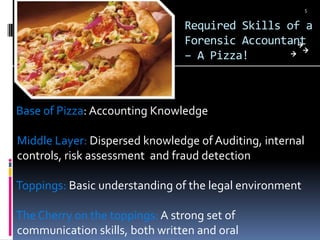

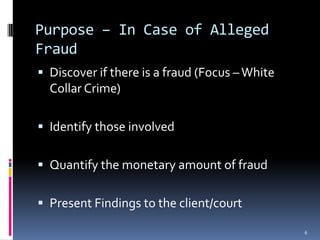

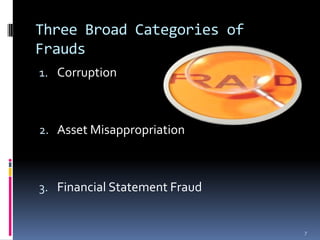

This document discusses forensic auditing. It begins by defining forensic auditing as investigating financial records to determine if fraud has occurred. A forensic accountant requires skills in accounting, auditing, and communication. Forensic audits aim to discover if fraud happened, identify those involved, quantify losses, and present findings. There are three broad categories of fraud - corruption, asset misappropriation, and financial statement fraud. A forensic audit involves accepting the investigation, planning, gathering evidence through various techniques, and reporting findings which may be presented in court. It requires a skilled team comfortable with legal proceedings.

![The [social] future of public financial management](https://cdn.slidesharecdn.com/ss_thumbnails/thesocialfutureofpublicfinancialmanagement-120429213457-phpapp02-thumbnail.jpg?width=640&height=640&fit=bounds)