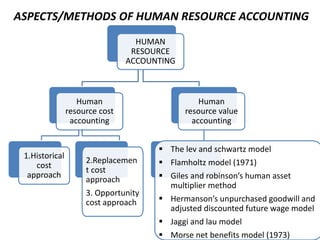

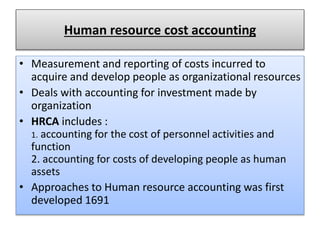

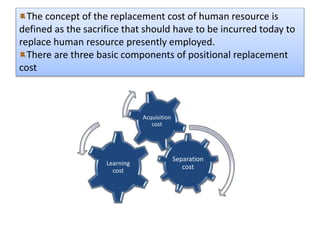

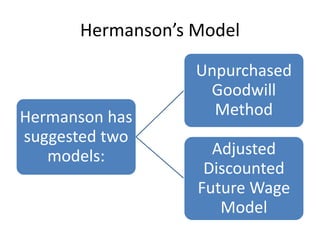

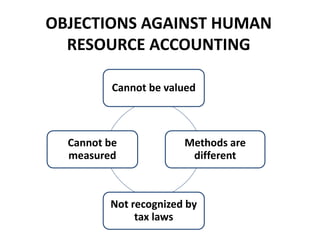

Human resource accounting aims to value and account for human resources as organizational assets. There are two main approaches: human resource cost accounting, which deals with accounting for investment in developing employee skills; and human resource value accounting, which attempts to place a monetary value on employees. Several models have been developed for human resource value accounting, including the Lev and Schwartz model, Flamholtz model, Giles and Robinson's human asset multiplier method, and Hermanson's unpurchased goodwill and adjusted discounted future wage models. Implementing human resource accounting provides quantitative information to support decision making around areas like training, recruitment, and resource allocation. However, limitations include uncertainty around employee tenure and difficulty measuring individual contributions to organizational effectiveness.