Downloaded 802 times

![Nabendu Maji Bharati Vidyapeeth University Institute Of Management And Entrepreneurship Development, Pune MBA (G) – B Roll No. 73 [email_address]](https://image.slidesharecdn.com/forensicaccounting-111003123908-phpapp01/75/Forensic-Accounting-1-2048.jpg)

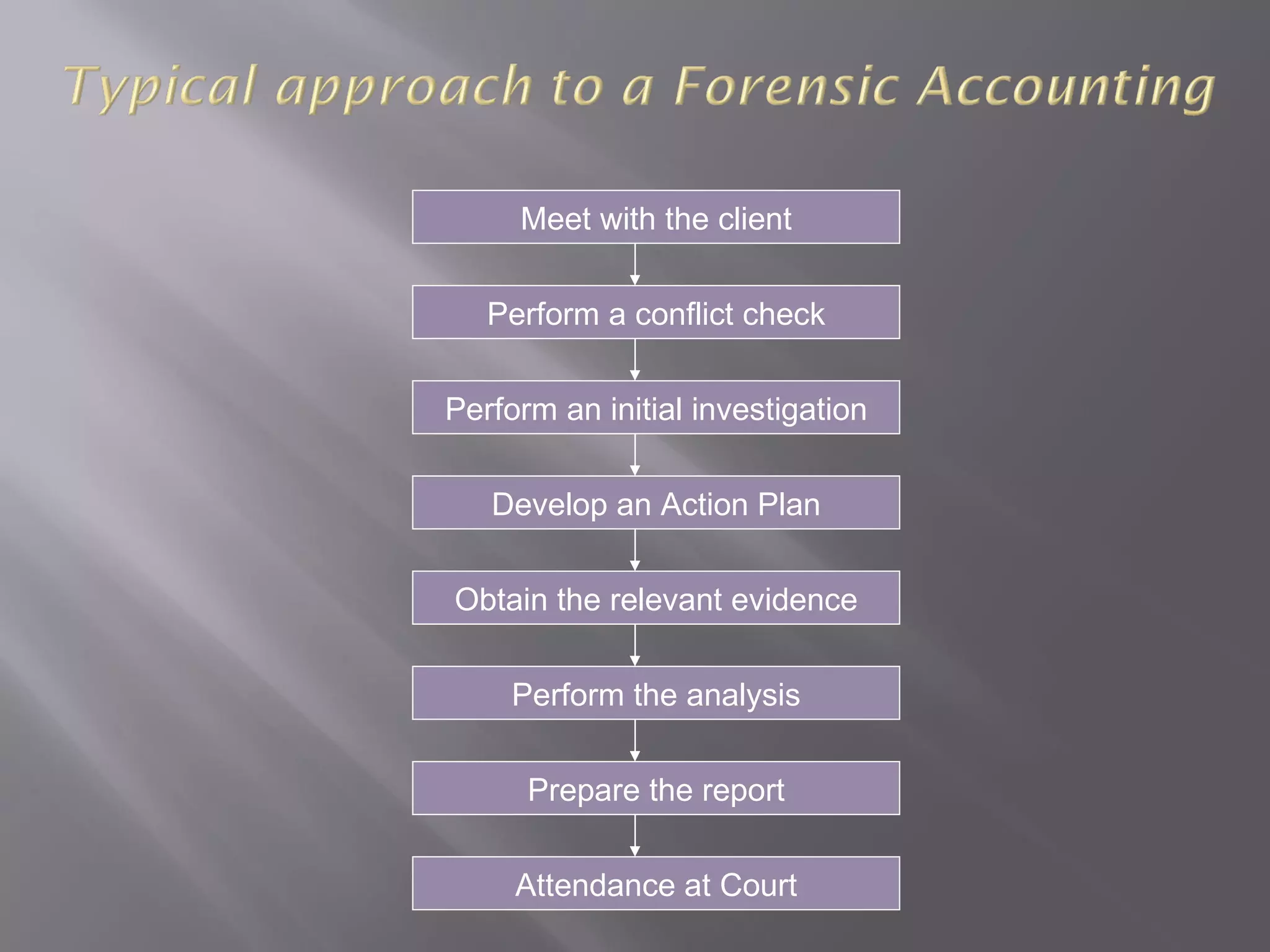

This document discusses forensic accounting, including what forensic accountants do and the typical process they follow. It defines forensic accounting as utilizing accounting, auditing, and investigative skills to identify, interpret, and communicate evidence from financial transactions and events, especially for actual or anticipated legal disputes. It describes that forensic accountants perform investigations and analyses of complex financial issues to assist with litigation, insurance claims, fraud investigations, and other legal matters. The typical process involves meeting with clients, collecting relevant evidence, analyzing the evidence, preparing a report, and presenting findings.