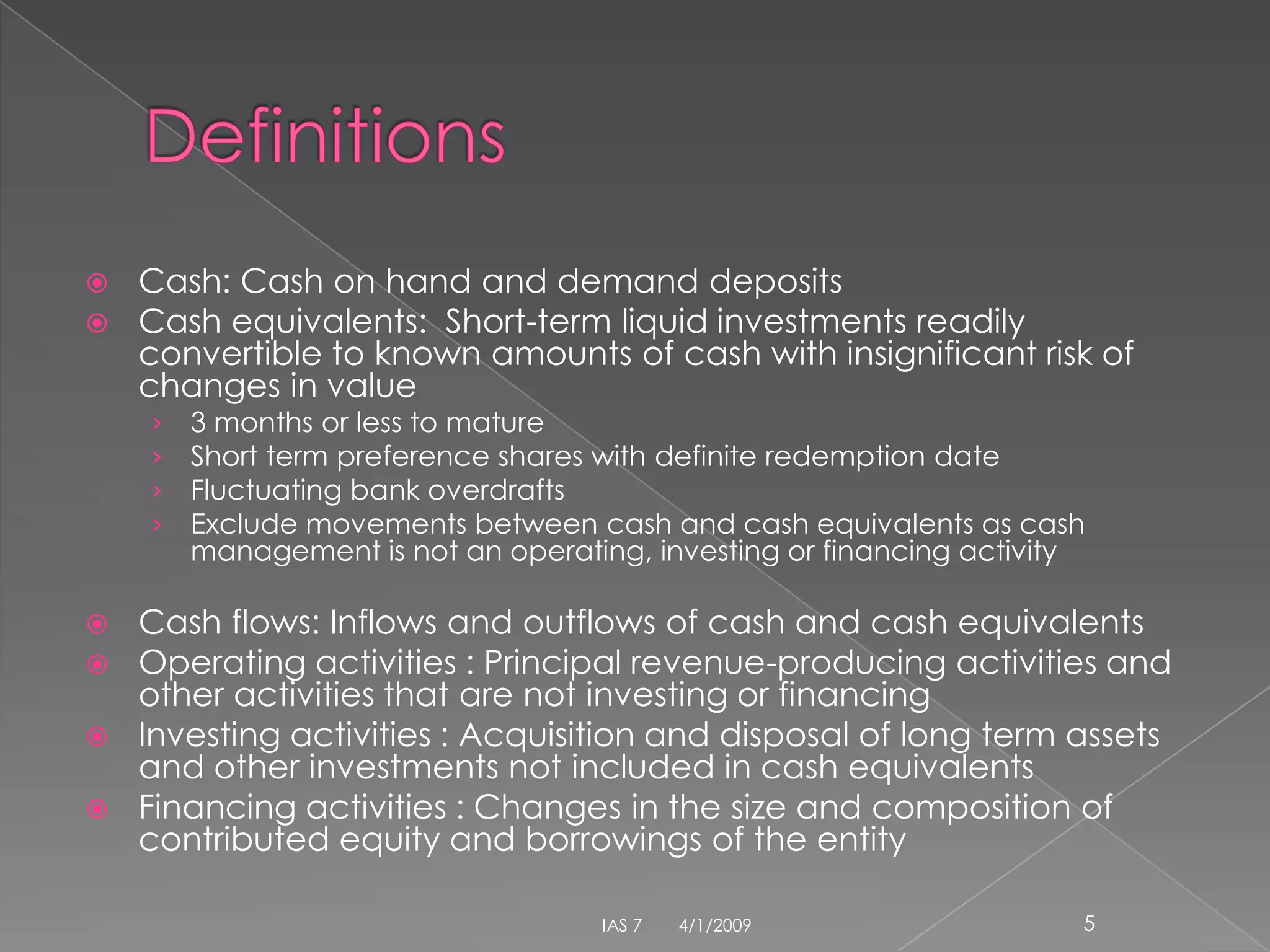

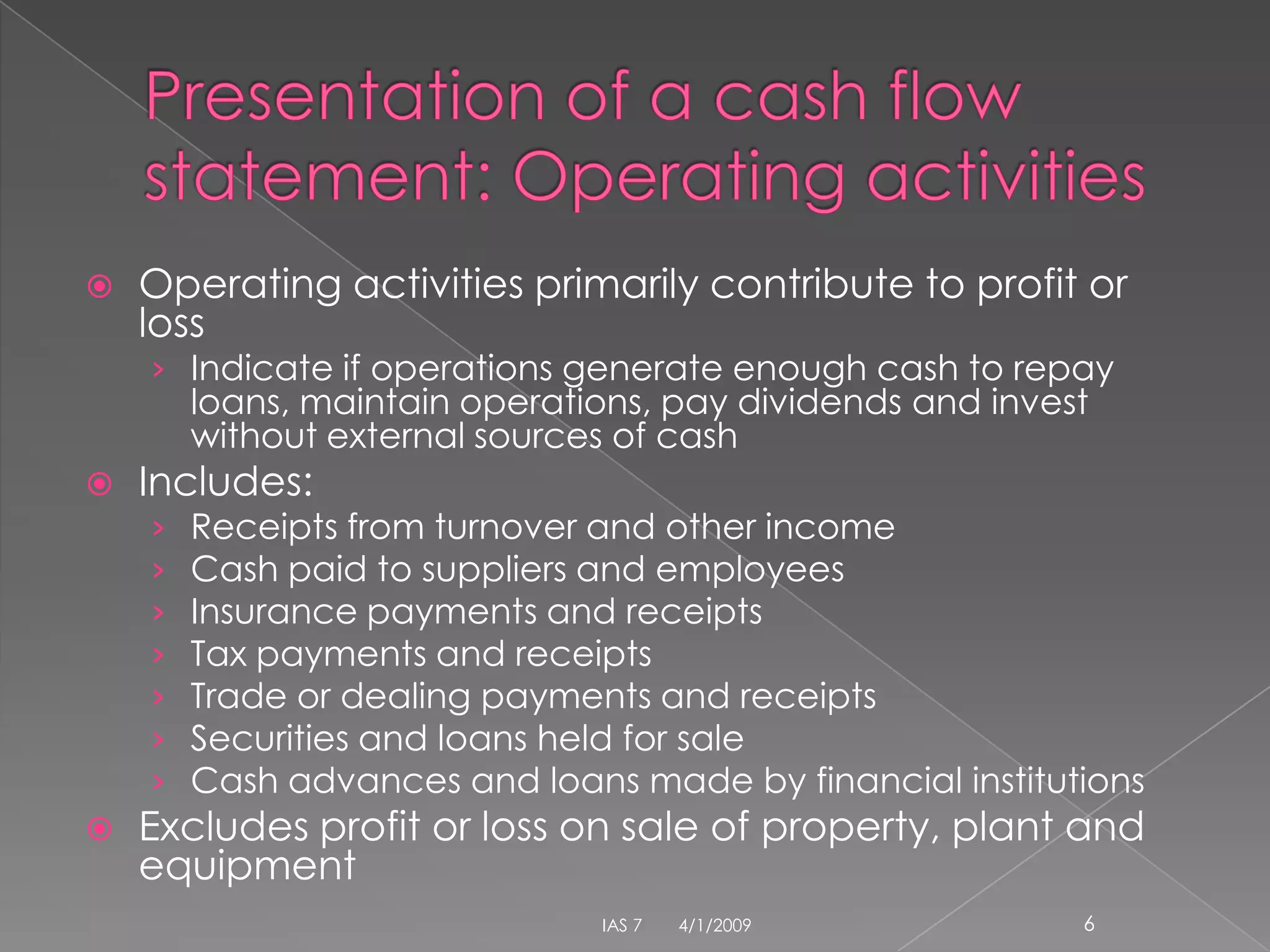

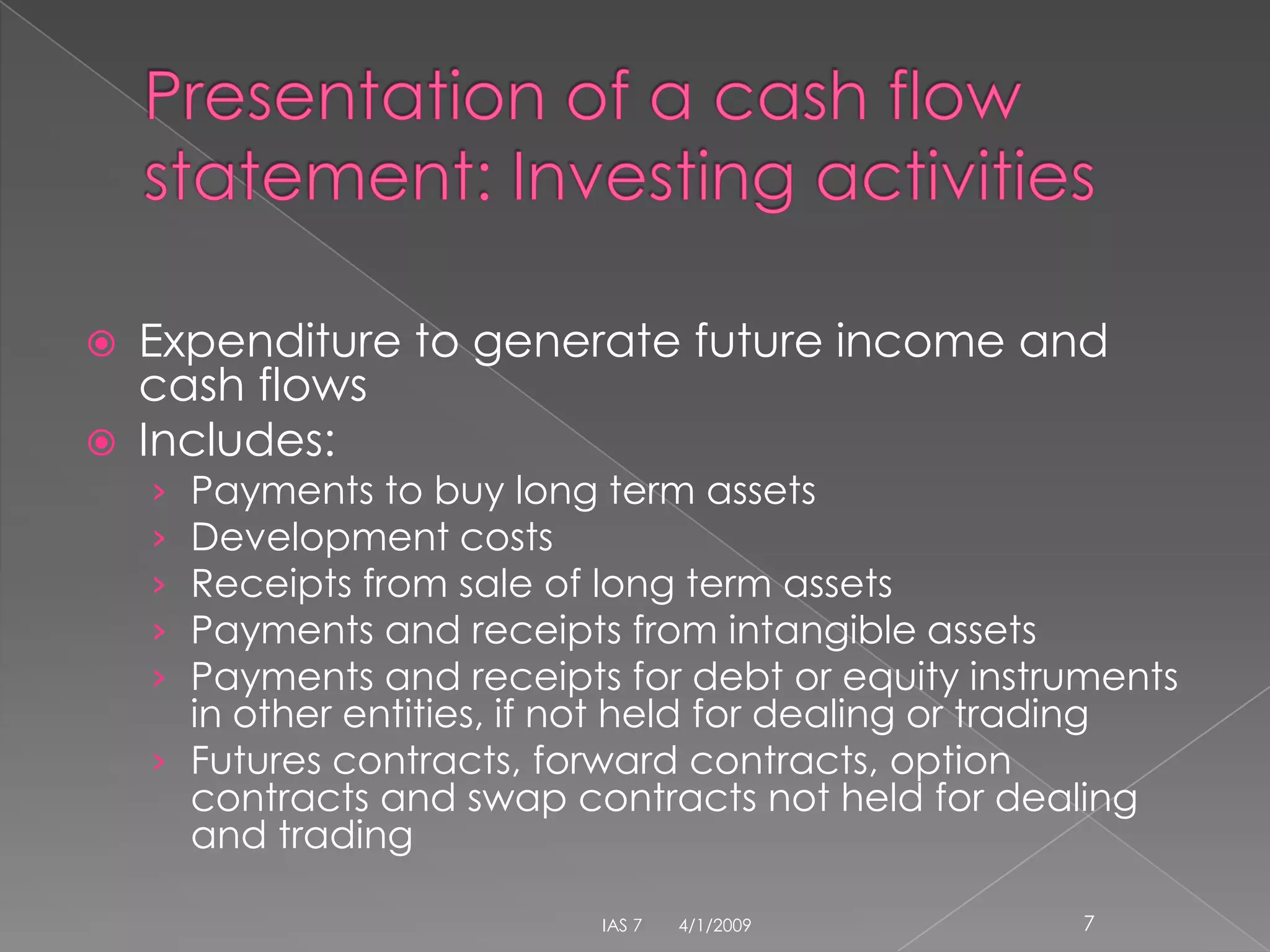

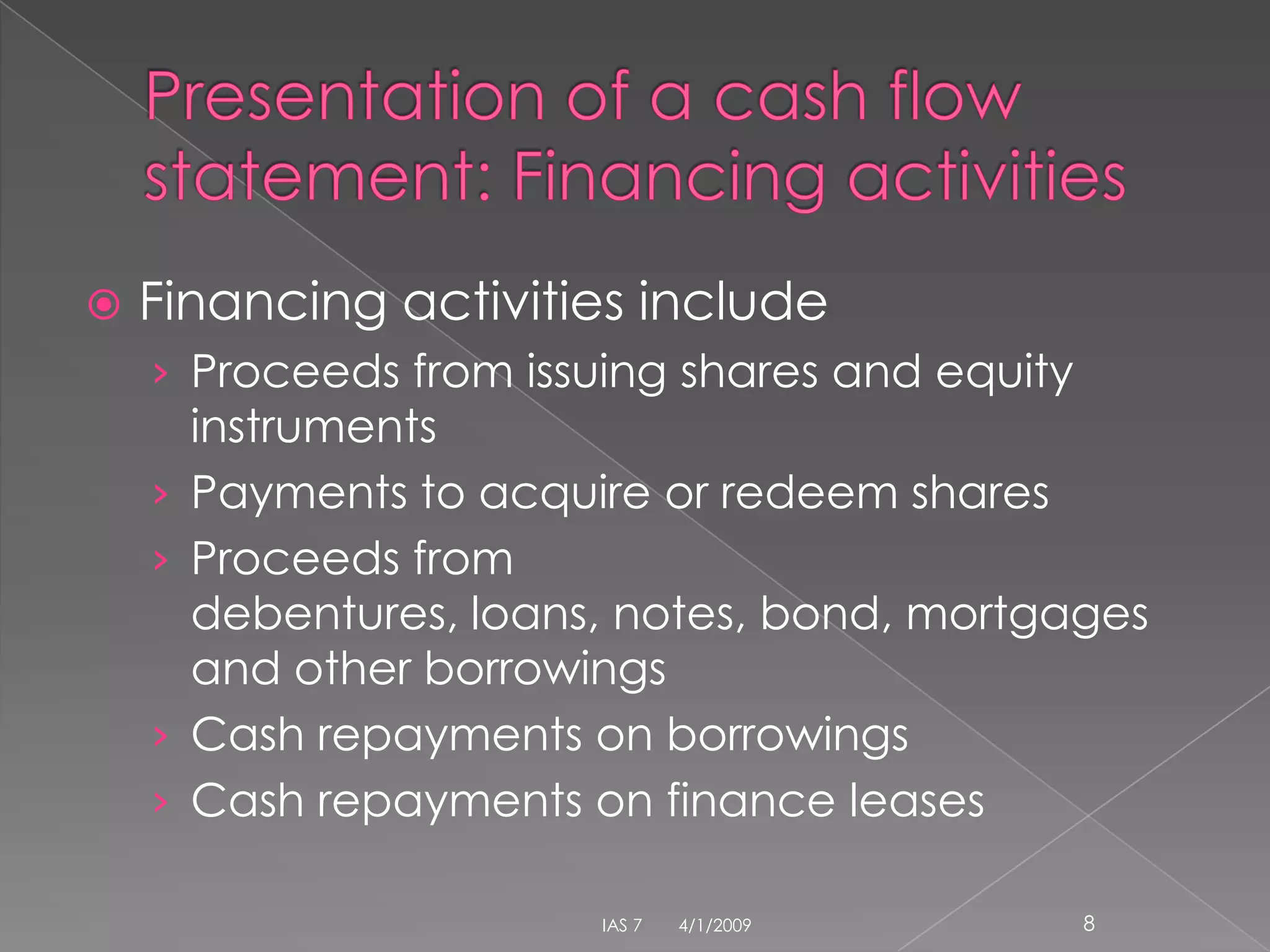

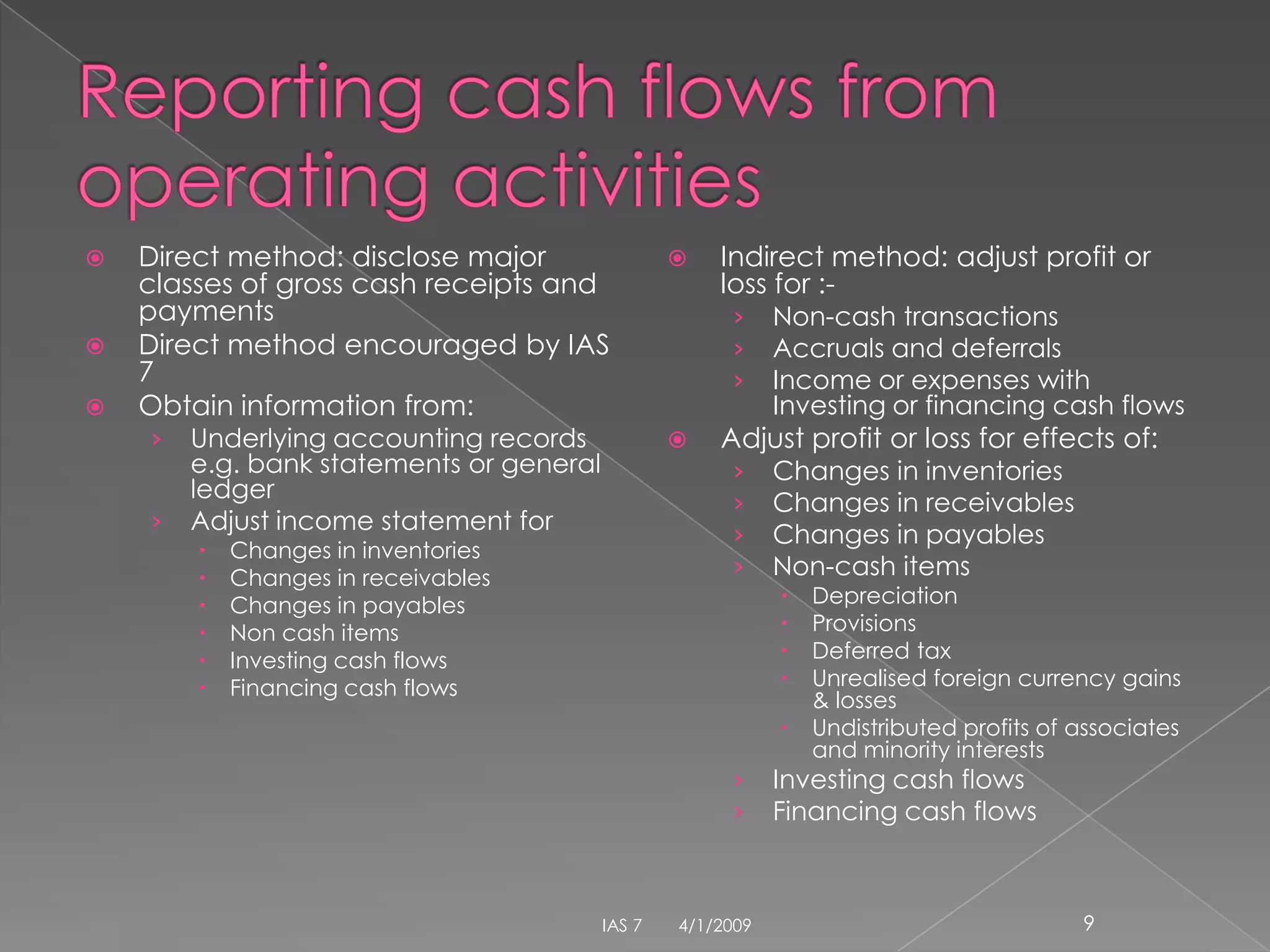

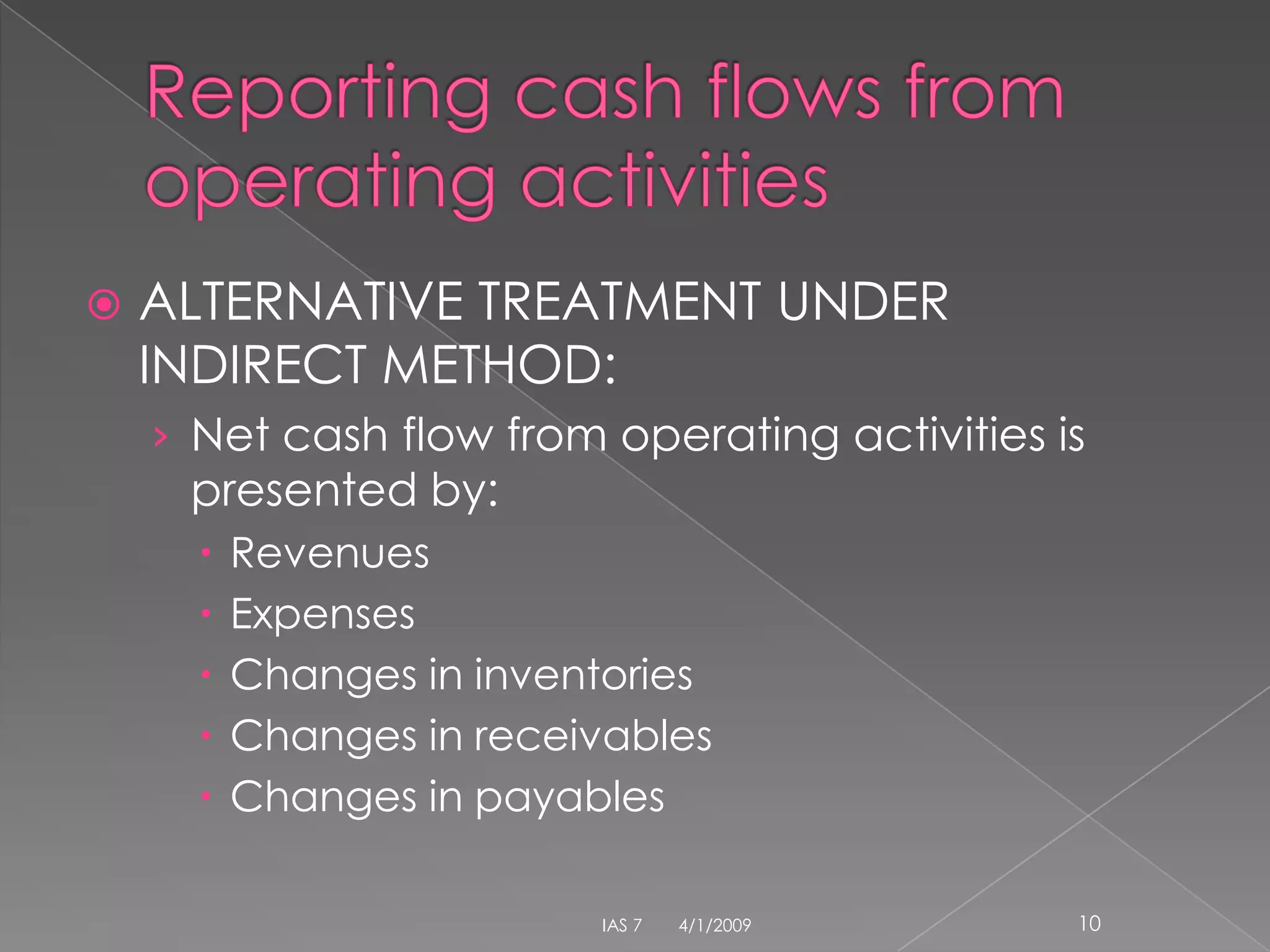

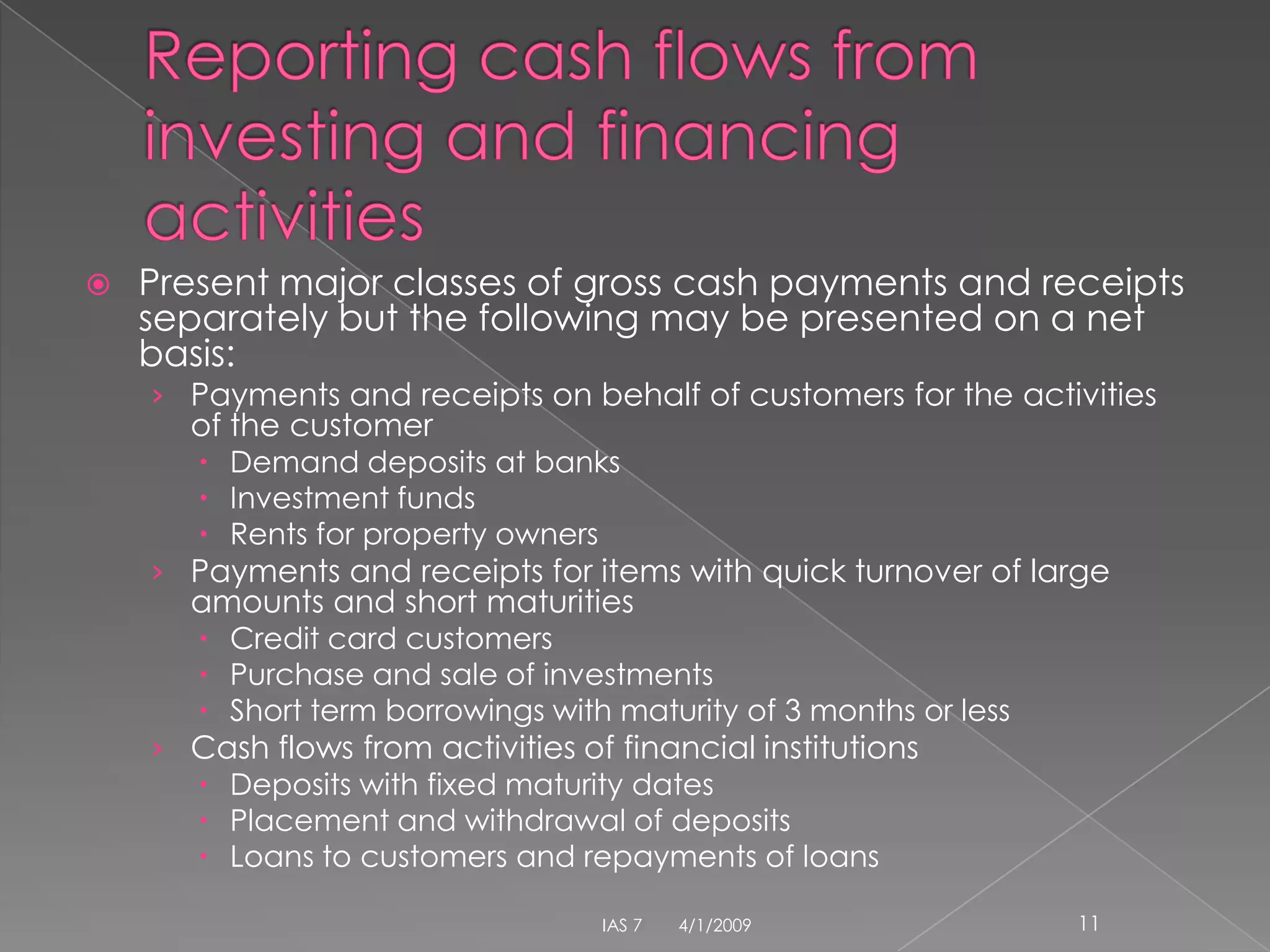

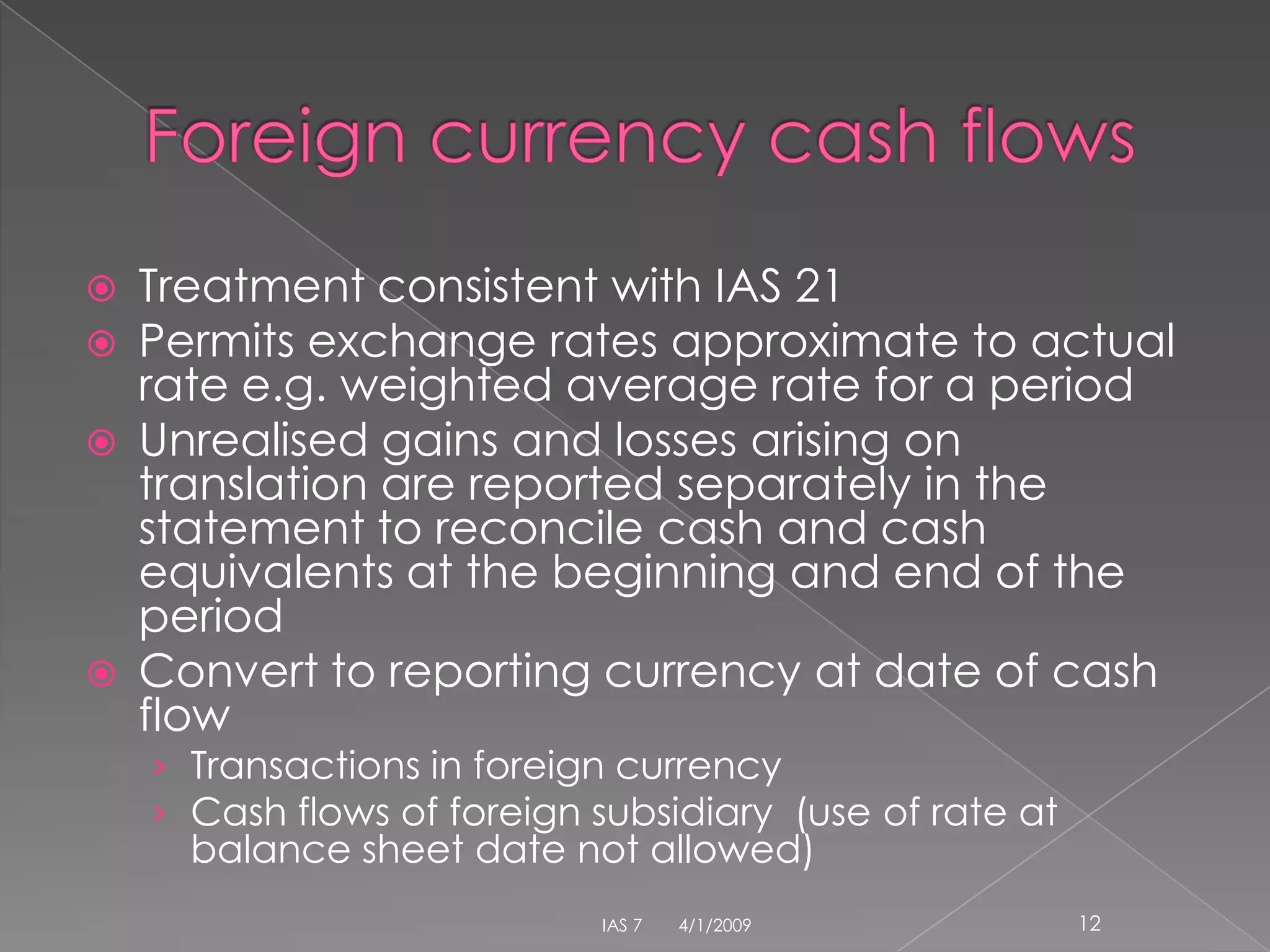

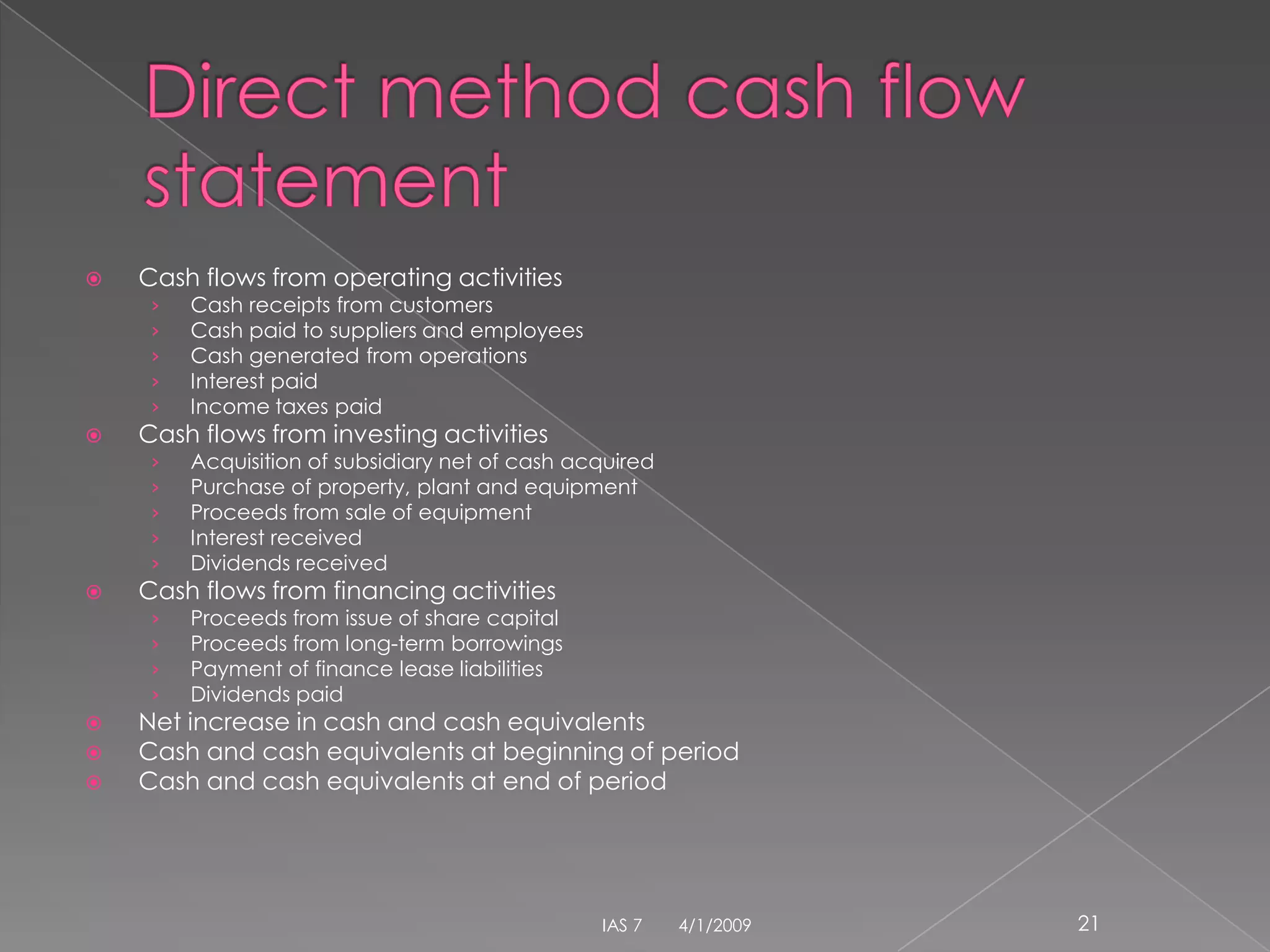

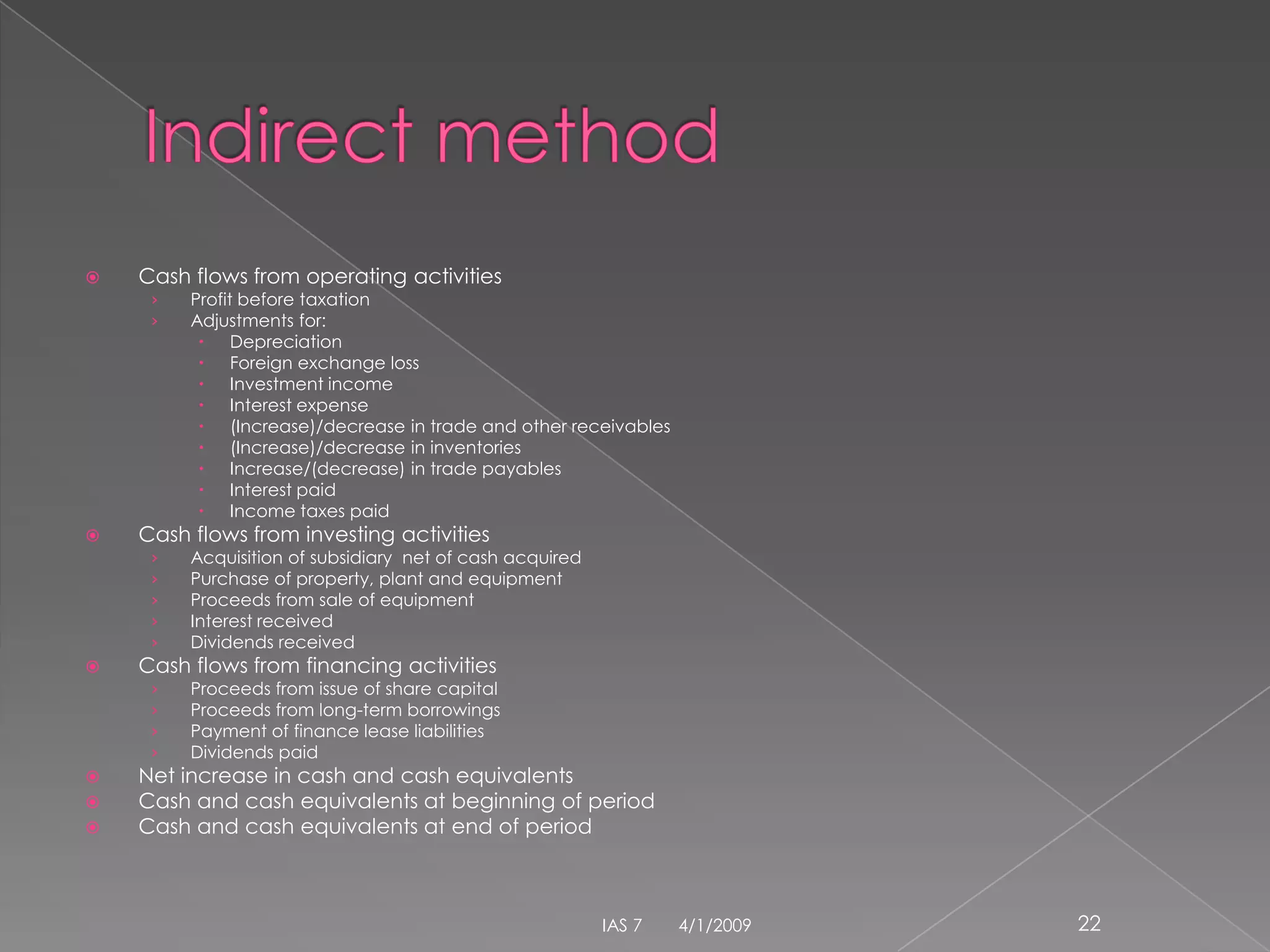

IAS 7 provides guidance on cash flow statements. It requires entities to present a statement of cash flows which classifies cash flows during a period into operating, investing and financing activities. Cash flows are presented using either the direct or indirect method. Non-cash transactions are excluded from the cash flow statement. Cash flows must be reconciled to cash and cash equivalents reported on the balance sheet, and any restrictions on cash must be disclosed.