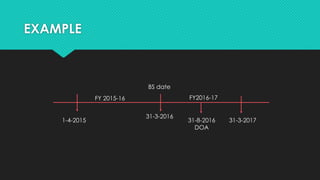

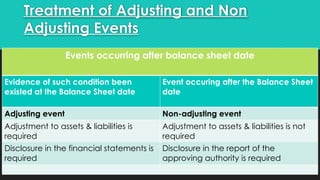

Accounting Standard (AS) 4 addresses contingencies and events occurring after the balance sheet date, outlining their types, treatments, and required disclosures. It differentiates between adjusting events, which provide evidence of conditions existing at the balance sheet date, and non-adjusting events, which arise after that date. Disclosure requirements include the nature of the event and its financial effects, with exceptions when a going concern assumption is questioned.