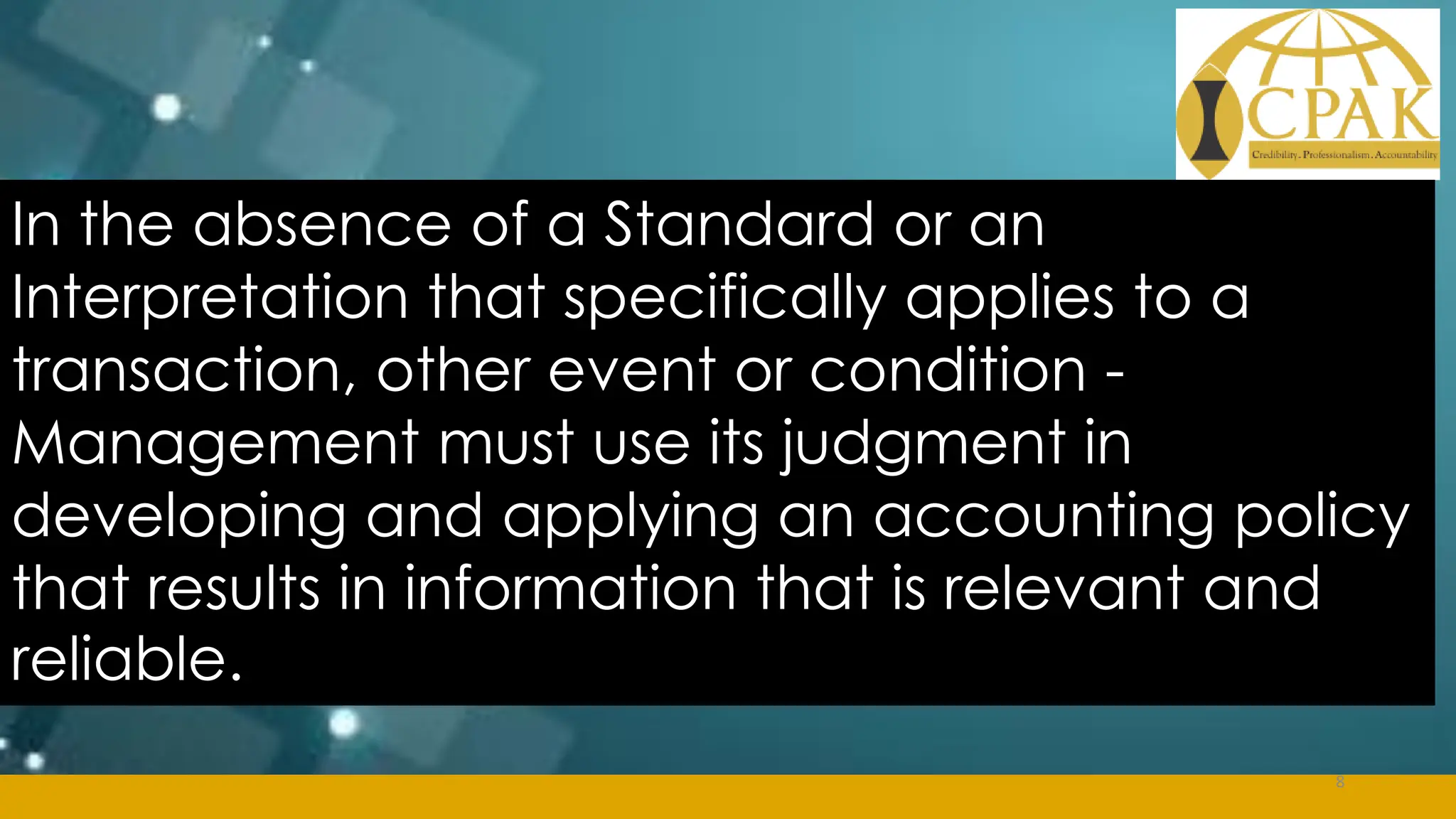

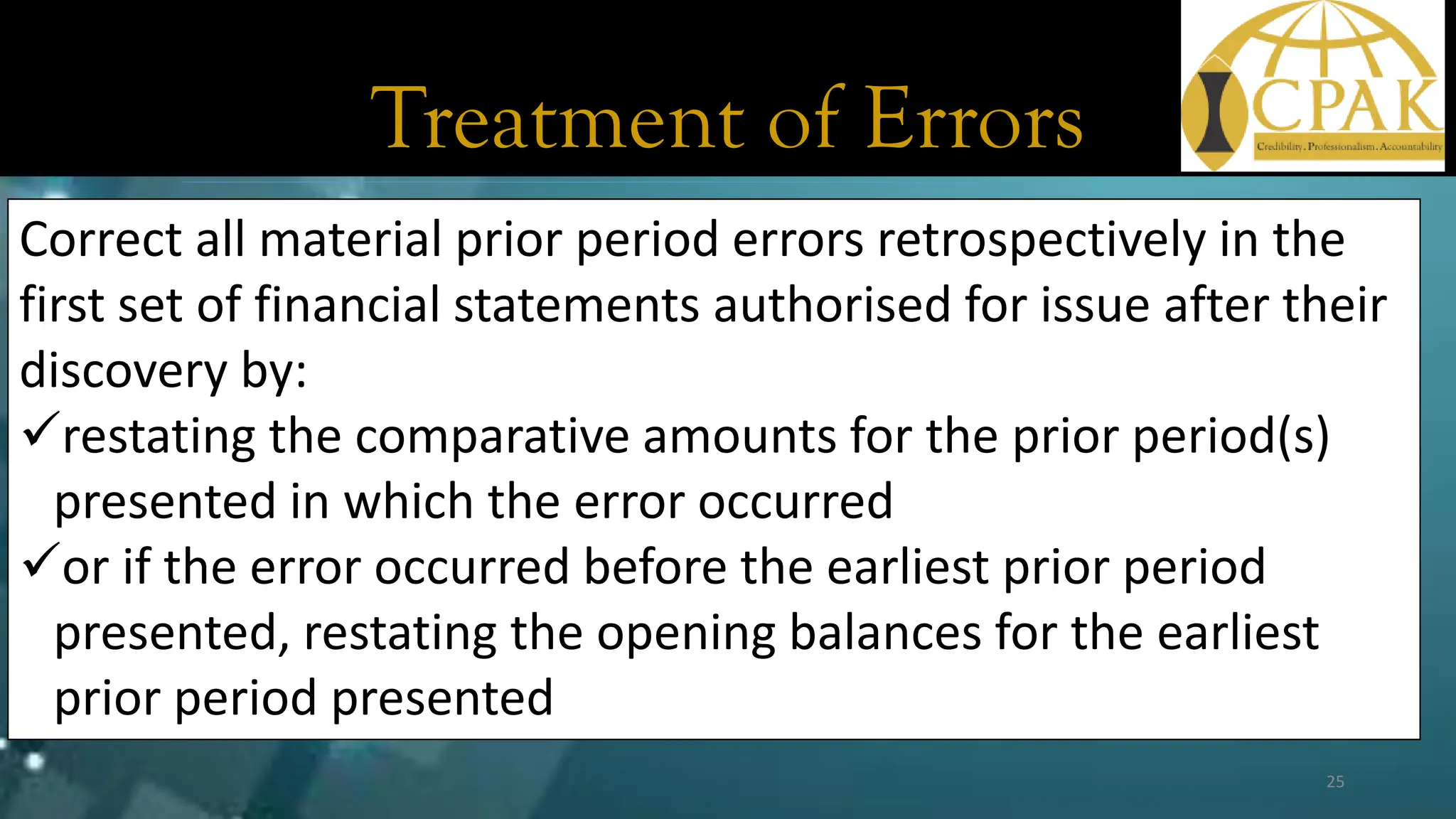

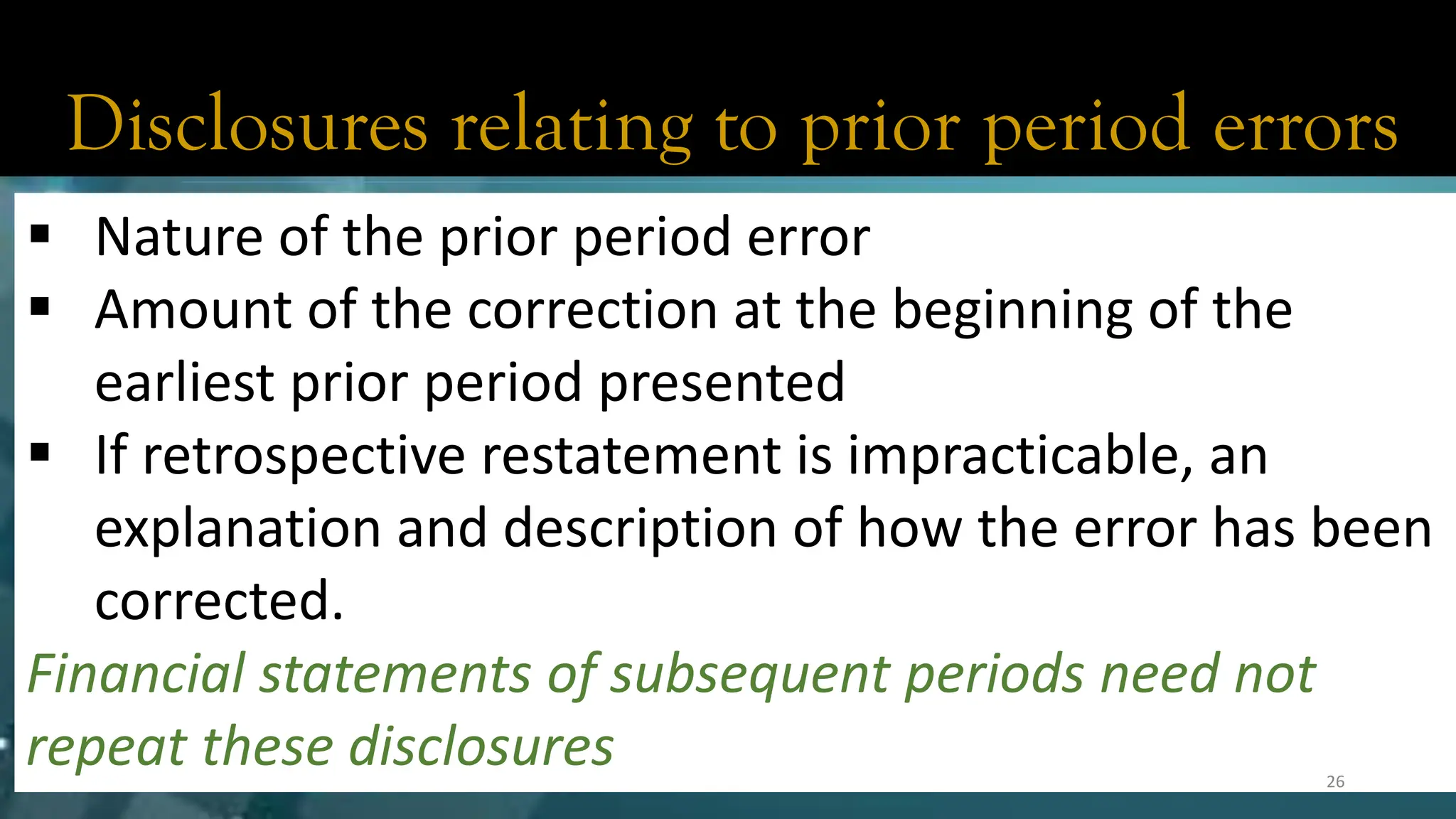

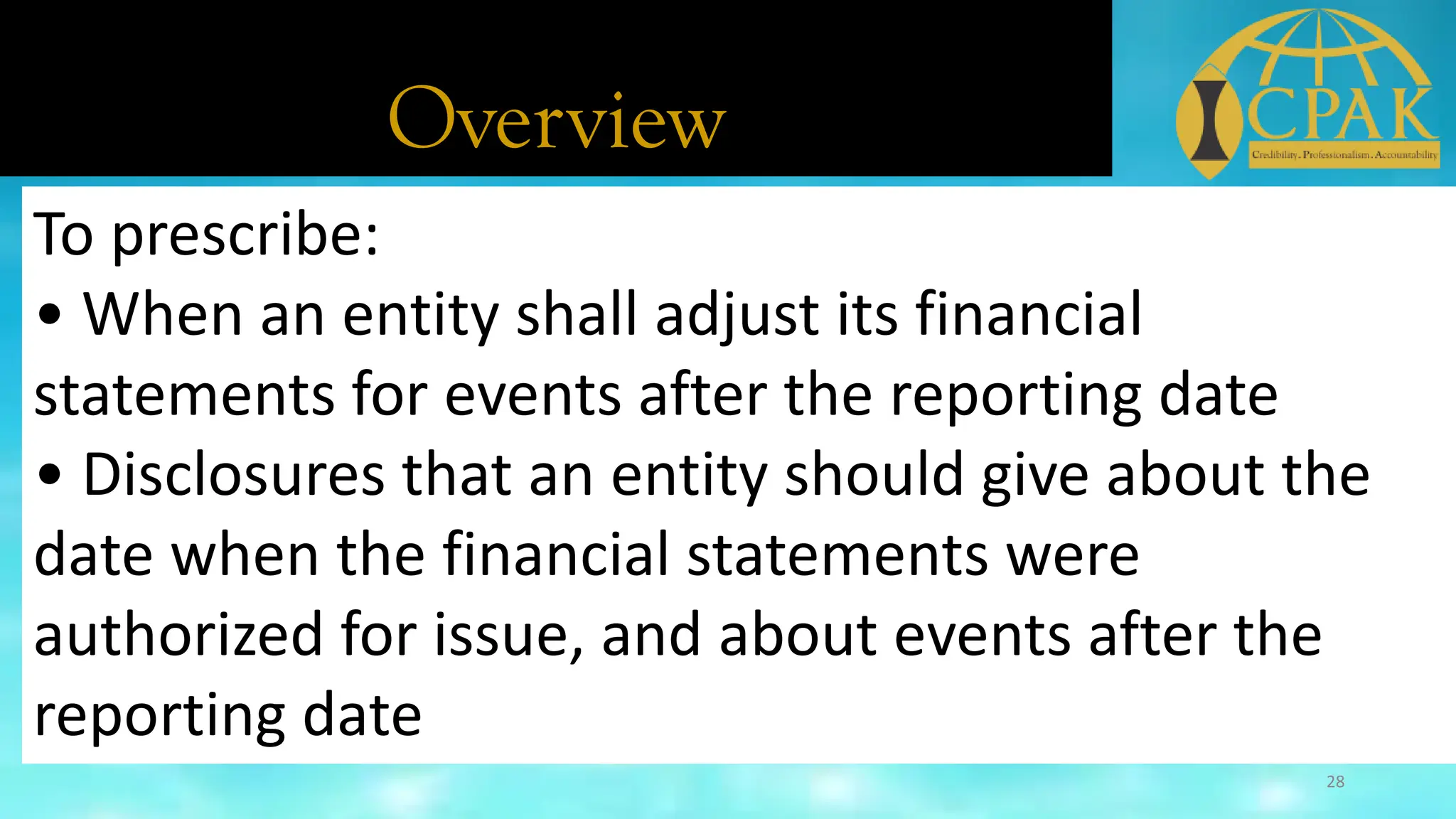

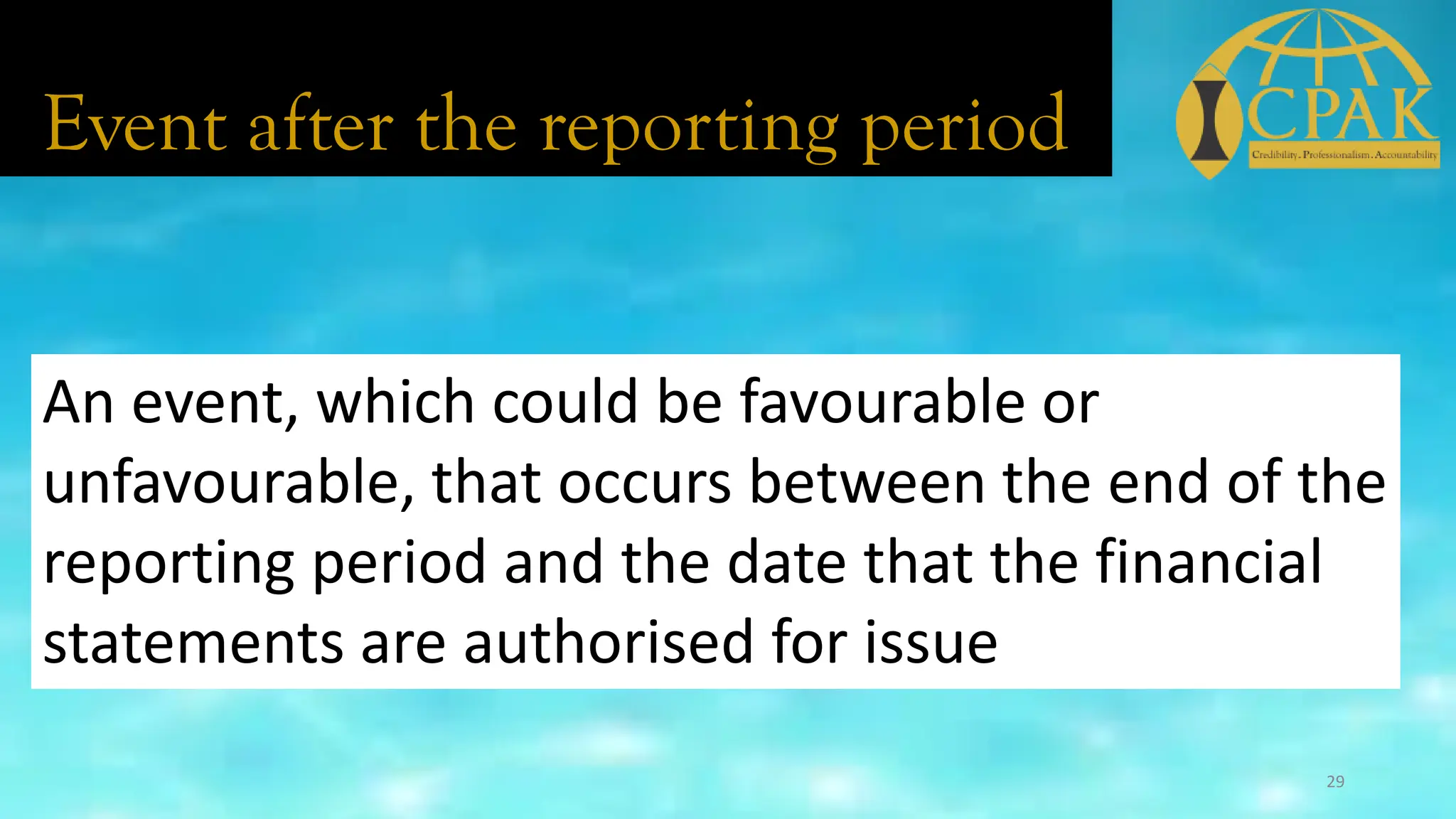

This document provides an overview and summary of key points from IPSAS 3 on accounting policies, changes in estimates and errors. It discusses the objective and requirements around selection and application of accounting policies, consistency of policies, treatment of changes in policies and estimates, and corrections of prior period errors. Key disclosure requirements are also outlined.

![DND - Cost Reduction Strategies to Enhance Operational Efficiency for SMEs[1]...](https://cdn.slidesharecdn.com/ss_thumbnails/dnd-costreductionstrategiestoenhanceoperationalefficiencyforsmes1-241028085054-45982cc1-thumbnail.jpg?width=640&height=640&fit=bounds)

![DND - Cost Reduction Strategies to Enhance Operational Efficiency for SMEs[1]...](https://cdn.slidesharecdn.com/ss_thumbnails/dnd-costreductionstrategiestoenhanceoperationalefficiencyforsmes1-240922065555-6ee2ed93-thumbnail.jpg?width=640&height=640&fit=bounds)