Downloaded 40 times

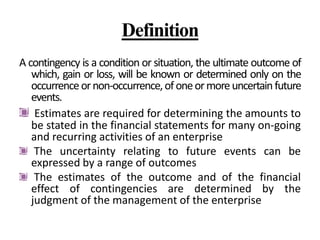

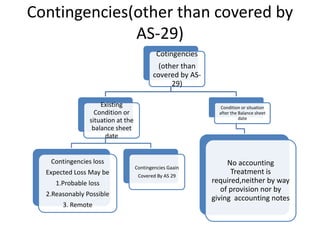

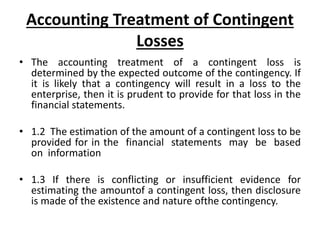

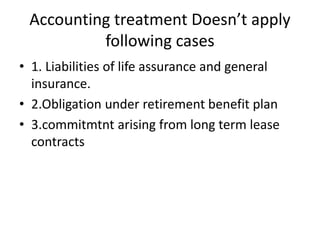

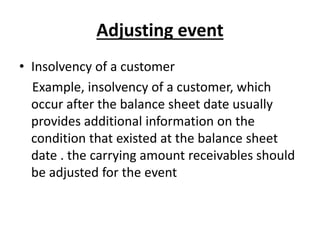

Accounting Standard 4 deals with contingencies and events occurring after the balance sheet date. It defines contingencies as uncertain future events whose outcomes are unknown at the balance sheet date. Estimates are required to account for contingencies in financial statements. Events after the balance sheet date refer to significant events between the balance sheet date and approval of financial statements. Adjusting events require adjustment to amounts in the financial statements, while non-adjusting events require disclosure in notes only.