Downloaded 62 times

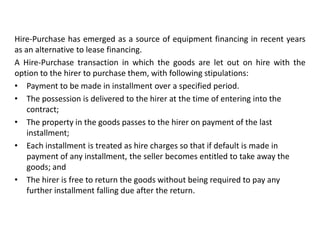

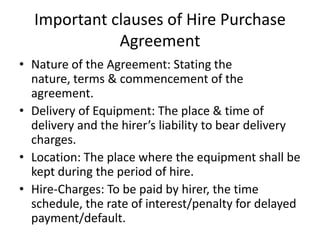

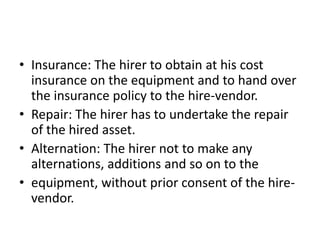

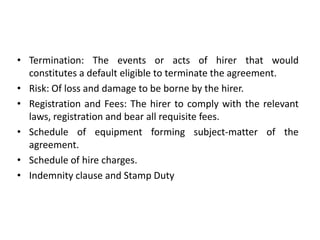

Hire purchase is a form of financing where goods are leased with the option to purchase. Key aspects include: - Payments are made in installments over a set period, with possession given initially but ownership transferring after the final payment. - If payments are defaulted on, the seller can repossess the goods. The hirer can also return goods before completing payments. - A hire purchase agreement has aspects of both a bailment for the lease period and a sale when the purchase option is exercised. - Ownership transfers to the hirer on the final payment, but the financier retains ownership until then despite the hirer controlling the goods.