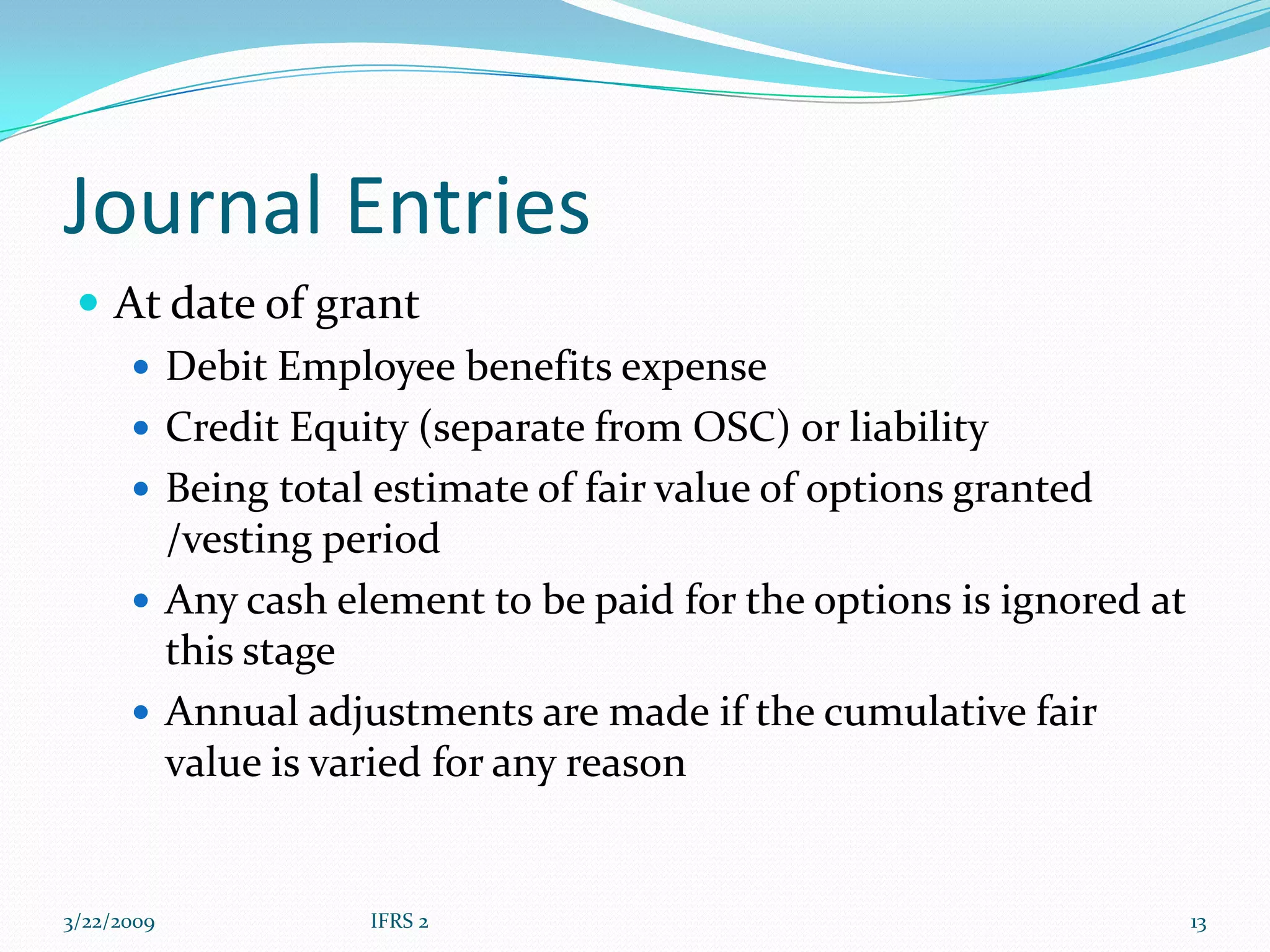

Accounting entries required at grant and exercise of options to reflect fair value and cash proceeds accurately.

The timing difference between reported profit and taxable profit; recognition of deferred tax assets explained.

Journal entries for taxation related to share options and the steps for managing deferred tax assets.

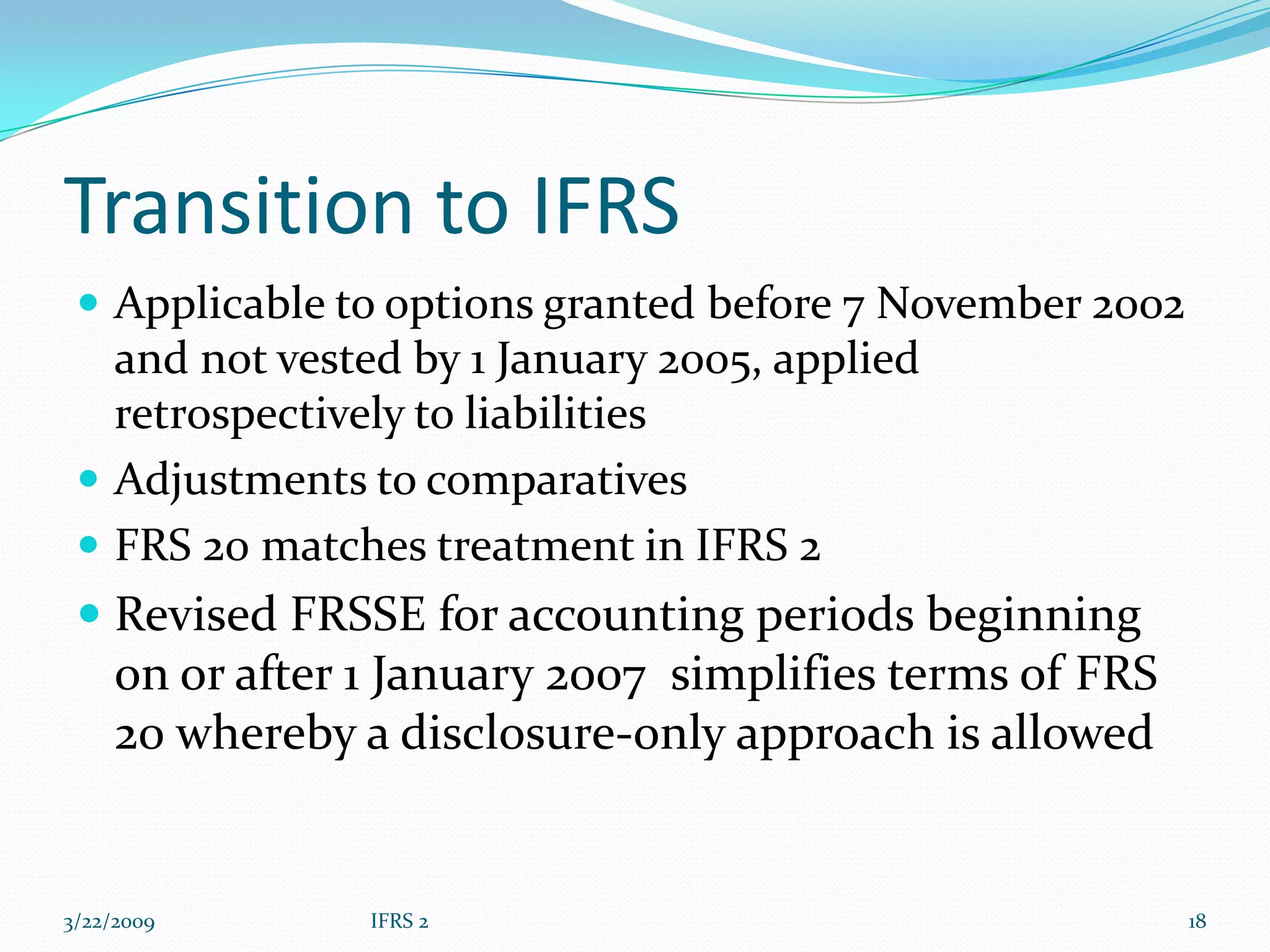

Guidelines for applying IFRS to options granted before 2002, including necessary adjustments.

Key disclosure information required under IFRS regarding expenses, liabilities, and valuation assumptions.