Download to read offline

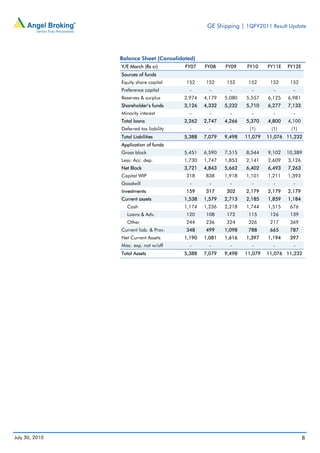

- GE Shipping's (Gesco) 1QFY2011 results were above estimates due to strong performance in the offshore segment, however the shipping segment was impacted by lower freight rates and tonnage. - Revenue declined 10.6% YoY due to a 31.6% decline in the shipping segment, offset by 45.1% growth in the offshore segment. - EBITDA margin expanded 495 bps YoY to 40.6% due to strong margins in the offshore segment. - PAT grew 11.4% YoY to Rs. 171.8 cr. Management expects to list its offshore subsidiary Greatship by 2HFY2011 which will unlock value.